The global financial system has witnessed a profound shift as interest rates have surged to levels not observed in over two decades, fundamentally altering the cost of borrowing and investing. This dramatic reversal from a prolonged era of near-zero rates, primarily orchestrated by central banks worldwide, particularly the U.S. Federal Reserve, represents a pivotal moment with far-reaching implications for consumers, businesses, and investors alike. The rapid escalation of rates, a stark departure from the stability experienced since the 2008 financial crisis, has prompted widespread reevaluation of financial strategies and economic outlooks.

The End of an Era: From Ultra-Low Rates to Inflationary Pressures

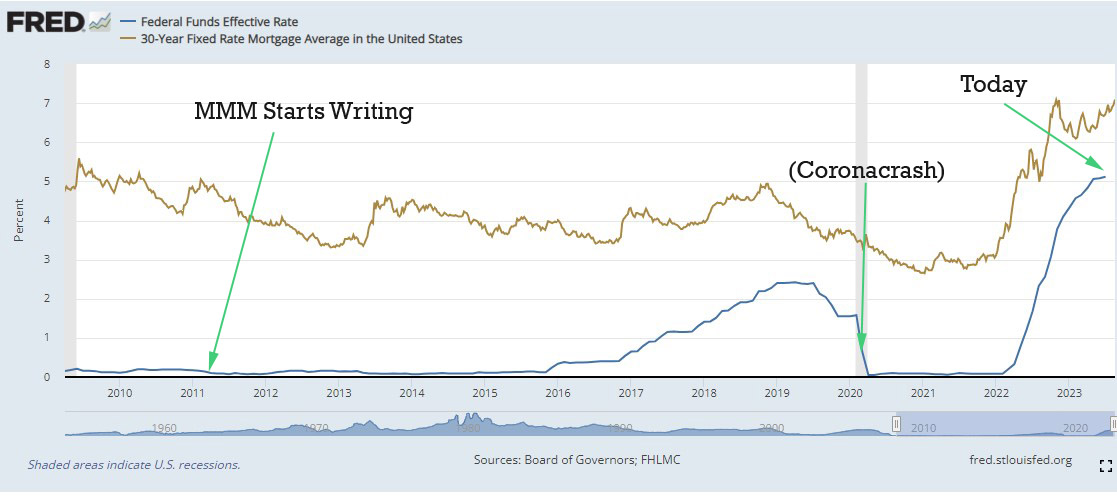

For nearly fourteen years, a period extending well before 2011, the financial world operated under the pervasive influence of exceptionally low interest rates. Following the 2008 global financial crisis and reinforced during the COVID-19 pandemic, central banks implemented accommodative monetary policies, pushing benchmark rates to historic lows, often hovering near zero. This environment was characterized by readily available and inexpensive credit, designed to stimulate economic activity, encourage investment, and foster job creation.

This prolonged period of easy money fueled significant growth across various sectors. Mortgages became more affordable, driving demand in the housing market and stimulating both existing home sales and new construction. Businesses, benefiting from cheap capital and venture funding, expanded rapidly, leading to the formation of new companies, increased office rentals, factory construction, and robust hiring. This economic dynamism contributed to two decades of prosperity, technological innovation, and rising living standards in many developed economies.

However, the sustained infusion of liquidity eventually led to an imbalance: too much money chasing too few goods, particularly evident in the housing sector and various consumer goods. This imbalance, exacerbated by supply chain disruptions during the pandemic and geopolitical events, culminated in unacceptably high inflation rates. The U.S. Consumer Price Index (CPI), for instance, soared to a 40-year high of 9.1% in June 2022, far exceeding the Federal Reserve’s target of 2%. This inflationary surge signaled the end of the ultra-low interest rate regime and necessitated a decisive policy response.

The Federal Reserve’s Pivot: A Measured but Aggressive Tightening Cycle

Confronted with persistent and elevated inflation, the U.S. Federal Reserve, under Chairman Jerome Powell, began a series of aggressive monetary policy tightenings in March 2022. The Fed’s dual mandate — to achieve maximum employment and maintain price stability — shifted its focus decisively towards curbing inflation. The federal funds rate, the benchmark for many other interest rates in the economy, was incrementally raised from near zero to over 5% within a span of less than two years. This marked the fastest pace of rate hikes since the 1980s.

The rationale behind these rate hikes is to cool down an overheated economy by making borrowing more expensive, thereby reducing aggregate demand. Higher interest rates increase the cost of mortgages, auto loans, credit card debt, and business financing, discouraging consumption and investment. The goal is to bring inflation back down to the target 2% without triggering a severe recession, a scenario often referred to as a "soft landing."

Widespread Economic Repercussions

The rapid increase in interest rates has rippled through virtually every segment of the economy, producing both intended and unintended consequences.

-

Housing Market Dynamics: The most immediate and significant impact has been felt in the housing sector. Mortgage rates, particularly for the popular 30-year fixed-rate mortgage, have more than doubled, climbing from approximately 3% in late 2021 to over 7.5% by mid-2023. This dramatic increase has severely eroded housing affordability. For instance, a hypothetical $400,000 home with a 10% down payment saw its monthly principal and interest payment jump from around $1,519 at a 3% rate to approximately $2,530 at a 7.5% rate – a 66% increase. This surge in costs has priced many potential buyers out of the market, leading to a significant slowdown in home sales and a reduction in new housing starts. While home prices remain elevated in many areas, the rate of appreciation has slowed considerably, with some regions experiencing modest declines. The "lock-in" effect is also notable, as homeowners with existing low-rate mortgages are reluctant to sell and incur a much higher financing cost for a new property.

-

Business Investment and Employment: Companies now face higher borrowing costs for expansion, equipment purchases, and operational capital. This has led to a noticeable scaling back of investment plans, with many businesses postponing new projects or reducing their capital expenditures. The technology sector, particularly sensitive to interest rates due to its reliance on future growth projections, has experienced significant layoffs. Major tech giants like Amazon and Meta (Facebook’s parent company) announced tens of thousands of job cuts, signaling a broader trend of companies prioritizing efficiency and cost-cutting over rapid expansion. However, despite these targeted layoffs, the overall labor market has shown remarkable resilience, with the national unemployment rate remaining near 50-year lows, confounding many economists’ predictions of a more substantial slowdown.

-

Banking Sector Vulnerabilities: The swiftness of rate hikes exposed vulnerabilities within the banking system. In March 2023, the U.S. witnessed a "miniature banking crisis" with the failures of Silicon Valley Bank (SVB) and Signature Bank. These institutions, heavily invested in long-dated, low-yield bonds, suffered significant losses as rising interest rates depreciated the value of their bond portfolios. When depositors, particularly in the tech sector, initiated large-scale withdrawals, these banks faced liquidity crises, leading to their collapse. The events highlighted the systemic risks associated with rapid monetary tightening and prompted regulatory scrutiny and temporary government interventions to stabilize the financial system.

Investment Strategies in a High-Rate Environment

The altered interest rate landscape necessitates a reevaluation of investment approaches for both individual and institutional investors.

-

Equity Markets: The stock market has experienced increased volatility in response to rising rates. Higher borrowing costs can dampen corporate profits, and the present value of future earnings is discounted more heavily. From its peak in early 2022, the overall U.S. market saw a significant correction, declining by approximately 10% by mid-2023. While this represents a period of flat or negative returns, long-term investors often view such downturns as opportunities. Historically, the stock market tends to trend upwards over extended periods, making consistent, disciplined investing (e.g., through dollar-cost averaging into index funds) a widely recommended strategy. The current market "discount" of roughly 10% compared to peak prices could enhance long-term returns for new investments.

-

Fixed Income and Savings: The attractiveness of cash and fixed-income investments has surged. Savings accounts, money market funds, and short-term bonds now offer yields upwards of 4-5%, a substantial increase from the sub-1% rates of previous years. This presents a compelling alternative for capital preservation and modest returns, particularly for investors seeking lower risk. The decision between allocating capital to equities versus fixed income now involves a more nuanced risk-reward calculation, as guaranteed returns from stable instruments are significantly higher. However, it’s crucial to remember that while 4-5% yields are attractive, they may still be outpaced by long-term stock market returns, especially if equities are purchased during a market downturn and subsequently recover.

The Outlook for Housing Prices and Future Interest Rates

Forecasting the trajectory of housing prices and interest rates remains complex, with various factors at play.

-

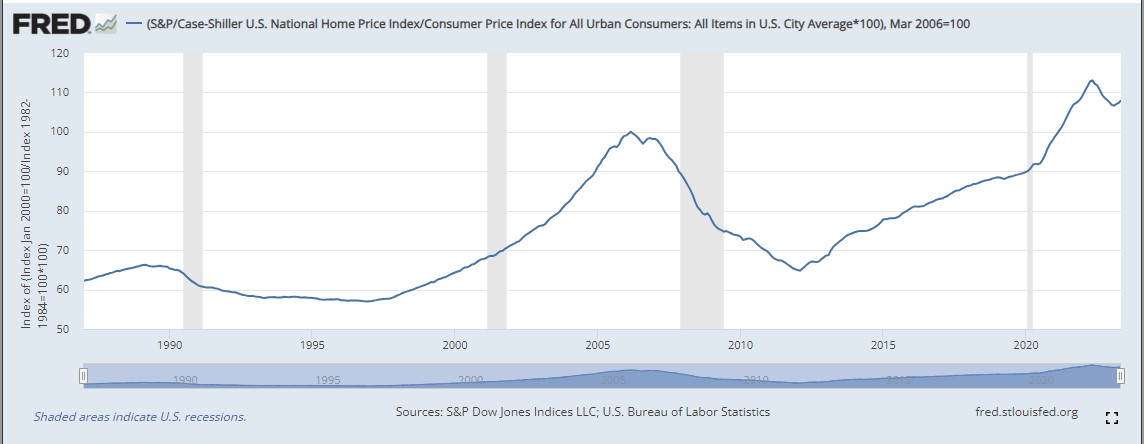

Housing Price Projections: The "value" of a house is intrinsically linked to supply and demand dynamics. While higher interest rates are intended to cool demand, the supply side faces its own challenges. Construction costs, encompassing materials and labor, continue to be a significant factor. While technological advancements and global trade can make some components cheaper over time, other inputs remain costly. Furthermore, local regulatory hurdles, restrictive zoning laws, and protracted approval processes in many municipalities severely constrain new housing development. These "Not In My Backyard" (NIMBY) policies create artificial scarcity, pushing prices higher. Given that inflation-adjusted U.S. house prices are near all-time highs, some analysts suggest a potential for a 10-25% correction or, more likely, a prolonged period of flat prices that do not keep pace with inflation, effectively making homes relatively cheaper over time compared to rising incomes. However, outcomes will vary significantly by region depending on local supply-demand balances and regulatory environments.

-

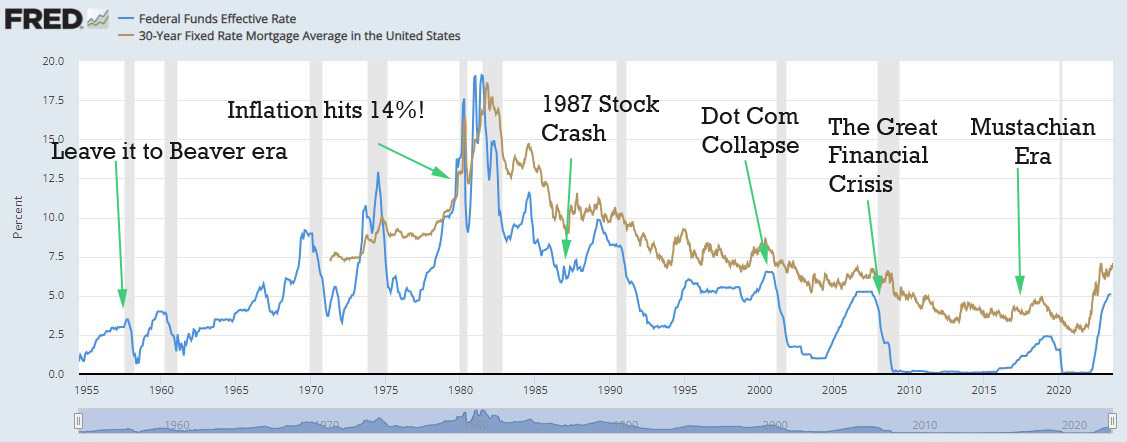

When Will Interest Rates Decline? The current "high" interest rates are, in a broader historical context spanning the last seventy years, closer to average than extreme. This suggests that the recent period of ultra-low rates was an anomaly, and current levels might represent a return to a more normalized environment.

The future path of interest rates largely hinges on the Federal Reserve’s assessment of economic conditions, particularly inflation and employment data. Rates are expected to decline only when the economy shows clear signs of cooling, such as sustained low inflation, rising unemployment, and other indicators of a genuine economic slowdown or recession.

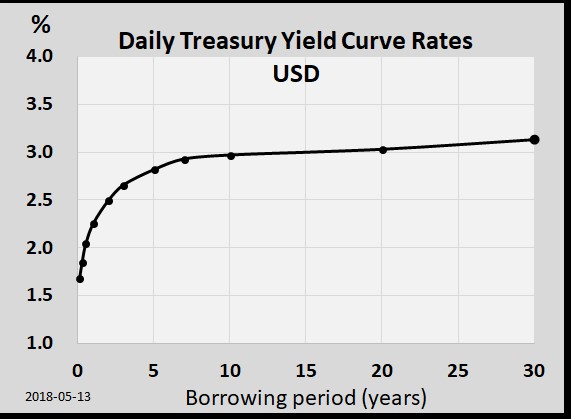

A key indicator for market expectations is the U.S. Treasury Yield Curve. Traditionally, longer-term bonds offer higher yields than shorter-term ones, rewarding lenders for locking up their money for longer. However, the current environment features an inverted yield curve, where short-term rates (e.g., 1-year Treasury bills yielding ~5.4%) are higher than long-term rates (e.g., 10-year Treasury bonds yielding ~4.05%). This inversion implies that bond buyers anticipate interest rates will fall in the future, typically starting within 12-18 months. Historically, an inverted yield curve has been a remarkably accurate predictor of future recessions, preceding ten of the last eleven U.S. recessions over the past 75 years. Based on this historical precedent and current market sentiment, many economists and market participants anticipate interest rates may begin to decline within 18-24 months, potentially accompanied by an economic contraction.

Strategic Financial Preparedness in Volatile Times

The current economic environment underscores the importance of financial prudence and adaptability. While market fluctuations and interest rate changes are beyond individual control, personal financial choices remain paramount. Maintaining a lean and sustainable lifestyle, prioritizing saving, and judiciously managing debt are foundational principles for navigating economic shifts.

For those considering significant financial decisions, such as purchasing a home, the current landscape demands careful consideration. While higher mortgage rates present a challenge, having substantial savings or the ability to purchase outright can provide a position of strength, reducing reliance on external financing and offering flexibility to capitalize on potential market opportunities.

Ultimately, the focus should remain on long-term financial health. By establishing robust savings, minimizing high-interest debt, and making informed decisions about earning and spending, individuals can build resilience against economic headwinds. The transient ripples of interest rate shifts and market volatility can be better managed when the fundamental "sails" of one’s financial life—income, savings, and responsible consumption—are optimally aligned, steering towards enduring stability and prosperity.