A recent commentary from a reader of the Financial Independence, Retire Early (FIRE) movement has ignited a crucial discussion regarding the accessibility and applicability of its core principles in the current economic landscape. The reader articulated a growing sentiment, suggesting that much of the established FIRE advice, particularly from earlier proponents, appears increasingly disconnected from the realities faced by individuals in 2024. This perspective highlights concerns that the foundational narratives of early FIRE adopters, often characterized by high-earning tech salaries and pre-2019 home purchases at significantly lower prices, may no longer resonate with a generation contending with escalating housing costs, elevated interest rates, and the broader economic shifts of the post-pandemic era.

The Evolving Landscape of Financial Independence

The critique posited that the prevailing advice – such as "house hacking" or "buying a fixer-upper" – is often financially out of reach or logistically complex given current market conditions and restrictive local zoning regulations. This reflects a broader apprehension that the pathways to financial independence, once seemingly straightforward for a privileged few, might be narrowing for many others who did not embark on their FIRE journey during a more economically opportune period. The commenter’s plea for a "next generation of FI bloggers" underscores a desire for updated strategies and voices that address contemporary challenges more directly.

The FIRE movement, which gained significant traction in the early 2010s, advocates for aggressive saving and investing to accumulate sufficient capital to live off investment returns, thereby enabling early retirement. Its tenets often emphasize frugality, strategic income generation, and significant savings rates (typically 50-70% of income). Proponents, including early bloggers like Mr. Money Mustache, have long championed a lifestyle focused on conscious spending, waste reduction, and maximizing financial efficiency. However, the economic environment has undergone substantial transformations since the movement’s early days, prompting a re-evaluation of its practical implementation.

Income vs. Expenditure: The Enduring Mustachian Principle

A central tenet of Mustachian philosophy, a subset of FIRE, emphasizes that while income generation is important, the control of expenditure is paramount. This perspective posits that even substantial incomes can be eroded by unchecked spending, a phenomenon observed in high-earning professionals who still experience financial stress despite decades of high salaries. The argument is that the ability to "waste almost any amount of income" remains a universal truth, making spending efficiency a critical skill across all income brackets. For those on lower income scales, judicious spending becomes even more vital, transforming waste reduction into a potent tool for wealth accumulation rather than merely a supplementary measure.

Historically, the FIRE movement has weathered various economic cycles that led critics to declare its obsolescence. From the dot-com bust of the early 2000s, which challenged aggressive growth investment strategies, to the 2008 global financial crisis that decimated portfolios and real estate values, and subsequent periods of low-interest rates and quantitative easing, the fundamental principles of saving, investing, and mindful consumption have consistently proven adaptable. Each perceived "crisis" has merely served to refine and strengthen the movement’s core message: financial resilience is built not on market timing or extraordinary income alone, but on disciplined habits and a flexible mindset.

The Housing Conundrum: Data and Reality

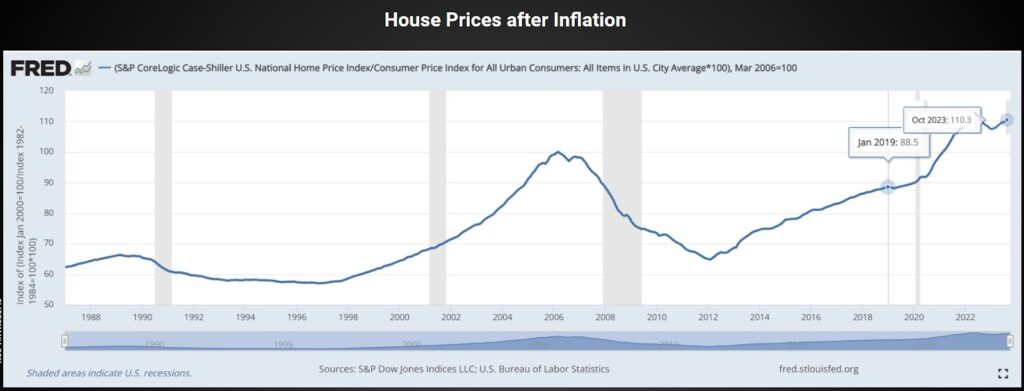

The discussion particularly zeroes in on housing, a cornerstone of personal finance and a significant barrier for many aspiring to financial independence. The perception of an inflated housing market is not unfounded. Data from the St. Louis Federal Reserve (FRED) illustrates that, adjusted for inflation, U.S. house prices in 2024 are approximately 25% higher than at the start of 2019. This represents a substantial increase over a relatively short period, outpacing average salary growth in many regions. However, a longer historical view reveals a more nuanced picture: current inflation-adjusted prices are only about 10% higher than the previous peak in early 2006, eighteen years prior. This suggests that while recent increases are sharp, the overall long-term trajectory might not be as unprecedented as it "feels" in the immediate post-pandemic context.

Despite the national averages, localized markets exhibit significant disparities. Cities like Longmont, Colorado, for instance, have seen median home prices soar to $540,000, roughly triple their value since 2011. This means houses in such desirable locales have indeed outpaced average salary growth, pushing homeownership further out of reach for many within those specific communities. This regional divergence underscores a critical challenge: the national data, while informative, often masks acute local crises in affordability, making strategies like "house hacking" difficult due to cost or restrictive zoning, as highlighted by the reader.

Geographical Arbitrage: A Core Strategy Reimagined

In response to these localized housing pressures, a core Mustachian principle—geographical arbitrage—is increasingly advocated. This strategy, often referred to as "house shopping with your middle finger" to cultural expectations, involves treating housing as any other market product: subject to supply, demand, and variable pricing. It encourages individuals to transcend emotional or historical ties to a specific location and instead evaluate housing decisions through a pragmatic lens, considering the broader spectrum of available options.

This approach involves a multi-step decision-making process:

- Analyze Needs: Identify essential requirements for a happy and functional life (e.g., climate, community, access to nature, employment opportunities).

- Evaluate Options: Research various locations, both domestically and internationally, that meet these needs.

- Run the Numbers: Compare the cost of living, particularly housing, across these options, factoring in local salaries, taxes, and amenities.

- Decide: Choose between renting, buying, or house hacking, potentially in a new location that offers better value.

The underlying premise is that a "birthright" to afford housing in one’s hometown is an economically unsound assumption. Just as one does not automatically receive a luxury product simply for residing near its manufacturer, one cannot expect to effortlessly afford a home in an increasingly expensive area without considering alternatives.

Domestic Relocation: Unlocking Value Within Borders

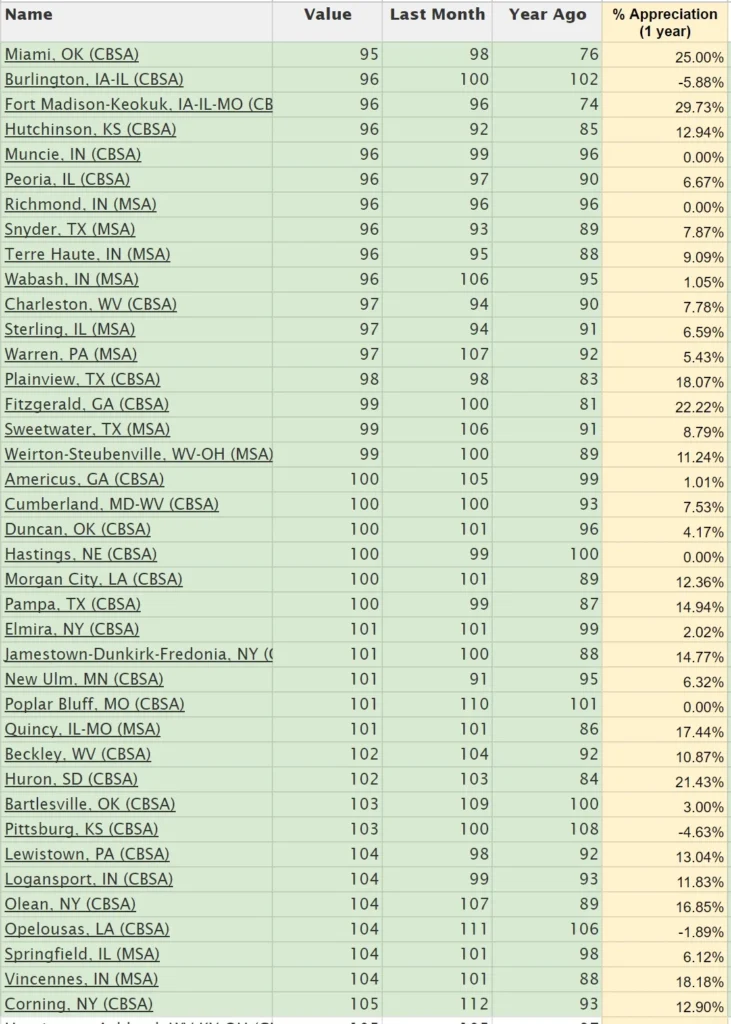

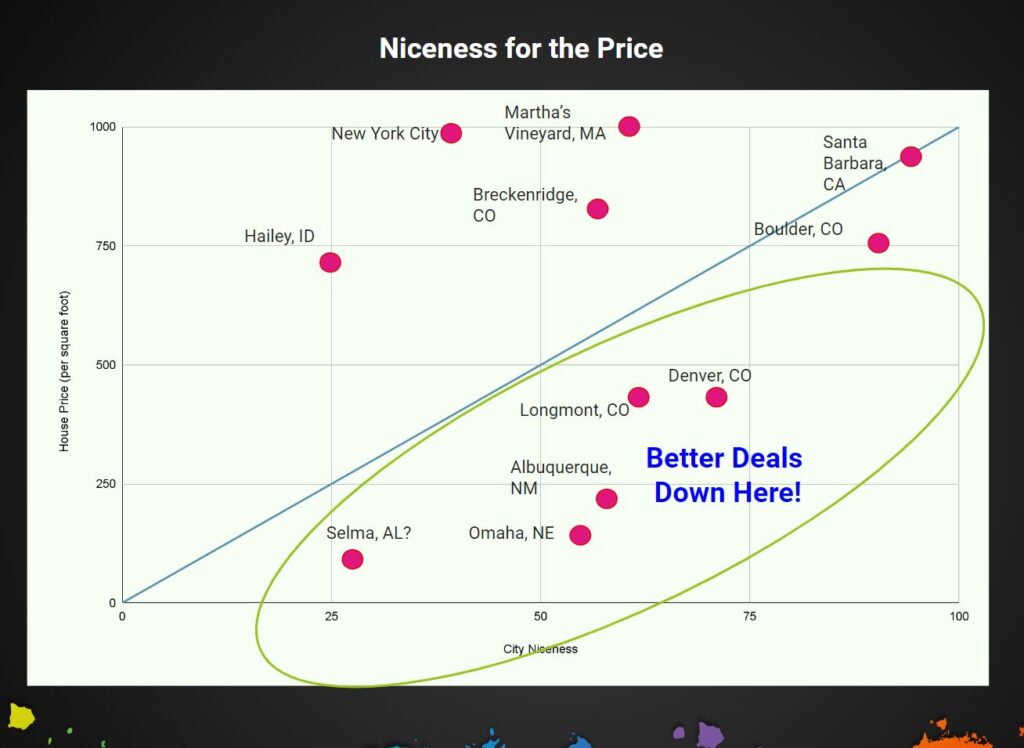

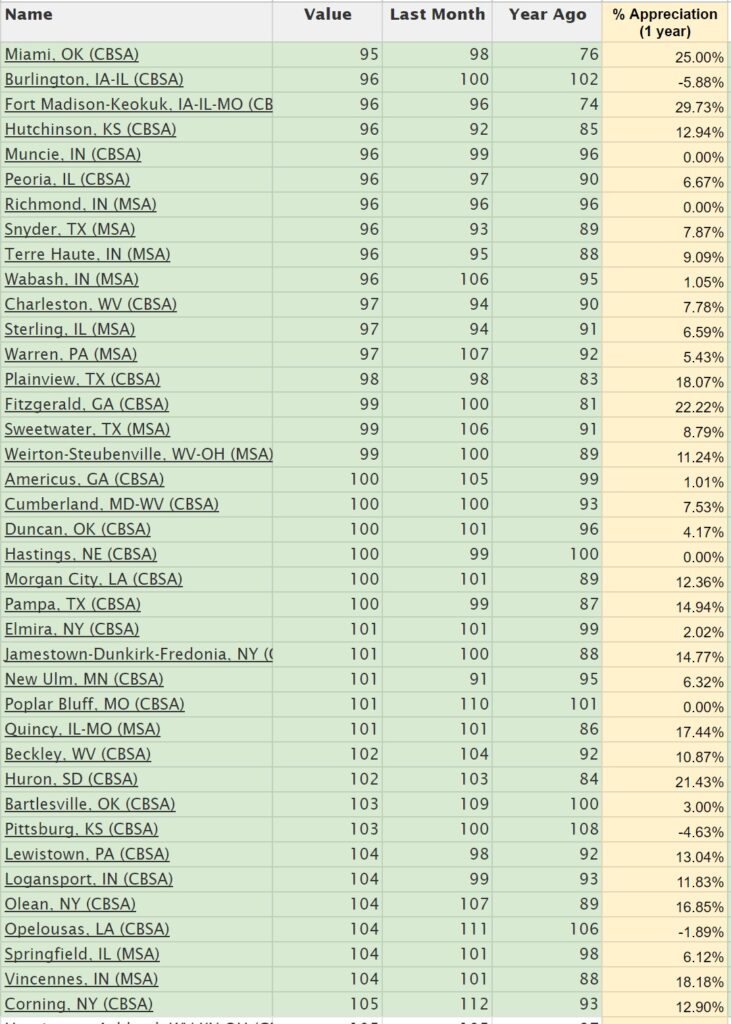

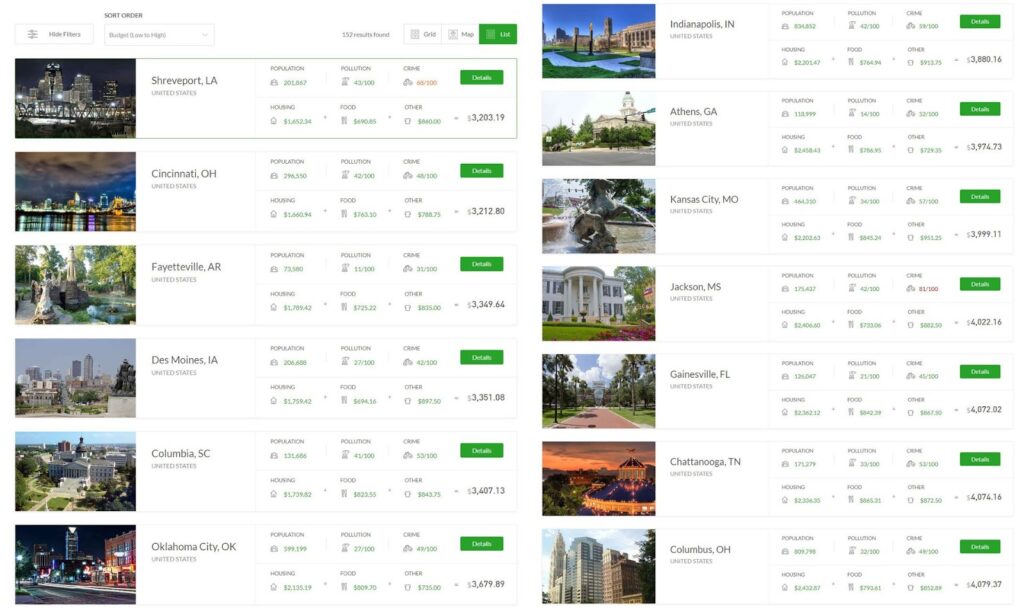

The United States, with its vast geographical and economic diversity, presents ample opportunities for domestic geographical arbitrage. The irrational patterns of housing prices across the country—ridiculously high in some desirable areas, surprisingly affordable in others—create significant opportunities for those willing to relocate. Online tools, such as the St. Louis Fed’s list of metro areas by price per square foot, enable data-driven research into cities offering better value. For example, while Longmont, Colorado, might command $450 per interior square foot, a city like Albuquerque could offer a comparable quality of life at a significantly lower cost.

This analytical approach encourages prospective homeowners to consider a wider range of cities that balance affordability with desirable amenities. By sorting data by cost per square foot, individuals can identify a band of affordable cities where a 2,000 square foot home might cost around $200,000, representing a substantial reduction in capital outlay compared to high-cost areas. Furthermore, tracking year-over-year price changes in these cities can provide insights into market trends, helping to identify areas that are either appreciating rapidly or becoming more affordable.

International Horizons: Expanding the Search for Affordability

For those with a more adventurous spirit, the concept of geographical arbitrage extends beyond national borders. Platforms like "The Earth Awaits," developed by FIRE community members, allow users to filter global cities based on specific criteria such as budget, family size, housing preferences (e.g., two-bedroom outside city center), and even climate preferences. A hypothetical search for a two-person household in North America, with a budget of up to $6,000 per month and mild winters (January lows not colder than 10F), can yield a diverse list of affordable cities like Fayetteville, Arkansas; Columbia, Missouri; or Chattanooga, Tennessee. These tools not only present cost data but also provide population figures, offering a glimpse into the "feel" of a city—an essential qualitative factor for relocation.

Expanding the search to regions like South America reveals even greater affordability. Cities in countries such as Ecuador, Colombia, or Peru often offer a significantly lower cost of living, including housing, for those willing to embrace a new cultural environment. While international relocation introduces additional layers of complexity—including visa requirements, legal frameworks, cultural integration, and maintaining ties with one’s home country—these challenges are framed as "Adulting Puzzles" rather than insurmountable obstacles. The argument is that the long-term financial and lifestyle benefits of a strategic international move far outweigh the temporary administrative hassles.

Addressing the "Fear of Change"

A significant psychological barrier to geographical arbitrage is the inherent human resistance to change and the strong emotional ties to current locations, families, and established routines. This "fear of change" can often overshadow rational economic analysis, leading individuals to remain in financially suboptimal environments. However, the FIRE philosophy encourages questioning these assumptions, distinguishing between genuine, positive bonds to a place and mere inertia or apprehension.

The act of moving, even internationally, is presented as a series of manageable tasks: research, paperwork, phone calls, and official visits. These are skills that, once acquired, empower individuals to take control of their living situation. The critical takeaway is that enduring an extra 10-15 years of work simply to afford a higher cost of living in an undesirable location is a far greater "hassle" than dedicating a few weeks to planning and executing a strategic move to a better, more affordable place.

The Future of FIRE: Adaptation and Resilience

Ultimately, the physical environment—encompassing community, access to nature, urban features, and climate—is arguably one of the most crucial determinants of a happy life. The cost of living is but one factor, albeit a significant one. The true power of the FIRE movement lies in its emphasis on conscious choice and proactive decision-making. By applying diligent thought and effort to housing choices, individuals can optimize their "Nice for the Price" ratio, securing a higher quality of life for a lower financial outlay.

The current economic climate, characterized by fluctuating salaries, increased inflation, and a volatile housing market, does not render the FIRE movement obsolete. Instead, it necessitates adaptation, deeper analysis, and a willingness to embrace change. The fundamental principles of reducing waste, maximizing savings, and strategically allocating resources remain as potent as ever. The discussion around housing, in particular, highlights that financial independence is not solely about accumulating wealth but also about optimizing the cost of one’s most significant recurring expense. By sharing insights and strategies for identifying optimal living environments, the FIRE community continues to evolve, demonstrating its resilience and ongoing relevance in guiding individuals toward a life of greater freedom and purpose. The imperative is not to abandon the principles but to apply them with renewed creativity and a broader geographical scope.