The global financial landscape has undergone a dramatic transformation, as interest rates, after more than a decade of near-zero levels, have surged to their highest points in over two decades. This abrupt shift, orchestrated primarily by central banks aiming to combat persistent inflation, marks a significant departure from the era of ultra-cheap money that defined the post-financial crisis and pandemic periods. The repercussions are now rippling through every facet of the economy, from housing markets and consumer spending to corporate investment and government borrowing, prompting widespread reevaluation of financial strategies.

A Decades-Long Era Concludes

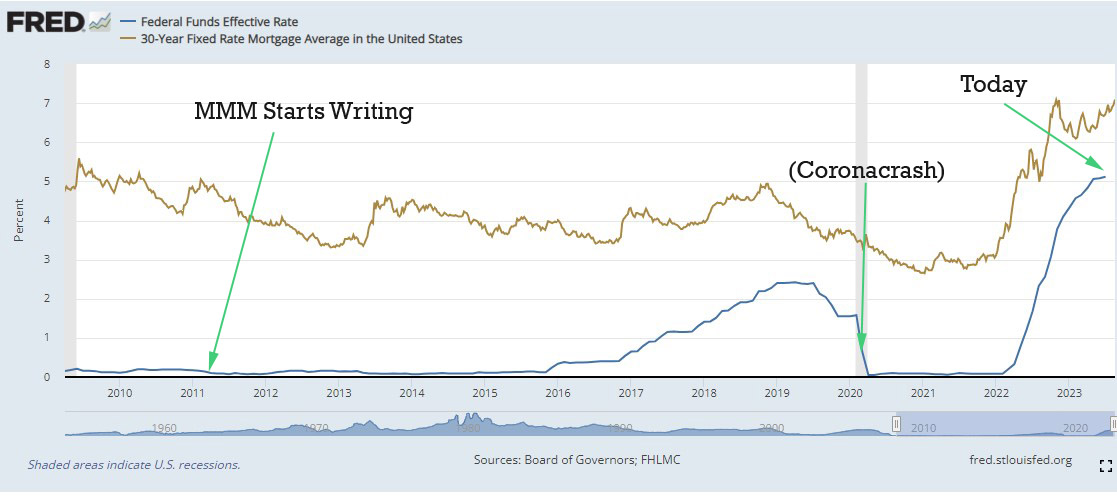

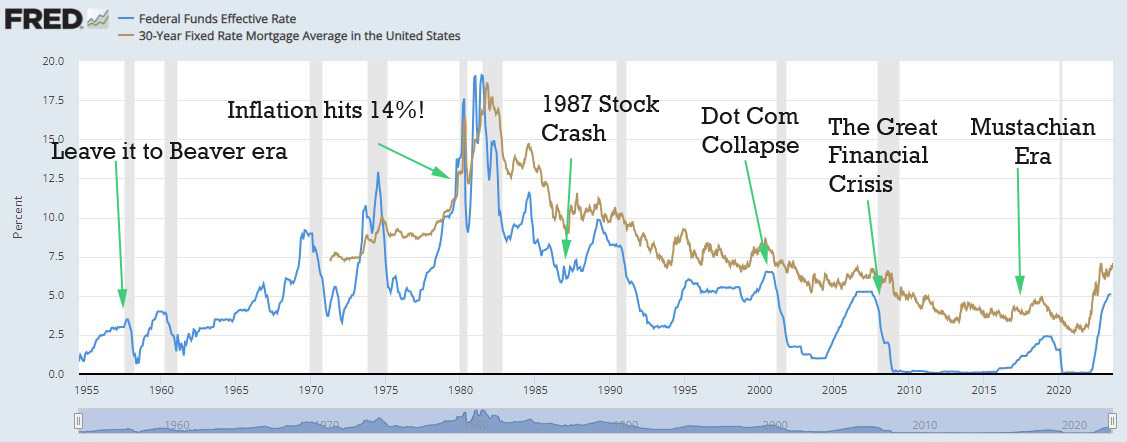

For roughly fourteen years, since the aftermath of the 2008 global financial crisis and extended through the COVID-19 pandemic, interest rates in many major economies, particularly the United States, hovered at historically low levels. The Federal Reserve, like many central banks, aggressively cut its benchmark federal funds rate to near zero (0.00-0.25%) to stimulate economic recovery, encourage borrowing, and avert deflationary spirals. This policy, often referred to as "quantitative easing," injected vast amounts of liquidity into the financial system, making credit exceptionally cheap for consumers and businesses alike.

This prolonged period of easy money fostered an environment of robust economic growth. Mortgages became more affordable, fueling a significant boom in housing markets as demand outstripped supply. Businesses found it inexpensive to borrow for expansion, leading to increased investment, job creation, and the proliferation of new ventures. The accessibility of capital spurred innovation and consumption, contributing to an extended period of prosperity characterized by rising asset prices and generally stable employment.

However, the very success of these policies, coupled with unprecedented fiscal stimulus during the pandemic and subsequent supply chain disruptions, eventually led to an unforeseen challenge: rampant inflation. By early 2021 and accelerating into 2022, consumer prices began to climb at rates not seen in forty years, far exceeding central banks’ target of around 2%. This surge in inflation, driven by "too much money chasing too few goods," necessitated a dramatic policy reversal.

The Federal Reserve’s Aggressive Tightening Cycle

Recognizing the urgent need to rein in escalating prices, the Federal Reserve, under Chairman Jerome Powell, began an aggressive monetary tightening cycle in March 2022. The federal funds rate, which had been held at near zero, was systematically increased across eleven consecutive meetings, reaching a target range of 5.25-5.50% by July 2023. This rapid succession of hikes aimed to cool down the economy by making borrowing more expensive, thereby reducing demand and bringing inflation back towards the target.

This policy shift represents the fastest pace of rate increases since the early 1980s, fundamentally altering the economic landscape. The immediate and most visible impact has been on borrowing costs for consumers and businesses. Mortgage rates, for instance, which had dipped below 3% for a 30-year fixed loan during the pandemic, soared to over 7% by mid-2023, making homeownership significantly less affordable for many. Similarly, interest rates on credit cards, auto loans, and business lines of credit have all seen substantial increases.

Economic Impacts Across Sectors

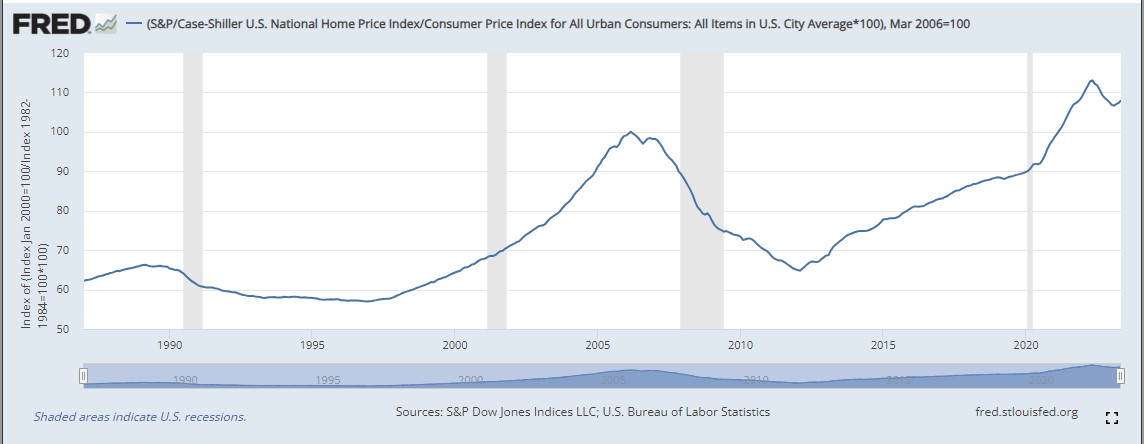

The higher cost of borrowing has initiated a broad economic slowdown. In the housing market, demand has cooled considerably, leading to a reduction in sales volume and, in some areas, a moderation or even decline in home prices. Potential homebuyers are either priced out or choosing to wait for more favorable conditions, while existing homeowners with low fixed-rate mortgages are less inclined to sell, contributing to a persistent inventory shortage in certain segments.

Corporate investment has also slowed as companies face higher capital costs. Many businesses have scaled back expansion plans, leading to reduced hiring and, in some cases, significant layoffs. Tech giants like Meta (Facebook) and Amazon, which had rapidly expanded during the low-rate era, announced tens of thousands of job cuts in late 2022 and early 2023, signaling a broader adjustment in corporate strategies.

The banking sector also experienced notable stress. The rapid rise in interest rates devalued long-dated bonds held by many financial institutions, leading to significant unrealized losses. This vulnerability, combined with concerns over deposit concentration and management practices, contributed to a "miniature banking crisis" in March 2023, with the high-profile collapses of Silicon Valley Bank and Signature Bank. These events triggered broader fears of financial contagion, prompting swift intervention from regulators to stabilize the system.

Despite these challenges, official economic data presents a nuanced picture. While certain sectors have experienced contraction, the broader labor market has remained remarkably resilient. The unemployment rate has consistently hovered near 50-year lows (e.g., around 3.5-3.8% in mid-2023), confounding many economists’ predictions of a significant slowdown. Gross Domestic Product (GDP) growth, while decelerating, has largely avoided a deep recession. Consumer spending, though showing signs of moderation, has also remained robust, underpinned by strong wage growth and accumulated savings. This resilience has led some to describe the current period as a "soft landing" or a "digestive pause" for an economy that had previously consumed too much "sugar" in the form of easy money.

Investment Strategies in a High-Rate Environment

For individual investors, the shift in interest rates necessitates a reevaluation of financial strategies, though core principles often remain unchanged.

- Stock Market Volatility vs. Long-Term Growth: The stock market has experienced increased volatility. From its peak in early 2022, the overall U.S. market saw a significant correction, followed by a partial recovery. While some investors may be tempted to "time the market" by selling during downturns, financial advisors and historical data consistently caution against this approach. Long-term investing in diversified index funds remains a cornerstone strategy, as markets historically recover and achieve new highs over extended periods. The current "discount" on stock prices can be seen as an opportunity for long-term accumulators.

- The Allure of Fixed Income: With interest rates on savings accounts, money market funds, and bonds offering yields of 4.5% or more, fixed-income investments have become considerably more attractive than during the low-rate era. This offers a relatively low-risk option for parking cash or diversifying portfolios. However, for growth-oriented investors, the potential long-term returns from equities, even factoring in current market dips, typically outweigh those from fixed income over decades. The decision often involves balancing risk tolerance, time horizon, and specific financial goals.

- Debt Management: Higher interest rates make carrying consumer debt (credit cards, personal loans) significantly more expensive. Prioritizing the payoff of high-interest debt becomes even more critical. For those with adjustable-rate mortgages or contemplating new loans, understanding the implications of current and potentially future rate movements is essential.

The Housing Market: A Complex Outlook

The trajectory of housing prices remains a central concern. While higher mortgage rates are designed to cool demand and potentially reduce prices, several factors complicate this outlook:

- Construction Costs: Despite technological advancements that could theoretically lower building costs, the actual expense of labor, materials, and land remains substantial.

- Existing Supply Constraints: A persistent shortage of housing stock in many desirable areas continues to underpin prices. Many homeowners with low fixed-rate mortgages are reluctant to sell, further limiting available inventory.

- Regulatory Hurdles and Zoning Restrictions: Local zoning laws, lengthy approval processes, and stringent building codes in many municipalities significantly increase the cost and time required for new construction, hindering supply growth. This "Not In My Backyard" (NIMBY) phenomenon often prevents denser, more affordable housing from being built.

Economists are divided on the future of housing prices. While some predict a significant correction, perhaps a 10-25% decline from peak levels (bringing prices back to around 2020 levels), others anticipate a period of stagnation where prices remain flat for several years, effectively becoming cheaper relative to rising incomes and inflation. Regional variations are also critical, with some markets experiencing sharper adjustments than others.

When Will Interest Rates Decline?

A common question is when interest rates might revert to lower levels. Historically, current rates are not exceptionally "high" but rather closer to the long-term average seen over the past seventy years. The era of near-zero rates was an anomaly, not the norm.

The future path of interest rates is largely dependent on the Federal Reserve’s assessment of inflation and economic growth. Rates will likely begin to decline when the Fed observes sustained evidence of low inflation, coupled with signs of a significant economic slowdown or rising unemployment. As of late 2023, while inflation has moderated, it remains above target, and the labor market continues to show strength, leading the Fed to maintain a cautious stance.

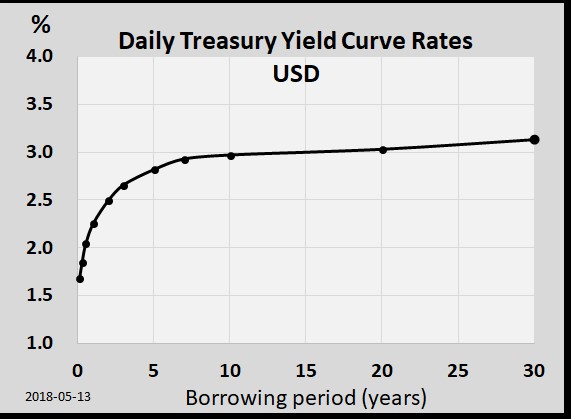

A key indicator watched by market participants is the U.S. Treasury Yield Curve. Traditionally, long-term bonds offer higher yields than short-term ones, compensating investors for locking up their money for longer. However, the current environment features an "inverted yield curve," where short-term rates (e.g., 1-year Treasury bonds at 5.4%) are higher than long-term rates (e.g., 10-year Treasury bonds at 4.05%). This inversion suggests that bond buyers anticipate future interest rate cuts, often in response to an impending economic slowdown or recession. Historically, an inverted yield curve has been a remarkably accurate predictor of recessions, preceding ten out of the last eleven in the past 75 years.

Based on this, market analysts generally forecast that interest rates could begin to decline within the next 12-24 months, potentially accompanied by some form of economic contraction. However, the exact timing and magnitude remain subject to economic data and geopolitical developments.

The Ultimate Strategy: Financial Resilience

Amidst the volatility and uncertainty, a fundamental principle of financial resilience emerges: reducing reliance on debt and cultivating substantial savings. For individuals who own their homes and cars outright, the fluctuations in interest rates on mortgages or auto loans become largely irrelevant. This position of financial strength allows for greater peace of mind and the flexibility to seize opportunities.

Building a robust emergency fund and maintaining a healthy savings rate enables individuals to navigate economic shifts without undue stress. It empowers them to make strategic decisions, such as pouncing on a favorable investment opportunity or a property that becomes available at a reasonable price, without being constrained by prevailing interest rates or credit availability.

In essence, while interest rate changes profoundly impact the broader economy, personal financial stability is ultimately more influenced by individual choices in earning, saving, spending, and living within one’s means. By prioritizing a lean, efficient lifestyle and building a strong financial foundation, individuals can ensure that the "smaller issues" of interest rate shifts remain mere ripples on the surface, rather than overwhelming waves.