As the United States enters another pivotal election cycle, the national discourse inevitably shifts towards the state of the economy, a perennial battleground for political candidates. While citizens are encouraged to engage in research and cast informed votes, the highly charged political rhetoric surrounding economic performance often obscures factual realities. This year, the debate has become particularly pronounced, with competing parties presenting vastly different interpretations of the nation’s financial health, frequently appealing to emotion rather than sound economic principles.

The Current Economic Landscape: A Data-Driven Overview

Contrary to certain political narratives, the U.S. economy currently exhibits remarkable strength across several key indicators. Official data consistently points to a robust labor market, with unemployment rates hovering at historic lows not seen in decades. For instance, recent figures indicate a national unemployment rate around 3.8%, a level that signifies near-full employment and strong demand for labor. This favorable employment picture means that more Americans are working, and businesses are actively seeking talent, leading to increased household income and consumer spending.

Furthermore, economic growth, as measured by Gross Domestic Product (GDP), has shown resilience, expanding even in the face of global uncertainties. While precise quarterly figures fluctuate, the overall trend suggests a healthy, expanding economy. The recent period of elevated inflation, often cited by critics as a sign of economic distress, is, in an economic context, largely understood as a consequence of strong demand outpacing supply, particularly in the wake of unprecedented fiscal stimulus and supply chain disruptions during the COVID-19 pandemic. To curb this inflationary pressure, the Federal Reserve judiciously implemented a series of interest rate hikes, a standard monetary policy tool designed to cool down an overheating economy and bring inflation back to its target rate, which it has largely succeeded in doing, with inflation now moderating to around 2.4%.

The Discrepancy: Public Perception vs. Reality

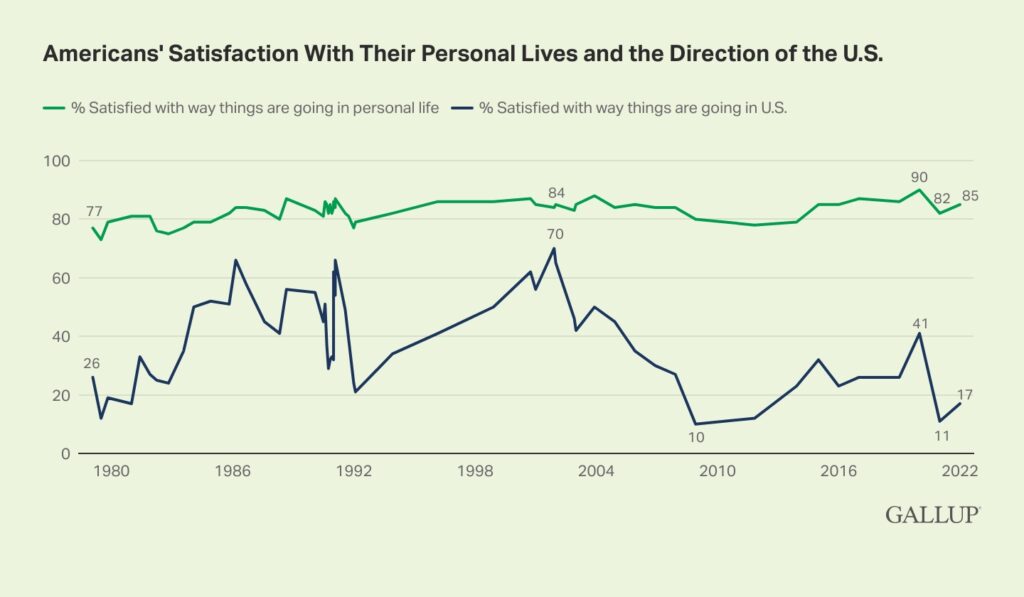

Despite the objectively strong economic indicators, there exists a significant disconnect between official data and public perception. A recent Gallup poll highlights this paradox: while a substantial majority of Americans (approximately 85%) report personal financial well-being, only a small fraction (around 17%) believe the national economy is performing well. This statistical incongruity suggests that individuals attribute their personal financial success to individual effort or good fortune rather than a generally favorable economic environment.

This widespread misperception is not accidental; it is frequently exacerbated by the current political climate and the pervasive influence of social media. In an era where information—and misinformation—travels at unprecedented speeds, emotionally charged narratives can quickly overshadow complex economic truths. Politicians often exploit this gap, framing positive economic data in a negative light or attributing unrelated issues to the current administration to sway undecided voters. This manipulation of public sentiment undermines informed decision-making and fosters an environment where economic literacy is increasingly vital. Understanding the true mechanisms of the economy empowers citizens to discern fact from fiction and make more sound financial choices, individually and collectively.

Deconstructing Economic Myths: Political Narratives Under Scrutiny

In the current election cycle, several persistent economic myths are being propagated by political figures. A critical examination reveals the inaccuracies underlying these narratives:

Myth 1: The President Controls the Economy

A prevalent theme in political campaigns is the tendency for opposition parties to blame the sitting president for economic downturns, while incumbent administrations readily claim credit for periods of prosperity. This narrative oversimplifies the intricate dynamics of the U.S. economy. The American economy, a colossal and largely free-market system, is far too vast and complex for any single individual, including the President, to exert direct, absolute control.

The U.S. economy, representing roughly 25% of global GDP, is intrinsically linked to and influenced by the remaining 75% of worldwide economic activity. Global supply chains, international trade agreements, geopolitical events, and the economic performance of other major nations all play significant roles. Domestic economic cycles, characterized by periods of "irrational exuberance" (like the 2007 housing boom) followed by fear and pessimism (such as the 2008-2012 financial crisis), are largely driven by market forces, investor sentiment, and consumer behavior. While government policies, including fiscal measures like tax rates and regulatory frameworks, do have an impact, their effects are often delayed, indirect, and difficult to isolate from other variables. The President, in essence, is akin to a captain steering a massive ship through unpredictable global waters; they can adjust the rudder, but the vessel’s movement is heavily influenced by tides, currents, and storms beyond their immediate control.

Myth 2: The President’s Hand on Interest Rates

Another common misconception is the belief that the President can unilaterally dictate interest rates. Candidates often express sympathy for middle-class Americans struggling with higher borrowing costs on mortgages, car loans, and credit cards, promising to "fight" to lower rates. Some even suggest direct intervention in the Federal Reserve’s operations, threatening its independence.

In reality, interest rates in the U.S. are primarily determined by the Federal Reserve, an independent central bank designed to operate free from political influence. This independence is crucial for effective monetary policy. The Federal Reserve’s mandate is to maximize employment and maintain price stability (i.e., control inflation). It achieves this through adjusting the federal funds rate, which influences other interest rates across the economy. When the economy slows or unemployment rises, the Fed can lower rates to stimulate borrowing and investment. Conversely, when the economy overheats and inflation accelerates, the Fed raises rates to cool demand. Placing this powerful tool directly in the hands of a sitting president would risk politicizing monetary policy, potentially leading to short-sighted decisions driven by electoral cycles rather than long-term economic health, a scenario often observed in countries with less independent central banks.

Myth 3: Inflation’s True Impact and Political Promises

The narrative that recent inflation has uniformly "made life harder for Americans" and that a president can "magically reverse it" is deeply flawed. The post-COVID inflation spike was a complex phenomenon, resulting from a confluence of factors: supply chain disruptions (factory closures, remote work), robust demand fueled by government stimulus, and historically low interest rates. These transient factors have largely dissipated, and inflation has significantly receded from its peak of over 9% in mid-2022 to a more stable 2.4%.

Crucially, while prices did rise, so did wages. Data indicates that since 2019, average wages have increased by approximately 21%, outpacing the overall rise in consumer prices (around 19%). This means that, on average, American workers’ purchasing power has actually increased, leaving them better off than before the inflationary period. The political promise to "bring prices back down" is not only unrealistic (deflation is generally harmful to an economy) but also misrepresents the current economic reality where higher wages have compensated for higher prices.

A related "bonus dumbness" often heard is the blame placed on "greedy corporations" for increasing prices to hoard profits ("greedflation"). While businesses always seek to maximize profits, competitive markets typically prevent widespread, sustained price gouging without underlying economic reasons. In-depth analyses, such as one by NPR on grocery prices, have shown that corporate profit margins in sectors often accused of "greedflation" did not significantly increase during the recent inflationary period, indicating that price increases were largely driven by higher input costs and demand, not excessive corporate avarice.

Myth 4: Presidential Influence on Housing Dynamics

Housing affordability has become a critical issue, with both home prices and rents rising faster than general inflation and wages over the past decade. Despite this, political solutions often proposed by candidates, such as first-time homebuyer subsidies or schemes to reduce interest rates, risk exacerbating the problem. Such measures, while seemingly beneficial, primarily boost demand without addressing the fundamental issue: insufficient housing supply.

The true solution lies in increasing the availability of housing. This requires tackling systemic barriers that hinder construction. These include streamlining and accelerating the permitting process, reducing onerous and expensive building codes, reforming or eliminating restrictive suburban-style zoning laws (e.g., single-family zoning, minimum lot sizes, excessive setback requirements, and mandated parking minimums), and limiting the disproportionate influence of NIMBY (Not In My Backyard) groups who often block development in their communities. By reducing the regulatory burden and increasing flexibility for homebuilders, the cost of construction could be significantly lowered, leading to a more abundant and affordable housing market, a change that no single president can enact without broader legislative and local government cooperation.

Myth 5: Gas Prices as a Political Barometer

Gasoline prices are a perpetual talking point in elections, often framed as a direct reflection of presidential policy and an indicator of economic hardship. This fixation is increasingly anachronistic. On an inflation-adjusted basis, gasoline prices today ($3-4 per gallon) are remarkably similar to what they were in the 1950s.

Furthermore, despite their visibility, gasoline costs constitute a relatively small portion of the average household budget—around 2.5% of disposable income. The far greater financial burden of car ownership comes from depreciation, insurance, maintenance, and financing, yet these are rarely discussed with the same fervor. Most significantly, the premise of gasoline’s importance is rapidly becoming obsolete. Electric vehicles (EVs) offer a superior, more cost-effective alternative, often being cheaper to purchase (especially used models) and significantly less expensive to fuel and maintain. The continued political focus on gasoline prices ignores the technological advancements and economic efficiencies offered by modern transportation, akin to debating the price of Kodak film in the age of digital photography.

Myth 6: The Economy is Something We Should Even Worry About

Perhaps the most profound misconception is the pervasive belief that economic growth and accumulation of wealth beyond a certain point inherently lead to greater happiness and well-being. While hard work and innovation are valuable pursuits, society, particularly in developed nations like the U.S., passed the point of "enough" decades ago. The complaints about economic hardship from segments of the American middle class often resemble a feast-goer lamenting the lack of one more flavor of dessert, rather than genuine deprivation.

Income and wealth inequality are undeniable issues that warrant attention and a progressive tax system to foster a more equitable, and often more peaceful and happy, society. However, studies consistently show that beyond a certain income threshold, increased wealth does not correlate with increased happiness. True well-being is more closely tied to mindset, community, purpose, and life skills than to a larger paycheck. If politicians genuinely prioritized national happiness and welfare, their rhetoric would focus on principles that foster contentment and resilience, rather than pandering to material desires or narrow economic interests.

The Broader Implications of Economic Misinformation

The constant stream of economic misinformation during an election year has far-reaching consequences. It erodes public trust in institutions, including government and traditional media. It can lead voters to support policies that are economically unsound or counterproductive, driven by emotional appeals rather than data-driven reasoning. For instance, pressuring the Federal Reserve to lower rates when inflation is high, or subsidizing housing demand without increasing supply, can lead to economic instability or exacerbate existing problems. Moreover, a misinformed electorate struggles to hold leaders accountable for genuine economic performance versus manufactured narratives.

The Path Forward: Informed Citizenship and Fact-Based Discourse

In an environment saturated with political spin, the onus falls on citizens to cultivate economic literacy and critical thinking. Resources that present factual data without partisan bias are invaluable. Initiatives like "USA Facts," spearheaded by former Microsoft CEO Steve Ballmer, offer a refreshing approach by compiling and presenting objective economic data, allowing individuals to form their own conclusions based on evidence. Such platforms demonstrate that a fact-based discourse on the economy is possible and desperately needed.

Ultimately, while the electoral process necessitates engagement, an understanding of the true drivers and indicators of economic health allows individuals to filter out political noise. Casting an informed vote is essential, but equally important is the ability to disengage from the constant barrage of political rhetoric and focus on one’s "circle of control" – managing personal finances, investing wisely, and contributing to one’s community – regardless of who occupies the White House. The goal should be not just to elect leaders, but to foster a society that understands its economic realities and pursues genuine well-being.