The landscape of global financial services is undergoing a fundamental transformation where risk, compliance, and governance have migrated from the peripheral back-office to the strategic center of institutional operations. As the industry grapples with an increasingly complex regulatory environment and the rapid integration of artificial intelligence, these functions—once dismissed as administrative necessities—are now recognized as critical drivers of competitive advantage and scalability. At the FinovateSpring 2026 conference, a select group of innovators demonstrated that the future of banking lies in the transition from reactive, manual oversight to proactive, automated systems that harmonize safety with innovation.

This shift comes at a pivotal moment for the financial sector. According to recent industry reports, global spending on regulatory technology (RegTech) is projected to exceed $130 billion by the end of 2026, a significant increase driven by the need for real-time monitoring and the mitigation of sophisticated cyber threats. Financial institutions are no longer merely looking for tools to satisfy auditors; they are seeking integrated frameworks that allow them to launch products faster, manage credit risk with higher precision, and protect consumer data across fragmented digital channels.

The Evolution of Finovate and the 2026 Regulatory Mandate

Finovate has long served as a barometer for the fintech industry’s priorities. While previous iterations of the conference focused heavily on user experience (UX) and front-end "neobank" aesthetics, the 2026 showcase reflects a more mature industry focused on infrastructure and resilience. The timeline leading up to this year’s event has been marked by a series of global regulatory shifts, including the full implementation of updated Basel III standards and stricter oversight of AI-driven decisioning by the Consumer Financial Protection Bureau (CFPB) and the European Banking Authority.

The emergence of these five companies at FinovateSpring 2026 highlights a broader trend: the "API-fication" of compliance. By embedding governance directly into the software stack, banks can now achieve a level of transparency and agility that was previously impossible under legacy systems.

CRIF: Bridging Tradition and Algorithmic Transparency

Headquartered in Italy and boasting a legacy dating back to 1988, CRIF represents the successful marriage of traditional credit bureau expertise with cutting-edge decisioning technology. At FinovateSpring, CRIF demonstrated how its platform enables lenders to design and deploy credit strategies with unprecedented speed. The company’s focus on "explainable AI" addresses one of the primary concerns of modern regulators: the "black box" problem of automated lending.

The CRIF platform offers a no-code strategy design environment, allowing business users to adjust risk parameters without extensive IT intervention. This is supported by real-time simulations and Key Performance Indicator (KPI) validation, ensuring that any change in lending strategy is both profitable and compliant before it goes live. In an era where credit unions and fintechs must compete with global Tier-1 banks, CRIF’s ability to provide a single framework for data, analytics, and governance provides a scalable path for institutions of all sizes to modernize their risk management protocols.

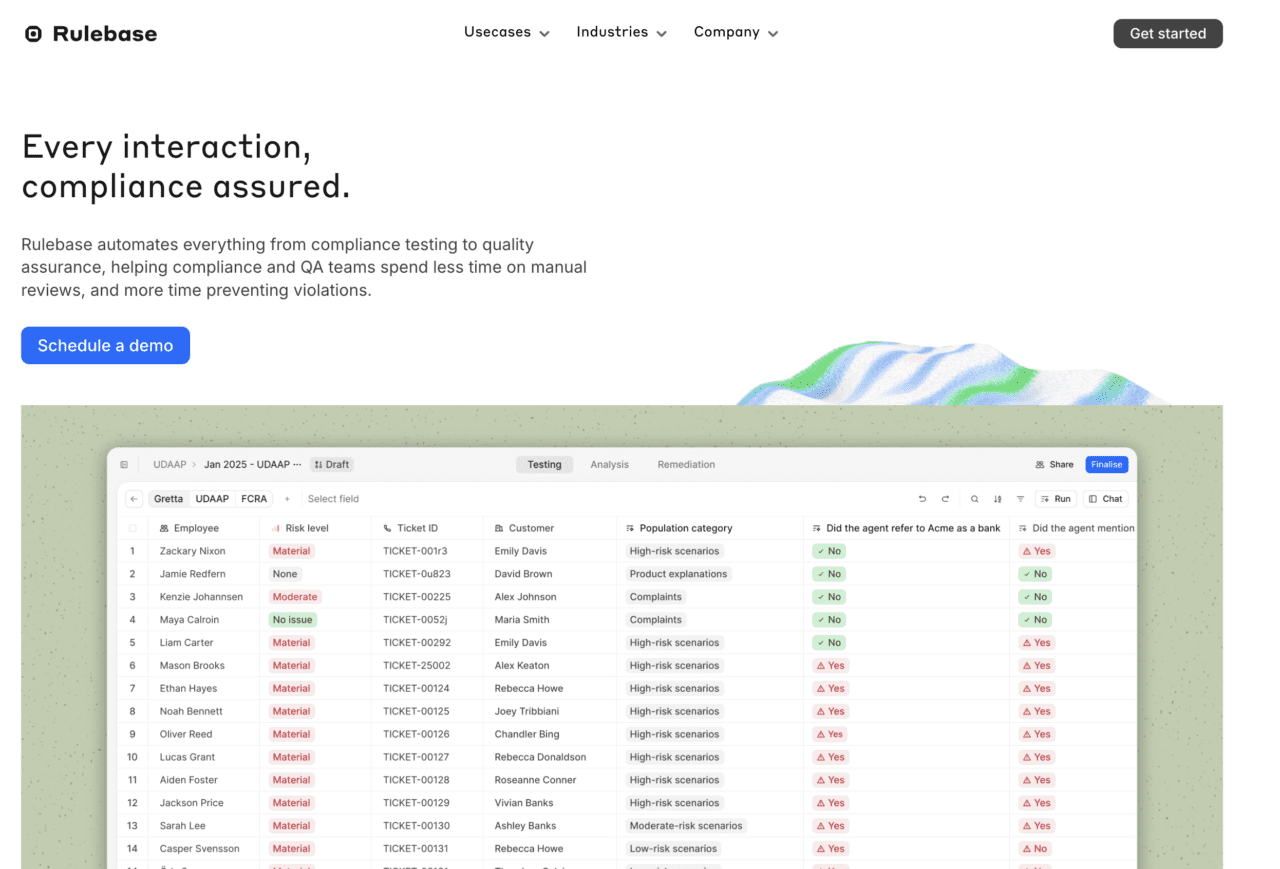

Rulebase: Automating the Quality Assurance Lifecycle

Founded in 2025, the New York-based startup Rulebase has quickly moved to fill a critical gap in the compliance market: the need for continuous, automated testing. Historically, compliance quality assurance (QA) has relied on periodic spot-checks and manual audits, a method that is increasingly insufficient in a high-velocity digital economy.

Rulebase’s platform continuously monitors customer interactions and internal workflows, detecting potential violations as they occur. By generating audit-ready evidence in real-time, the platform reduces the "compliance tax" on human capital, allowing specialized staff to focus on high-risk anomalies rather than routine monitoring. The company’s presence at Finovate underscores a growing demand for tools that move beyond "point-in-time" checks to a model of "always-on" compliance.

Winnow: Transforming Legal Research into Actionable Intelligence

Compliance is often hindered not by a lack of will, but by the sheer volume of regulatory data. Winnow, founded in 2018 and based in Anaheim, California, addresses this by streamlining the research process. The platform replaces fragmented manual searches with attorney-reviewed regulatory guidance tailored to the specific needs of the institution.

In the current environment, where state and federal laws can often overlap or conflict, Winnow provides a centralized repository of legal intelligence. This allows financial institutions to understand their obligations in minutes rather than weeks. By reducing the time and cost associated with traditional legal research, Winnow enables banks to allocate resources toward execution and customer service, effectively turning regulatory hurdles into manageable operational tasks.

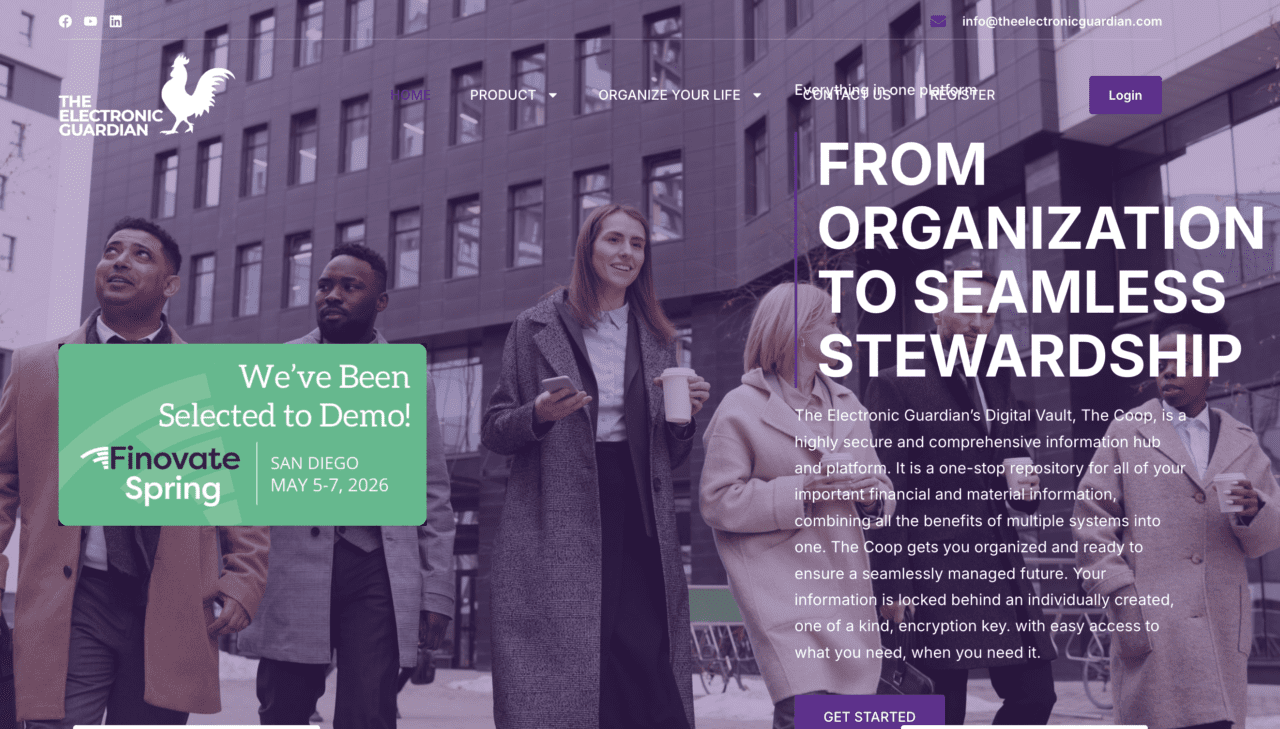

The Electronic Guardian: Security through Estate Organization

The Electronic Guardian offers a unique perspective on risk by focusing on the consumer’s long-term financial security. Its flagship platform, "The Coop," is a digital repository designed for the secure organization and eventual transfer of critical financial and personal information. This "at rest" recoverability ensures that sensitive data remains protected by private encryption while remaining accessible for legacy planning and asset continuity.

For banks and insurance providers, offering a tool like The Electronic Guardian is a strategic move to increase customer "stickiness" and build trust. In a world where identity theft and digital asset loss are rising concerns, providing a secure vault for estate inventory positions the financial institution as a lifelong partner in the client’s financial journey. Founded in 2019 in Pittsburgh, the company’s success at FinovateSpring 2026 indicates a growing interest in "wellness-based" fintech solutions that prioritize data sovereignty.

Model IQ: Quant-Driven Governance for a Model-Reliant Industry

As financial institutions become more dependent on complex mathematical models for everything from fraud detection to capital stress testing, the risk of "model failure" has become a systemic concern. Model IQ, developed by Kevin D. Oden & Associates, provides an automated platform specifically designed to manage this risk.

Based in San Francisco and founded in 2018, Model IQ was built by quants to address the stringent requirements of SR 11-7, FDIC, and NCUA guidelines. The platform automates the entire model lifecycle, from development and validation to ongoing monitoring. By bringing structure and consistency to model risk management, Model IQ allows regional banks and credit unions to maintain the same level of oversight as their larger counterparts, ensuring that their automated systems remain accurate, ethical, and compliant with federal mandates.

Supporting Data: The Rising Cost of Non-Compliance

The urgency for the solutions showcased at FinovateSpring 2026 is underscored by the rising financial penalties for regulatory failures. In 2024 and 2025, global banking fines related to Anti-Money Laundering (AML), Know Your Customer (KYC), and data privacy violations reached record highs. For mid-sized institutions, a single regulatory fine can wipe out an entire year’s profit margin.

Furthermore, a 2025 survey of bank executives revealed that over 65% of institutions still rely on spreadsheets or legacy on-premise software for at least one core compliance function. This "governance gap" is what CRIF, Rulebase, Winnow, and Model IQ aim to close. The transition to cloud-native, AI-augmented governance tools is no longer a luxury but a prerequisite for operational survival.

Industry Reactions and Expert Analysis

Analysts attending the event noted that the common thread among these companies is the reduction of operational friction. "We are seeing the end of the ‘Department of No,’" remarked one fintech consultant during a panel discussion. "Modern governance tools are designed to say ‘yes’ more often by providing the data and transparency needed to take calculated risks."

Official responses from participating banks suggest a high level of interest in "modular compliance." Rather than replacing an entire core banking system, institutions are looking for specialized "plug-and-play" solutions like Winnow for legal research or Rulebase for QA. This modular approach allows for faster integration and a quicker return on investment (ROI).

Broader Impact and Future Implications

The long-term implications of the innovations seen at FinovateSpring 2026 extend beyond the balance sheet. As banks adopt these proactive governance frameworks, the entire financial ecosystem becomes more resilient. Automated compliance reduces the likelihood of systemic failures, while transparent decisioning tools like those offered by CRIF help to mitigate algorithmic bias, promoting financial inclusion.

Moreover, the rise of digital estate planning through platforms like The Electronic Guardian reflects a shift in consumer expectations. Customers now expect their financial institutions to safeguard not just their money, but their entire digital legacy.

In conclusion, the 2026 FinovateSpring showcase has demonstrated that the future of fintech is not just about the "fin," but increasingly about the "tech" that governs it. By embracing automation, AI-driven analytics, and centralized legal intelligence, financial institutions can transform risk and compliance from a burden into a springboard for growth. As the volume and velocity of global financial data continue to accelerate, the companies highlighted this year provide the essential roadmap for navigating the complexities of the modern regulatory landscape.