The financial trajectory of mid-career professionals in the public sector has become a focal point of economic analysis as rising living costs and consumer debt levels intersect with the traditional stability of government employment. In central Connecticut, a case study involving two 34-year-old state employees, Brian and Michael, illustrates the complexities of modern wealth building. Despite a combined gross household income of approximately $167,544, the couple faces significant hurdles, including nearly $30,000 in consumer debt and the absence of real estate equity. Their situation highlights a broader national trend where high-earning millennial households struggle to transition from high-end rentals to permanent homeownership due to short-term financial liabilities and shifting market conditions.

Demographic and Professional Profiles

Brian and Michael represent a specific demographic of the New England workforce: the "stable-income, high-liability" household. Brian serves as a quality assurance manager for a state-run hospital, a role that provides substantial benefits, including a pension and lifetime healthcare—increasingly rare commodities in the private sector. Michael operates as a project coordinator for a state behavioral health agency, supplemented by secondary income as a disability leadership coordinator and advocate.

Their professional roles are deeply intertwined with their personal histories; Michael is a brain injury survivor, which informs his advocacy work, while Brian’s career path has transitioned from the corporate sector to non-profit and finally to public service. This shift toward the public sector has secured their long-term retirement framework but has left them with immediate liquidity challenges and a perceived lag in traditional "adulting" milestones compared to their peers.

Economic Context: The Connecticut Rental and Utility Landscape

The couple’s financial pressure is exacerbated by the specific economic climate of Connecticut. In late 2022 and early 2023, the state’s rental market experienced significant volatility. Brian and Michael were forced to relocate from a $945-per-month studio to a $2,000-per-month luxury apartment in a refurbished industrial mill. This 111% increase in housing costs is reflective of the broader "mill conversion" trend in New England, where historic industrial spaces are repurposed into high-end residential units, often at the expense of local affordability.

Furthermore, the couple’s expenditure on electricity—averaging $235 per month—highlights a localized economic burden. Connecticut consistently ranks among the states with the highest residential electricity rates in the continental United States. According to the U.S. Energy Information Administration (EIA), Connecticut residents often pay significantly above the national average per kilowatt-hour, a factor that complicates the ability of residents to redirect funds toward debt repayment or savings.

Analysis of Debt Structure and Interest Volatility

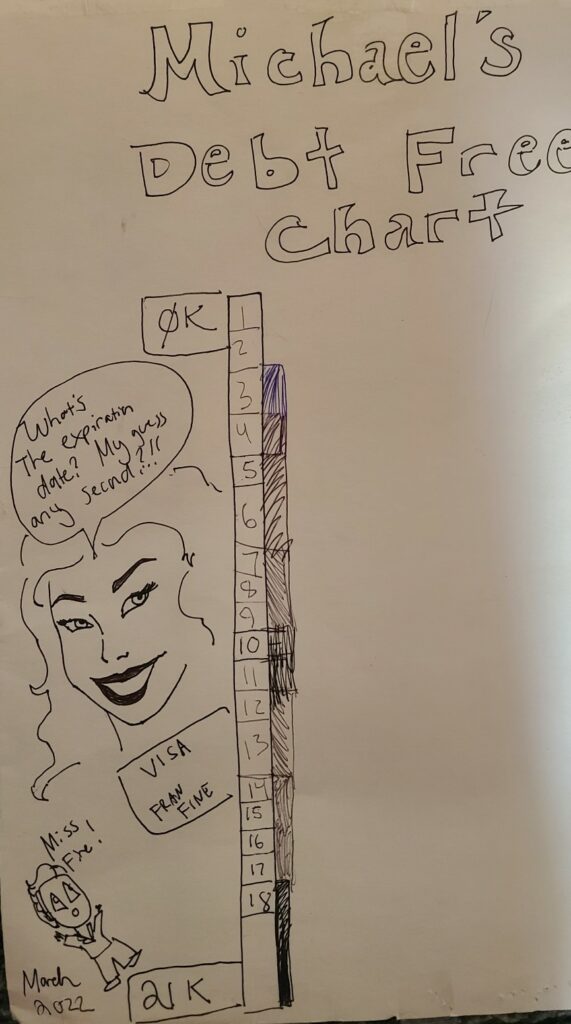

As of late 2023, the household’s total consumer debt stands at $28,259, distributed across three primary credit vehicles. The structure of this debt presents a looming "interest cliff" that necessitates immediate strategic intervention.

- High-Balance Zero-Percent Card: Brian holds a $16,057 balance on a Visa through Sharon Credit Union (SCU), which carries a 0% introductory rate until November 2023. Post-promotion, the rate is set to jump to 17.99%.

- Moderate-Interest Consolidation: Michael maintains a $9,700 balance on a Visa Platinum at 10.99%.

- Low-Balance Promotional Card: Brian has a $2,503 balance at 0.99%, also expiring in November 2023, after which the rate increases to 17.74%.

Financial analysts note that the reliance on 0% interest "teaser" rates is a common strategy for managing large balances, but it carries the risk of significant interest compounding if the principal is not retired before the expiration date. For Brian and Michael, the November deadline serves as a critical pivot point for their net worth.

Asset Portfolio and Retirement Framework

While the couple’s short-term liquidity is strained, their long-term asset base is more robust than their self-assessment suggests. Their total assets are valued at approximately $91,250, though a significant portion is held in illiquid retirement accounts.

Brian’s retirement structure is particularly noteworthy, utilizing what financial experts often call the "Triple Crown" of public sector investing: a 403(b), a 457(b), and a state pension fund. The 457(b) plan offers a distinct advantage for early retirement, as it allows for penalty-free withdrawals upon separation from service, regardless of age—a feature not available in standard 401(k) or 403(b) plans. Brian’s projected pension, estimated at $4,150 per month starting in 2054, provides a guaranteed income floor that mitigates the risks associated with Social Security’s long-term solvency.

Michael’s primary retirement vehicle is a Vanguard 401(k) valued at $36,992, invested in a 2055 Target Retirement Fund. With a 10% personal contribution and a 4% employer match, Michael is maintaining a 14% total savings rate, which aligns with standard recommendations for mid-career professionals.

Strategic Debt Eradication and Cash Flow Optimization

To address the $28,259 debt, a rigorous "spending detox" has been proposed. The current annual net income of $109,455, when weighed against annual expenditures of $96,414, suggests a theoretical surplus of $13,041. However, the couple’s current reporting indicates that much of this surplus is being absorbed by discretionary spending.

The proposed financial restructuring involves categorizing all expenses into three tiers: Fixed, Reduceable, and Discretionary. By eliminating discretionary costs—including "eating out," "home goods," and "non-essential personal care"—the household could theoretically increase their monthly debt repayment capacity to $4,456. At this accelerated rate, the entirety of the $28,259 debt could be retired in approximately 6.5 months.

This "famine" period is designed to prevent the interest rate hikes scheduled for November from significantly eroding their principal payments. Once debt-free, the couple would be positioned to redirect that $4,456 monthly surplus toward an emergency fund and, eventually, a down payment for a home.

The ROI of Advanced Education in the Public Sector

A secondary consideration in the couple’s ten-year plan is Brian’s pursuit of a master’s degree. From a journalistic and economic perspective, the Return on Investment (ROI) for graduate education in the public sector varies wildly by field. In many state government structures, a master’s degree provides a "step increase" or moves an employee into a higher pay grade.

However, analysts caution that unless the degree is a prerequisite for a specific, higher-paying promotion, the opportunity cost—both in tuition and lost time—may outweigh the salary bump. For a household already carrying $28,000 in consumer debt, adding student loans or depleting savings for a degree without a guaranteed salary increase could further delay homeownership goals.

Broader Implications for Millennial Homeownership

The case of Brian and Michael reflects a broader national conversation regarding the "markers of adulthood." The delay in homeownership for high-earning millennials is often attributed to the "avocado toast" trope of frivolous spending, but the data suggests a more complex reality. High entry costs for real estate, the necessity of maintaining two vehicles in suburban Connecticut, and the rising costs of pet care and utilities create a high "burn rate" for even six-figure households.

In Connecticut specifically, the inventory of single-family homes remains tight. For Brian and Michael, the transition from a "luxurious mill apartment" to a rural property with a garden requires a shift from a consumption-based lifestyle to a capital-accumulation mindset. Their success depends not on their income—which is already in the top quintile for their age group—but on their ability to manage the "lifestyle creep" that often accompanies public sector career advancement.

Conclusion and Future Outlook

The financial roadmap for Brian and Michael over the next decade involves a sequence of high-priority actions: immediate debt eradication, the establishment of a six-month emergency fund (estimated at $30,000 to $40,000 based on their fixed costs), and the maximization of tax-advantaged retirement accounts.

By leveraging Brian’s 457(b) and Michael’s 401(k), the couple can significantly reduce their taxable income while building a bridge to an early or comfortable retirement. Their goal of homeownership is attainable within a three-to-five-year window, provided they maintain the discipline to treat their current surplus as capital for investment rather than disposable income. As the Connecticut housing market continues to evolve, their status as state employees with protected benefits provides a level of economic insulation that, if paired with rigorous cash-flow management, ensures a high probability of long-term financial success.