The implementation of financial literacy programs within the domestic sphere has gained significant traction among child development experts, as evidenced by a recent case study involving a Vermont family during the state’s annual county fair season. Utilizing the high-consumerism environment of the traditional agricultural exhibition, the parents—founders of the personal finance platform Frugalwoods—demonstrated a structured pedagogical approach to money management for children aged five and seven. This methodology, centered on a clear distinction between essential needs and discretionary wants, provides a framework for understanding how early exposure to economic principles can shape lifelong financial behaviors.

The Vermont County Fair as a Microcosm of Consumerism

The Vermont county fair, a staple of New England’s agricultural heritage, serves as more than just a venue for livestock exhibitions and community gatherings. For families, it represents a concentrated environment of marketing directed at minors. With an array of sensory stimuli, from "cuddling cows" to the ubiquitous presence of souvenir stands and high-priced concessions, the fair offers a real-world laboratory for financial decision-making.

Observers note that such events often overwhelm the decision-making faculties of young children. However, by treating the fair as a "panorama of consumerism," the subjects of this study utilized the venue to test a pre-established "Family Money Philosophy." This philosophy dictates a rigid boundary: parents provide for all fundamental needs—including shelter, healthcare, nutrition, and educational tools—while the children are responsible for funding all discretionary extras.

Chronology of Financial Instruction: From Labor to Liquidity

The educational process observed in the Vermont household follows a specific chronological progression, beginning with the concept of earned income and moving toward the complexities of debt and independent commerce.

Phase I: The Labor Market and Chore Negotiation

The foundation of the girls’ financial autonomy is a seasonal chore system. Unlike standard allowances, which are often provided regardless of effort, this system mimics a market economy. Chores are categorized into two distinct types:

- Unpaid Daily Responsibilities: These include personal maintenance tasks such as bed-making, room cleaning, and laundry. These are framed as essential contributions to the household collective.

- Paid Service Contracts: These involve tasks that benefit the family unit as a whole, such as organizing kitchen cabinets or clearing communal trash.

A critical component of this phase is the "fair market value" negotiation. For instance, the seven-year-old subject recently negotiated a $10 lump sum for a comprehensive organization of kitchen drawers. This introduces the concept of labor value and the ability to negotiate terms based on the scale of the project.

Phase II: The Reality of Physical Currency Management

Once income is earned, the children are tasked with the physical responsibility of their capital. The study highlighted a "near-crisis" event at a science museum where the seven-year-old misplaced her wallet containing her earned savings. The resolution—approaching a cashier to recover the lost item—served as a primary lesson in the vulnerability of assets and the importance of secure storage.

Phase III: The Debt Experience and the "Unicorn Lesson"

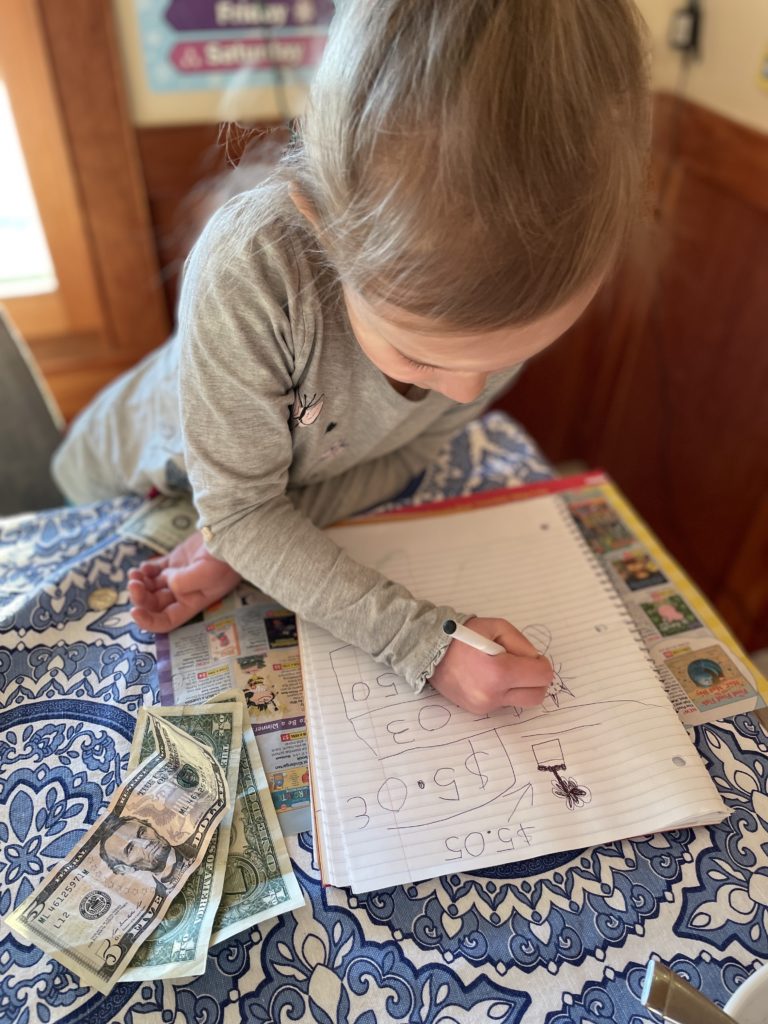

One year prior to the current fair season, a pivotal lesson in credit and debt occurred involving the purchase of a $13 inflatable unicorn. Having only $9 in cash, the elder child was permitted to go into debt to her parents for the remaining $4. The subsequent "debt service" phase—where the child was required to perform chores to pay off the balance without receiving new cash—resulted in a visceral understanding of the "opportunity cost" of debt. The subject noted that working for an item already possessed was significantly less rewarding than working for future capital.

Supporting Data: The Impact of Early Financial Education

Research from the FINRA Investor Education Foundation suggests that individuals who receive financial education early in life are more likely to have higher credit scores and lower rates of delinquency as adults. Furthermore, a study by T. Rowe Price indicated that 75% of parents who talk to their children about money regularly find that their children are more responsible with their belongings.

In the Vermont case, the data is reflected in the children’s evolving spending habits. During the most recent fair and farm visits, the children transitioned from impulsive individual spending to a collaborative model. When faced with a $7 dessert, the two siblings calculated the cost-benefit of splitting the price, requiring them to navigate the mathematical challenge of dividing an odd number in a currency system based on decimals.

Economic Context: The Cost of Childhood "Extras"

The necessity of such education is underscored by the rising costs of child-directed consumer goods. According to the American Farm Bureau Federation and various fair association reports, the cost of "midway" entertainment and concessions has risen by approximately 15-20% over the last three years, largely due to increased labor and ingredient costs.

For a family in the Vermont region, the "Scholastic Book Fair" also serves as a major touchpoint for consumerism. While the parents provide a "house full of books" sourced from libraries and second-hand sales, the school-sanctioned book fair represents a high-pressure marketing environment. By requiring children to use their own chore money for these purchases, the parents force a comparison-shopping mindset: is a new book at full retail price worth the labor equivalent of five hours of chores, or is a library book sufficient?

Official Responses and Psychological Analysis

While there are no official government mandates for "domestic financial literacy," developmental psychologists often weigh in on the "parent-as-bank" model. Dr. David Anderson, a clinical psychologist at the Child Mind Institute, has previously noted that "giving children a sense of agency over their small-scale economic world helps build executive function."

The parental subjects in this Vermont case study emphasized that their goal is to "demystify" money. By explaining that "Mama works and is paid money… which she then uses to buy groceries," the parents are removing the abstraction from the ATM or the credit card. This transparency is designed to reduce "money anxiety" by replacing mystery with a clear, functional equation.

Broader Impact and Future Implications

The long-term goal of this domestic curriculum is the transition from a "cash-and-carry" model to a "savings-and-investment" model. The parents have announced plans to establish a "Bank of Parental Units," which will introduce the concept of compound interest. By offering a high-interest rate on the children’s savings, the parents intend to incentivize delayed gratification—a trait consistently linked to higher socioeconomic success in longitudinal studies like the famous "Stanford Marshmallow Experiment."

Key Takeaways from the Vermont Model:

- Separation of Needs and Wants: Establishes a baseline for budgeting.

- Negotiated Labor: Teaches the value of work and the mechanics of the labor market.

- Controlled Debt: Allows for low-stakes failure, preventing high-stakes financial ruin in adulthood.

- Independent Execution: Encourages children to conduct their own transactions, building confidence in commercial environments.

As the Vermont county fair concludes, the data from this household suggests that the children have moved beyond the "cuddling cows" phase of development and into the "capital management" phase. The elder child’s assessment of her mother’s financial consulting job—noting that meetings are "boring but important"—indicates a budding realization that the adult world of finance is a serious, yet navigable, system.

The implications of this case study suggest that financial literacy is not a subject to be delayed until high school or college. Rather, it is a "scaffolded" education that begins with counting pennies for a farm-stand cupcake and evolves into a sophisticated understanding of debt, interest, and the intrinsic value of labor. For families looking to insulate their children against the pressures of modern consumerism, the Vermont model offers a rigorous, fact-based blueprint for success.