The financial trajectory of middle-income professionals in the current economic landscape is increasingly defined by a paradox of high gross earnings and persistent consumer debt. In central Connecticut, Michael and Brian, both 34, represent a growing demographic of dual-income households that, despite achieving significant career milestones and a combined annual income of approximately $167,544, find themselves navigating the complexities of debt management, rising housing costs, and the pursuit of traditional markers of adulthood. Their situation highlights the broader challenges of "lifestyle creep," the volatility of the Northeastern rental market, and the critical importance of strategic fiscal planning in a high-interest-rate environment.

The Current Financial Landscape: Income vs. Liability

Michael and Brian have spent the last decade building a life together, recently celebrating their 10th anniversary. Michael operates as a project coordinator for a state behavioral health agency and supplements his income as an advocate and disability leadership coordinator. Brian serves as a quality assurance manager for a state-run hospital. Together, they bring home a net annual income of $109,455 after taxes and pre-tax retirement deductions.

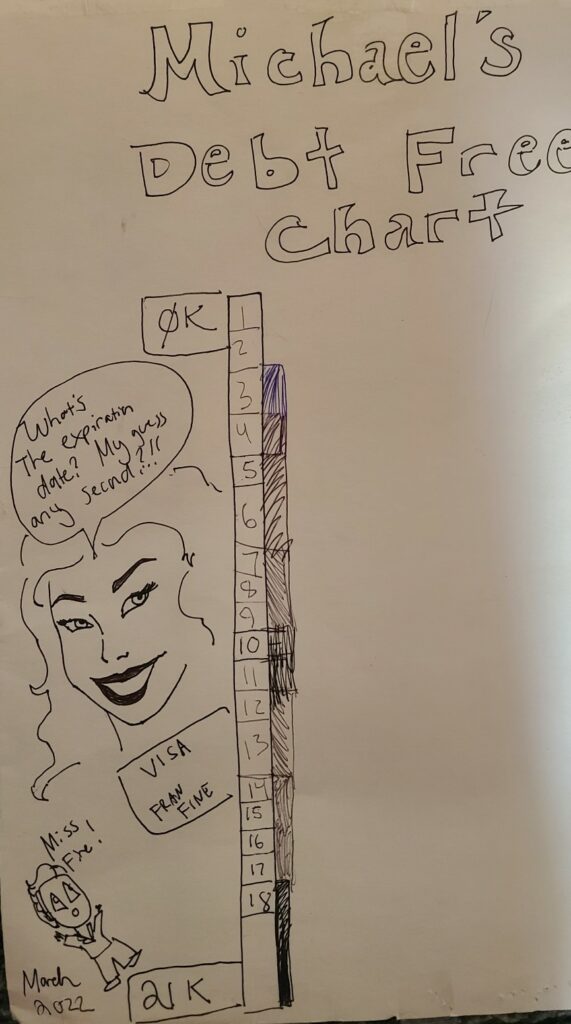

Despite this robust income, the couple is currently burdened by $28,259 in consumer debt. The debt is distributed across several high-interest credit vehicles: a $16,057 balance on an SCU Visa, a $9,700 balance on a Visa Platinum, and a $2,503 balance on a Navy Federal Visa. Much of this debt was accrued during a period of significant life transitions, including a forced relocation and unexpected veterinary expenses. Their financial profile is further characterized by approximately $91,250 in total assets, the majority of which are tied up in retirement accounts such as 401ks, 457bs, and 403bs, leaving them with limited liquid liquidity for immediate goals like homeownership.

A Chronology of Transition: 2022–2023

The couple’s current financial strain is rooted in a series of events that began in late 2022. For eight years, they resided in a 600-square-foot studio apartment in central Connecticut, paying a modest $945 per month. This low overhead allowed for a period of relative financial stability; however, the 2022–2023 rental market necessitated a move.

The transition to a 1,200-square-foot, two-bedroom apartment in a refurbished industrial mill more than doubled their housing costs to $2,000 per month. This relocation coincided with a health crisis involving two new kittens, leading to significant unplanned veterinary bills. The "scramble" to find housing in a competitive market, combined with moving expenses and medical costs for their pets, shifted their focus from saving for a down payment to managing rising credit card balances.

By mid-2023, the couple realized that their previous plan to enter the housing market in late 2023 had been derailed. The move, while providing a more "age-appropriate" and "formal" living space, fundamentally altered their monthly cash flow, leaving them in a cycle of debt repayment that they now seek to break permanently.

Supporting Data: The Connecticut Economic Context

The financial pressure felt by Michael and Brian is mirrored in regional and national data. According to recent housing reports, Connecticut has seen some of the most consistent rent increases in the Northeast, with central Connecticut markets experiencing a lack of inventory that drives prices upward for both renters and buyers.

Furthermore, the couple’s credit card debt is subject to the current federal interest rate environment. With the Federal Reserve maintaining higher rates to combat inflation, the interest on their $28,000 debt—set to jump to between 17% and 18% for several balances in November 2023—represents a significant "leak" in their financial bucket.

Data from the Federal Reserve Bank of New York indicates that total credit card balances in the U.S. surpassed $1 trillion in 2023, with millennials (ages 30–39) seeing some of the sharpest increases in delinquency and balance growth. Michael and Brian’s struggle to balance high-cost living with debt reduction is a localized example of this national trend.

Analysis of Retirement and Career Assets

While the couple’s consumer debt is a pressing concern, their long-term asset base provides a strong foundation. Brian’s employment within the state system grants him access to a "triple crown" of retirement vehicles: a 403b, a 457b, and a state pension. The pension, estimated to provide a monthly payout of $4,150 upon retirement in 2054, is a rare and valuable asset in the modern economy.

However, Michael’s 401k, currently valued at $36,992, and Brian’s various smaller accounts suggest that while they are participating in retirement plans, they have not yet reached the "max-out" phase of investing. Financial analysts often suggest that households in this income bracket should aim to maximize tax-advantaged accounts to reduce their taxable income—a strategy Michael and Brian have yet to fully leverage due to their focus on debt and current spending habits.

Official Responses and Expert Perspectives

Financial consultants, including Liz Frugalwoods, have analyzed the couple’s situation, offering a roadmap that prioritizes immediate debt elimination over other milestones like graduate school or homeownership. The consensus among financial experts for cases such as this involves a three-pronged approach:

- Rigorous Expense Tracking: The couple currently has a $13,000 annual surplus on paper that is not being accounted for in their liquid savings. Experts suggest using digital tools or manual spreadsheets to identify where "phantom spending" is occurring.

- The Spending Detox: To eliminate $28,000 in debt within a six-to-seven-month window, experts recommend a temporary "famine" period. This involves cutting discretionary spending—such as eating out ($200/mo), home goods ($200/mo), and personal care ($180/mo)—to zero until the high-interest liabilities are cleared.

- Emergency Fund Stabilization: With only $9,000 in liquid cash, the couple is one emergency away from further debt. Increasing this fund to cover three to six months of expenses ($24,000 to $48,000) is considered a non-negotiable step before pursuing a home purchase.

Regarding Brian’s consideration of a master’s degree, the journalistic and financial consensus is cautious. In the current labor market, the Return on Investment (ROI) for graduate degrees is under scrutiny. Experts advise that such a move should only be made if there is a "guaranteed, iron-clad correlation" to a significant salary increase, rather than for academic fulfillment alone, especially when debt-free status is the primary goal.

Broader Impact and Implications for the Middle Class

The case of Michael and Brian serves as a cautionary and instructional tale for the modern middle class. It illustrates that a high salary is not a safeguard against financial anxiety if it is not paired with disciplined cash-flow management. The "shame" expressed by both individuals regarding their financial standing is a common sentiment among professionals who feel they have "fallen behind" their peers.

The broader implication is that the traditional markers of adulthood—homeownership, marriage, and career stability—are being redefined by the necessity of aggressive debt management. For Michael and Brian, the path forward requires a shift from a "feast and famine" cycle of spending to a sustainable, moderate lifestyle.

Their story also highlights the value of public-sector employment in providing a safety net through pensions and healthcare, which can offset the lack of real estate equity in the early stages of wealth building. As they work toward their goal of "unlocking the next level of adulting," their progress will depend on their ability to align their daily spending with their long-term values of legacy and independence.

Conclusion: The Path Toward 2033

In ten years, Michael and Brian aim to own a home on a private lot, operate a successful side business, and hold a diversified portfolio of assets. Achieving this vision will require a tactical retreat from discretionary spending in the short term to secure their long-term interests. By addressing their $28,259 debt with the same intensity they applied to Brian’s previous $58,000 student loan payoff, the couple is well-positioned to transform their financial "dreams deferred" into a reality of permanent debt freedom and generational wealth. The transition from a luxury rental to a owned homestead is not merely a matter of income, but a matter of the strategic allocation of every dollar earned in the intervening years.