The global financial technology landscape is currently navigating a pivotal transition where the theoretical potential of artificial intelligence and decentralized finance is being distilled into practical, scalable solutions for everyday users. As the industry prepares for FinovateSpring 2026, scheduled to take place in San Diego from May 5 to May 7, the focus has shifted toward the democratization of finance—a movement aimed at dismantling traditional barriers to credit, education, and international capital flow. While the broader tech sector remains preoccupied with the abstract capabilities of generative AI and blockchain, a specialized cohort of innovators is applying these technologies to resolve the friction points faced by international students, underserved small businesses, and the next generation of retail savers.

This year’s event highlights five specific fintech firms—Crebit Pay, GenAspire, Nextvestment, PROVIDR, and Vine Financial—each representing a different pillar of modern financial evolution. These companies are not merely offering incremental improvements to existing workflows; they are fundamentally reimagining how financial institutions interact with their constituents. From stablecoin-powered cross-border payments that bypass the inefficiencies of legacy correspondent banking to agentic AI platforms that empower loan officers to make faster, data-driven decisions, these innovations signal a move toward a more inclusive and efficient global economy.

A Chronology of Innovation and the Evolution of Finovate

The Finovate conference series has served as a primary barometer for the fintech industry since its inception in 2007. Initially focused on the rise of mobile banking and the first wave of "disruptive" startups, the event has evolved alongside the technological maturity of the sector. By the mid-2010s, the narrative shifted toward "collaboration over competition," as traditional banks began to view fintechs as essential partners rather than existential threats.

The 2026 iteration of FinovateSpring arrives at a time when the "AI hype cycle" is giving way to the "implementation era." Following the explosive growth of large language models in 2023 and 2024, financial institutions spent 2025 conducting rigorous pilot programs and addressing regulatory concerns regarding algorithmic bias and data privacy. The companies debuting in San Diego this year represent the first generation of "post-hype" fintechs—firms built with compliance, security, and real-world utility as their core architectural principles.

The timeline for these five featured firms reveals a concentrated surge in innovation between 2024 and 2025. This period was characterized by a stabilization in the digital asset markets and a maturing of "agentic" AI, which allows software to perform complex multi-step tasks rather than just generating text or images. For instance, PROVIDR and Crebit Pay, both founded in 2025, were born into a regulatory environment that had finally begun to provide clear frameworks for AI underwriting and stablecoin usage, allowing them to scale faster than their predecessors.

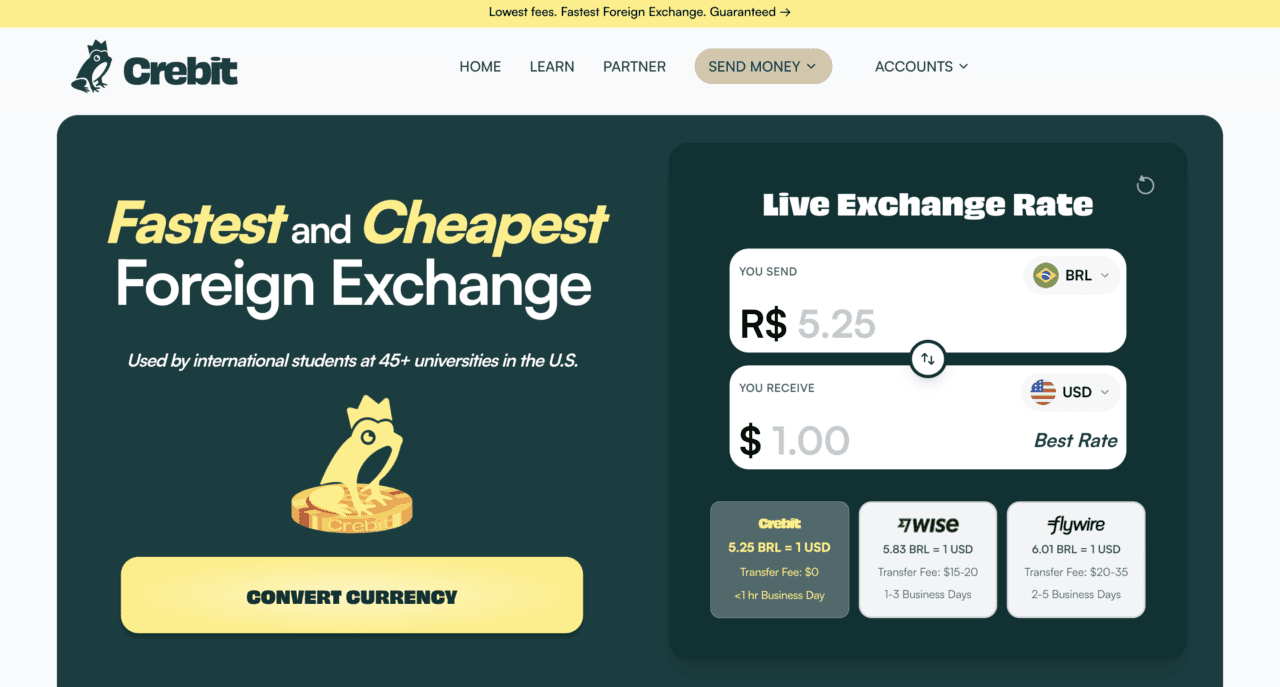

Streamlining Global Payments: The Case of Crebit Pay

One of the most persistent inefficiencies in the global financial system is the cost and speed of international remittances, particularly for the education sector. International students often face exorbitant fees and multi-day delays when transferring tuition or living expenses across borders. Founded in 2025 and headquartered in San Francisco, Crebit Pay is addressing this $500 billion-plus market by utilizing stablecoin infrastructure to facilitate low-cost, near-instant global payments.

Traditional foreign exchange (FX) transactions through the SWIFT network typically involve multiple intermediary banks, each taking a fee and adding to the settlement time. Crebit Pay’s platform offers a settlement process that is 4% to 10% cheaper than traditional FX providers. Crucially, the platform employs a "fiat-in, fiat-out" model, meaning the complexities of the underlying stablecoin technology are entirely invisible to the user. This approach allows credit unions and community banks to offer competitive international services to their members without requiring them to manage digital wallets or understand blockchain mechanics. By focusing on "underserved corridors"—regions often ignored by major payment providers due to lower transaction volumes—Crebit Pay is filling a critical gap in the financial ecosystem.

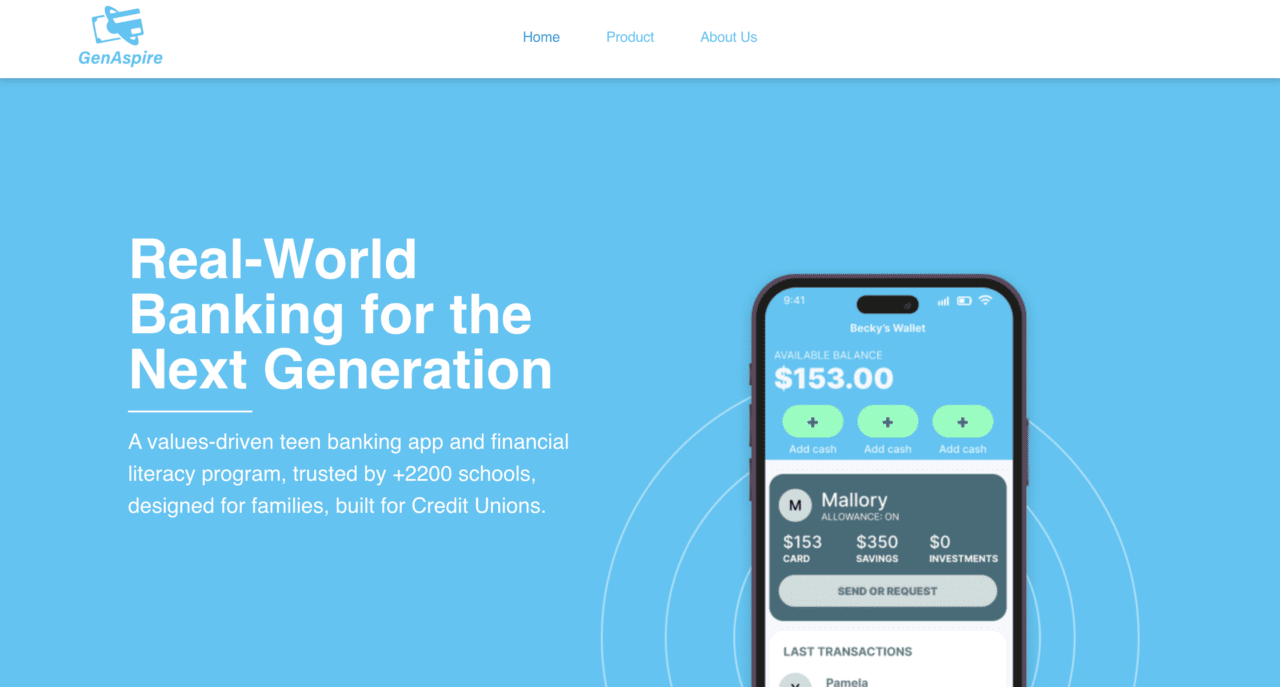

Cultivating the Next Generation: GenAspire and Financial Literacy

While payment infrastructure handles the movement of money, GenAspire is focused on the mindset of the people managing it. Based in Boynton Beach, Florida, and founded in 2025, GenAspire addresses the widening gap in financial literacy among teenagers. According to recent industry data, a significant percentage of Gen Z and Gen Alpha feel unprepared to manage personal finances, despite having unprecedented access to digital payment tools.

GenAspire’s platform is designed specifically for community financial institutions that want to build long-term loyalty with younger demographics. The app gamifies the banking experience, turning tasks like saving and budgeting into interactive challenges. By partnering with over 2,200 schools, GenAspire integrates financial education directly into the academic environment, ensuring that "real-world banking" is accompanied by real-world knowledge. For credit unions, this represents a strategic opportunity to onboard members at an early age, creating a pipeline of financially savvy customers who are more likely to utilize complex products like mortgages and investment accounts in the future.

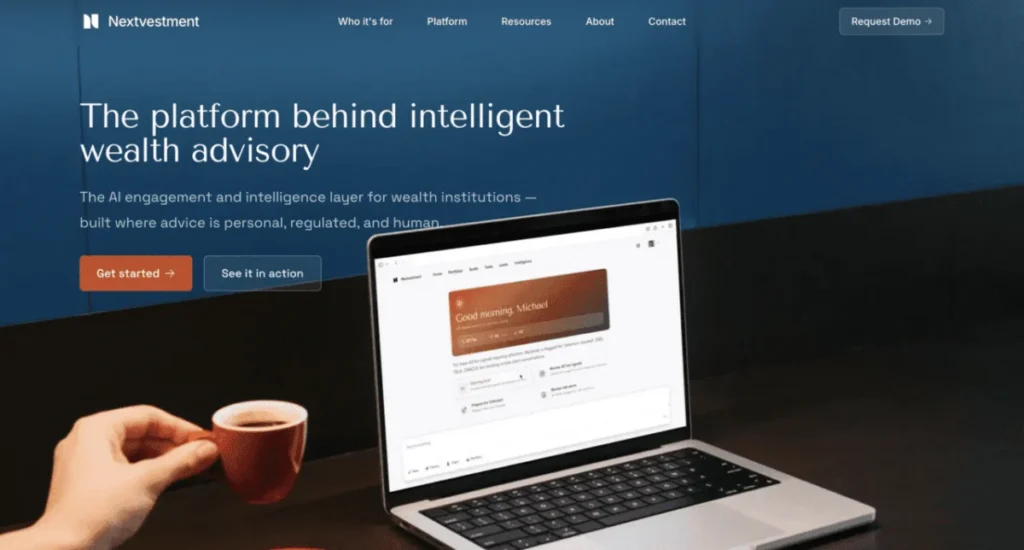

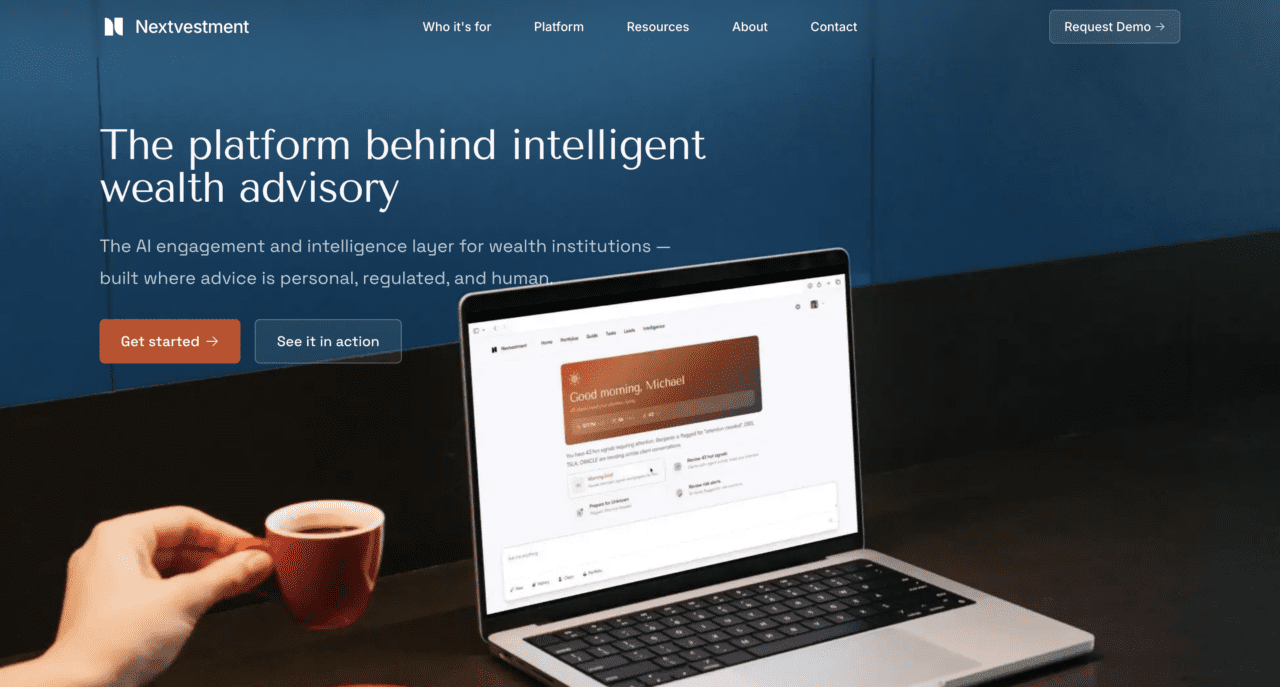

Bridging the Advisory Gap: Nextvestment’s Generative AI Platform

The wealth management sector is currently undergoing a massive demographic shift as trillions of dollars are transferred between generations. This "Great Wealth Transfer" requires a new approach to financial advice—one that combines the efficiency of digital platforms with the nuance of human expertise. Singapore-based Nextvestment, founded in 2024, has developed a generative AI platform that enables this "hybrid" model of service.

Nextvestment allows clients to engage in self-service exploration of investment strategies while using AI to monitor their behavior in real-time. When the system detects a moment where professional intervention is needed—such as a significant change in risk profile or a complex tax implication—it alerts the human advisor to step in. This "proactive compliance" ensures that advisors are spending their time on high-value interactions rather than administrative tasks. For family offices and individual advisors, this technology increases productivity without sacrificing the personalized touch that remains the hallmark of the wealth management industry.

Revolutionizing SME Lending: PROVIDR and Vine Financial

Small and medium-sized enterprises (SMEs) are often described as the backbone of the economy, yet they frequently struggle to secure the capital needed for growth. Traditional underwriting models, which rely heavily on credit scores and historical balance sheets, often fail to capture the true health of a modern small business.

Boston-based PROVIDR, founded in 2025, is tackling this issue through an agentic credit platform. By using AI to analyze alternative data—such as real-time cash flow, social media sentiment, and supply chain reliability—PROVIDR allows lenders to approve more qualified SME loans faster and at a lower cost. The platform does not replace the loan officer; instead, it provides them with a comprehensive "agentic" toolkit that automates the data-gathering and preliminary analysis phases, allowing for more accurate and confident decision-making.

Similarly, Austin-based Vine Financial, founded in 2019, focuses on the scalability of commercial portfolios. As lenders look to grow their commercial books, they often run into a manual bottleneck: the underwriting process. Vine Financial’s platform orchestrates the collaboration between financiers and borrowers, ensuring that deals flow smoothly through the approval pipeline. By turning underwriting into a strategic advantage rather than a logistical hurdle, Vine Financial enables lenders to scale their operations without a corresponding increase in headcount.

Supporting Data: The Economic Imperative for Change

The innovations presented by these five firms are supported by compelling macroeconomic data. According to a 2025 report from McKinsey & Company, the integration of generative AI into the global banking sector could add between $200 billion and $340 billion in value annually through increased productivity and improved risk management. Furthermore, the World Bank has consistently highlighted that reducing the cost of remittances to 3% (down from the current global average of over 6%) could save families in developing nations nearly $20 billion per year.

In the SME sector, the "credit gap"—the difference between the demand for financing and the available supply—is estimated to be over $5 trillion globally. Platforms like PROVIDR and Vine Financial are essential for closing this gap, as they reduce the "cost-to-serve" for banks, making it profitable to lend to smaller businesses that were previously considered too labor-intensive to underwrite.

Strategic Implications for the Banking Sector

For traditional financial institutions, the primary challenge of the current era is differentiation. In a market where basic digital banking features have become commoditized, banks must find new ways to provide value to their customers. The fintechs appearing at FinovateSpring 2026 offer a roadmap for this differentiation.

By adopting tools for financial literacy (GenAspire) and advanced advisory services (Nextvestment), banks can position themselves as partners in their customers’ long-term wellness rather than just utility providers. Simultaneously, by leveraging DeFi and AI for backend operations (Crebit Pay, PROVIDR, Vine Financial), they can achieve the operational margins necessary to survive in a high-interest-rate environment where the cost of capital remains a concern.

Industry analysts suggest that the "fast follower" strategy—where banks wait for technology to be proven before adopting it—is becoming increasingly risky. As these five fintechs demonstrate, the pace of innovation is accelerating, and the firms that integrate these technologies early will have a significant advantage in customer acquisition and retention.

Conclusion: The Path Forward from San Diego

As the fintech community gathers in San Diego this May, the focus will remain on the practical application of advanced technology to solve human problems. The democratization of finance is no longer a distant ideal; it is a tangible goal being realized through smarter underwriting, more efficient payment rails, and a commitment to financial education.

The success of Crebit Pay, GenAspire, Nextvestment, PROVIDR, and Vine Financial will be measured not just by their demo performances, but by their ability to integrate into the existing financial fabric and drive meaningful change for students, families, and businesses worldwide. For banks and financial institutions, the message is clear: the future of finance is inclusive, automated, and deeply integrated into the lives of the next generation. Those who embrace these changes will be the leaders of the 2030 financial landscape.