The Vermont county fair season serves as more than an annual celebration of agricultural heritage; it has become a primary laboratory for early childhood financial education. In an era where digital transactions often obscure the tangible value of currency, educators and parents are increasingly utilizing high-stimulus environments—such as fairs, museums, and school events—to instill foundational economic principles in children as young as five and seven years old. By transitioning from a passive allowance system to an active "labor and discretion" model, families are finding success in demystifying the complexities of consumerism and debt management.

The Theoretical Framework: Needs Versus Discretionary Desires

At the core of this pedagogical approach is a clearly defined family money philosophy. This framework distinguishes between essential parental obligations and discretionary child-led expenditures. Under this model, parents retain responsibility for "needs," which are categorized as housing, healthcare, nutrition, clothing, and educational materials. Furthermore, the parents provide access to cultural and social experiences by covering admission fees to venues such as the Vermont county fairs or local science museums.

The "discretionary" category, however, is shifted entirely to the children. This includes specialized snacks or desserts at restaurants, souvenirs from gift shops, and items from the Scholastic Book Fair. By drawing a hard line between the two, children are forced to evaluate the utility of a purchase. When a child understands that a book is available via the public library or a used book sale at no cost to them, the decision to spend their own capital on a new volume becomes a lesson in opportunity cost.

The Domestic Labor Economy: Establishing Market Value

To facilitate this discretionary spending, a micro-economy is established within the household. Unlike traditional allowance systems that provide a flat weekly rate regardless of effort, this model utilizes a "chores for compensation" system based on fair market value.

The Categorization of Labor

A critical distinction is made between "communal contribution" and "marketable labor." This teaches children the concept of the social contract versus professional employment.

- Unpaid Daily Responsibilities: These tasks are viewed as the "cost of entry" for being part of a functional family unit. They include self-care and maintenance tasks such as making beds, cleaning personal living spaces, putting away personal laundry, and clearing the dining table. On a rural Vermont homestead, this also extends to basic animal husbandry, such as collecting eggs from the chicken coop and managing compost buckets.

- Paid Contractual Chores: These are tasks that provide a service to the parents or the household at large, which the parents would otherwise have to perform or hire out. Examples include organizing kitchen cabinets, processing household trash, or assisting with larger-scale farm maintenance.

Negotiated Compensation

The system allows for negotiation, introducing children to the concept of labor value assessment. In a recent instance, a seven-year-old subject negotiated a $10 lump sum for a comprehensive reorganization of kitchen drawers and cabinets—a task completed in a single day. This introduces the concept of "project-based pay" and rewards efficiency and thoroughness. To maintain quality control, compensation is only dispensed if the task is completed to a professional standard, reinforcing the reality that sub-par labor in the adult world often results in financial penalties or the requirement to redo work without additional pay.

Case Study in Debt Management: The Inflatable Unicorn Incident

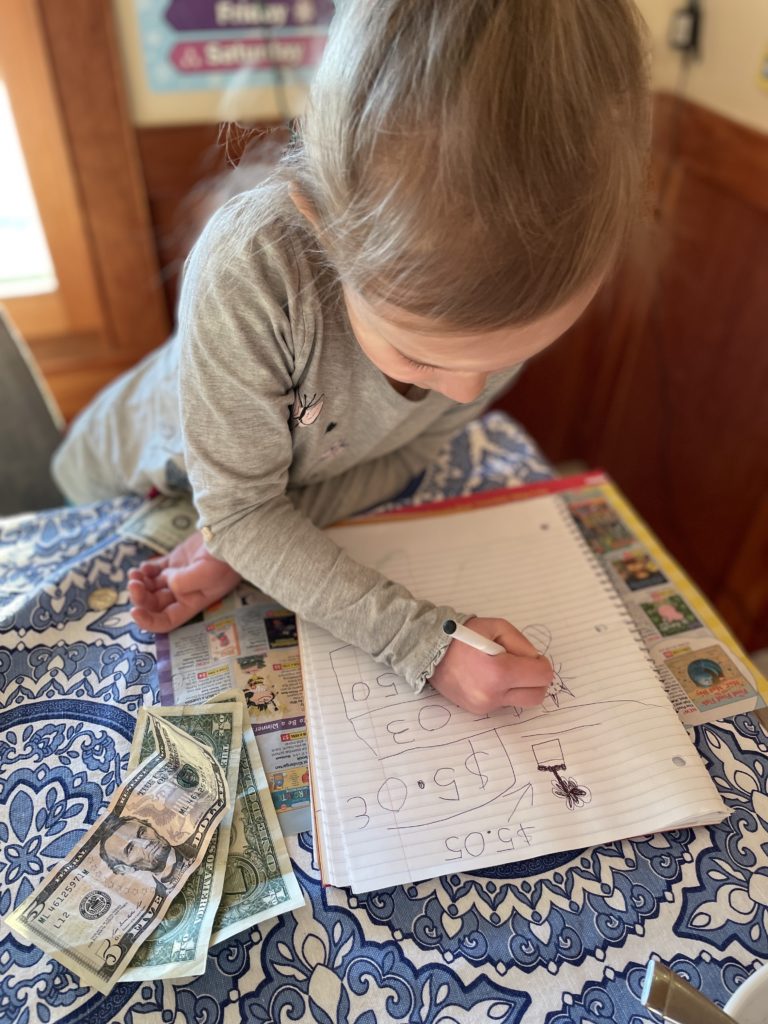

One of the most profound lessons in this financial curriculum occurred during a previous year’s county fair. A child expressed a desire to purchase an inflatable turquoise unicorn priced at $13. At the time of the request, the child possessed only $9 in personal capital.

The parents opted to act as a lending institution, providing a $4 bridge loan to facilitate the purchase. However, this came with strict "debt service" requirements. Upon returning home, the child was informed that all future paid chores were no longer optional until the $4 debt was settled. The child spent a significant period performing labor for which they received no "new" cash, as the earnings were immediately garnished to repay the loan.

The child’s subsequent realization—that working for an item already in one’s possession is significantly less rewarding than working for future capital—served as a visceral introduction to the psychological burden of debt. Data suggests that such early experiences with "negative reinforcement" in debt can lead to more cautious credit use in adulthood. In the year following this incident, neither child in the study has opted to enter into a debt agreement again.

Sibling Economics and Collaborative Purchasing

The financial education also encompasses collaborative spending and the division of costs. During a series of "pizza nights" at a local farm, the children identified a desire for desserts that were not covered under the parents’ "needs" budget.

Initially, the elder child (age seven) funded the $7 dessert independently but allowed the younger child (age five) to consume half. The elder child eventually identified the inequity in this arrangement and initiated a negotiation. This resulted in a cost-sharing agreement where both children contributed to the purchase.

This scenario introduced two secondary educational opportunities:

- Currency Denominations: Because $7 cannot be divided equally using single-dollar bills, the children were required to use coins (quarters, dimes, and nickels) to reach a $3.50 split, reinforcing mathematical literacy.

- Transaction Independence: The children were tasked with approaching the vendor, placing the order, and managing the physical exchange of currency and change without parental mediation. This builds "consumer confidence" and reduces the anxiety often associated with financial transactions.

National Context: The State of Youth Financial Literacy

The implementation of these "home-grown" economic systems comes at a time when national financial literacy is under scrutiny. According to the 2023 Survey of the States by the Council for Economic Education, only 25 states currently require high school students to take a course in personal finance.

Experts in childhood development argue that waiting until high school to introduce these concepts may be too late. The "scaffolding" method used in the Vermont case study—starting with counting and price reading before moving to debt and interest—aligns with recommendations from the Consumer Financial Protection Bureau (CFPB), which emphasizes that the building blocks of financial capability are laid in early childhood through the development of executive function and self-regulation.

Implications and Future Projections: The Parental Bank

As the children master the basics of earning and spending, the next phase of the curriculum involves the introduction of long-term savings and compound interest. The parents have proposed the creation of the "Bank of Parental Units," a domestic savings program that will pay a high internal rate of interest on any capital the children choose to save rather than spend.

This phase aims to shift the children’s focus from immediate gratification to capital growth. By providing a visible and high-yield interest rate (often much higher than market rates to ensure the lesson is impactful), parents can demonstrate how "money makes money."

Conclusion: Money as a Tool, Not a Status

The ultimate objective of this intensive financial upbringing is to demystify money and reframe it as a neutral tool for living. By stripping away the emotional weight and social status often attached to wealth, the parents aim to foster a generation of consumers who view financial management as a logistical skill rather than a source of anxiety.

Through the combination of real-world experience at the county fair, the disciplined environment of the chore economy, and the harsh reality of debt repayment, these children are gaining a level of economic agency that is rarely found in the traditional "allowance" model. As they move toward opening their first "bank accounts," the foundation of labor, math, and discipline appears firmly set, providing a blueprint for other families seeking to navigate the pressures of modern consumerism.