Brian and Michael, a couple based in central Connecticut, are currently navigating a complex financial transition as they approach their tenth anniversary. Both aged 34, the couple represents a significant demographic of millennials who, despite maintaining stable professional careers in the public and non-profit sectors, find themselves constrained by consumer debt and the rising barriers to entry in the residential real estate market. Brian serves as a quality assurance manager for a state-run hospital, while Michael operates as a project coordinator for a state behavioral health agency, supplemented by a secondary role as a disability leadership coordinator. Despite a combined gross household income of approximately $167,544, the couple reports feeling hindered by $28,259 in high-interest consumer debt and a lack of liquid savings, which has effectively deferred their goals of home ownership and marriage.

Professional Background and Economic Context

The couple’s financial trajectory is characterized by a shift from the private and non-profit sectors into public service. Brian, who previously managed $58,000 in student loan debt, successfully eliminated those obligations several years ago. His transition to a state-level role has provided significant long-term security, including a projected pension and lifetime healthcare benefits. Michael’s career is deeply rooted in advocacy, informed by his personal experience as a brain injury survivor.

Their current residence is a two-bedroom, two-bathroom apartment located in a refurbished industrial mill. While the unit offers modern amenities and architectural significance, the move to this location in late 2022 was prompted by an unplanned displacement from a long-term studio apartment. This transition coincided with high inflationary pressures in the Connecticut rental market and unexpected veterinary expenses, which served as the primary catalysts for their current debt accumulation.

Chronology of Recent Financial Stressors

The period between August 2022 and late 2023 serves as the critical timeline for the couple’s current financial standing.

- August 2022: The couple maintained a stable residency in a 600-square-foot studio apartment with a monthly rent of $945. At this time, they forecasted a transition to home ownership by late 2023.

- Late 2022 – Early 2023: An unplanned notice to vacate their long-term residence forced a 3.5-month search in a volatile rental market. Simultaneously, the couple adopted two kittens that required significant medical intervention, leading to high out-of-pocket veterinary costs.

- Mid-2023: The couple relocated to their current mill apartment, where rent increased to $2,000 per month—more than double their previous housing expenditure. To manage the costs of moving, furniture, and medical bills, the couple utilized credit cards, leading to the current debt load.

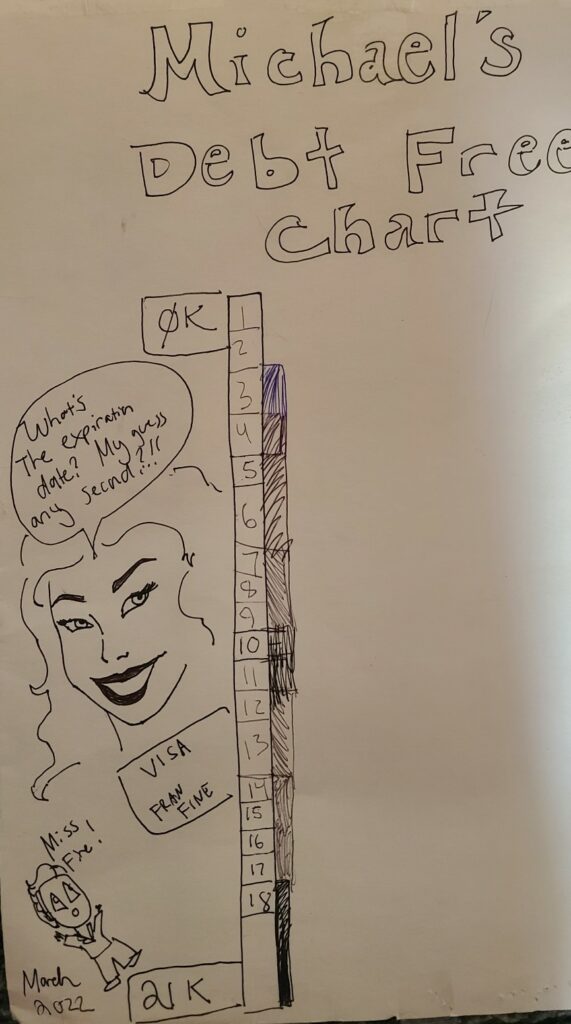

- November 2023: This date represents a critical "cliff" in their financial planning, as promotional 0% interest rates on their largest credit card balances are set to expire, potentially exposing them to interest rates exceeding 17%.

Comprehensive Financial Data Analysis

An objective analysis of the household’s balance sheet reveals a discrepancy between their earning potential and their current liquidity.

Income and Cash Flow

The household generates a net annual income of $109,455.42 after taxes and pre-tax retirement contributions. Their current reported annual spending is approximately $96,414.36, which includes $2,000 in monthly debt service. Under current conditions, the couple should theoretically possess a surplus of $13,041 annually. However, the lack of a formal tracking system has led to "leakage," where discretionary spending on home goods, dining, and personal care has absorbed potential savings.

Debt Obligations

The total consumer debt of $28,259 is distributed across three primary accounts:

- Visa (SCU): $16,057 at 0% interest (expiring November 2023, then 17.99%).

- Visa Platinum (NFCU): $9,700 at 10.99% interest.

- Visa Platinum (Navy Federal): $2,503 at 0.99% (expiring November 2023, then 17.74%).

Asset Allocation

The couple’s total assets are valued at $91,250, but these are largely illiquid or designated for retirement:

- Retirement Accounts: Michael’s 401k ($36,992) and Brian’s various state-sponsored accounts (403b, 457, and pension fund) comprise the bulk of their net worth.

- Liquid Cash: The couple holds approximately $9,000 in combined savings, which represents roughly 1.1 months of expenses—well below the recommended 3-to-6-month emergency fund threshold.

- Vehicles: Two 2007 model-year vehicles (Mercedes and Subaru) with high mileage (175,000+), posing a risk for future capital expenditures.

Market Analysis and Connecticut Housing Trends

The couple’s desire to "buy low" in the housing market faces significant headwinds. According to data from the Connecticut Association of Realtors, the median sales price for single-family homes in Connecticut has seen a steady increase, rising approximately 5-8% year-over-year in many central corridors. Furthermore, inventory levels remain at historic lows, creating a "seller’s market" despite rising mortgage interest rates.

For Brian and Michael, the transition from a $2,000 rental to a mortgage involves not just the down payment, but also the "hidden costs" of home ownership, such as property taxes (which are notably high in Connecticut), maintenance, and insurance. Financial experts suggest that a transition to home ownership for this couple is currently premature given their debt-to-income ratio and the lack of a robust down payment fund.

Strategic Recommendations for Debt Elimination

Financial consultants specializing in millennial wealth building suggest a multi-phased approach to stabilize the couple’s finances.

Phase 1: The "Spending Detox"

To address the $28,259 debt before the November interest rate hikes, a rigorous reduction in discretionary spending is required. By categorizing expenses into "Fixed," "Reduceable," and "Discretionary," the couple can identify approximately $1,370 in monthly savings.

- Elimination of Discretionary Items: Dining out ($200), gifts ($260), home goods ($200), and various subscriptions could be suspended temporarily.

- Aggressive Repayment: By redirecting these funds, the couple could increase their monthly debt payments to over $4,400, effectively clearing their entire debt load in less than seven months.

Phase 2: Emergency Fund Fortification

Once the consumer debt is eliminated, the priority must shift to cash liquidity. An emergency fund serves as the primary defense against future debt cycles. For this household, a target of $25,000 to $30,000 is recommended to cover six months of essential expenses. This fund would mitigate the impact of the "predictable emergencies" they previously faced, such as veterinary bills and car repairs.

Phase 3: Retirement Optimization

Brian’s access to both a 403(b) and a 457(b) plan provides a unique "double contribution" opportunity. In 2023, the IRS allows individuals to contribute up to $22,500 to each plan if they are offered by the same employer, effectively doubling their tax-advantaged savings potential. However, this should only be pursued once debt is cleared and the emergency fund is established.

Educational and Career Implications

A significant point of internal debate for the couple is Brian’s pursuit of a Master’s degree. From a purely financial standpoint, the Return on Investment (ROI) for advanced education must be scrutinized. If the degree does not correlate with a guaranteed and significant salary increase within the state hospital system, the expenditure of time and capital may actually delay their goal of home ownership. In the current economic climate, "credential inflation" often leads professionals to acquire debt for degrees that offer marginal utility in the labor market.

Broader Impact and Conclusion

The situation faced by Brian and Michael is emblematic of a broader "lifestyle creep" that affects high-earning millennial households. The psychological burden of "financial shame" mentioned by both subjects is a common byproduct of the gap between societal expectations of adulthood—such as home ownership—and the reality of modern economic volatility.

The implications of this case study suggest that for households with high gross incomes, the primary obstacle to wealth accumulation is often not the income level itself, but the lack of structural oversight regarding cash flow. By transitioning from a reactive financial posture (using credit cards for emergencies) to a proactive one (building cash reserves and tracking expenses), Brian and Michael can leverage their public sector stability to achieve long-term solvency.

The broader takeaway for similar households is that "spreadsheet problems"—debts and savings targets—are solvable through behavioral modification and disciplined allocation. As the couple approaches their 10-year anniversary, their focus shifts from the shame of past expenditures to the strategic utility of their future earnings, providing a blueprint for middle-class financial recovery in a post-inflationary economy.