The global financial landscape has undergone a dramatic transformation, with interest rates recently surging to their highest levels in two decades. This abrupt shift follows a prolonged period of near-zero rates that characterized the post-2008 financial crisis era, fundamentally altering economic calculations for consumers, businesses, and governments worldwide. The sudden recalibration by central banks, most notably the U.S. Federal Reserve, marks a decisive departure from the accommodative monetary policies that underpinned economic activity for over fourteen years.

The End of an Era: A Look Back at Near-Zero Rates

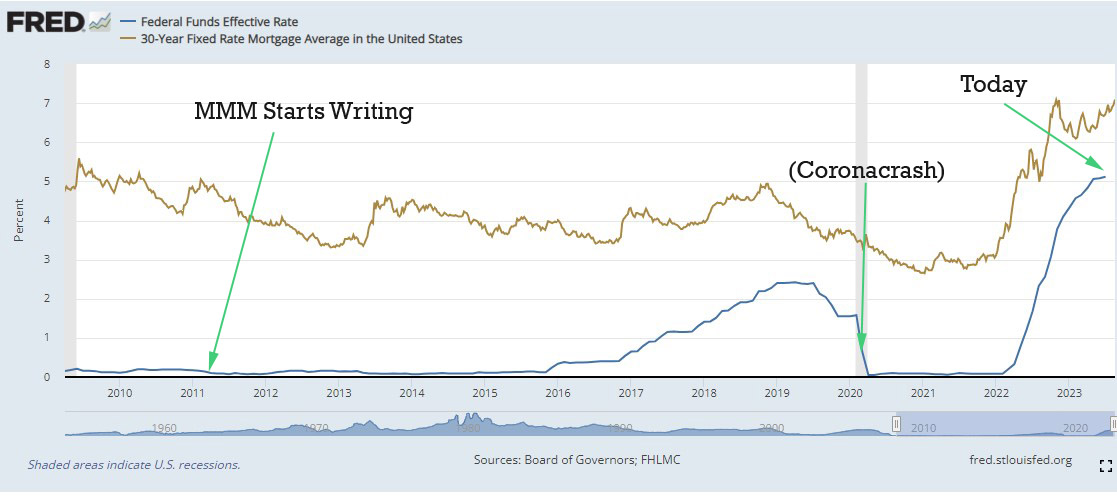

For more than a decade, stretching from the aftermath of the 2008 global financial crisis until late 2021, central banks across advanced economies maintained exceptionally low interest rates. This period of unprecedented monetary easing was primarily designed to stimulate economic growth, encourage borrowing and investment, and ward off deflationary pressures following a severe recession. With benchmark rates often hovering close to zero, the cost of capital was remarkably cheap.

This environment fueled significant expansion across various sectors. Mortgages became more affordable, leading to increased demand for both new and existing homes. Low borrowing costs also spurred corporate investment, with businesses finding it inexpensive to finance expansion, launch new ventures, and hire additional employees. This era witnessed a robust cycle of prosperity, innovation, and job creation, with readily available credit acting as a powerful stimulant for consumption and asset appreciation. The digital age, in particular, flourished under these conditions, with venture capital flowing freely into nascent technologies and startups.

The Rise of Inflation and the Policy Pivot

However, the prolonged period of easy money, coupled with a series of external shocks, eventually led to the resurgence of inflation. Beginning in late 2021 and accelerating into 2022, a confluence of factors ignited price increases not seen in decades. Supply chain disruptions, exacerbated by the COVID-19 pandemic and geopolitical tensions, constrained the availability of goods. Simultaneously, unprecedented fiscal stimulus packages injected significant purchasing power into the economy, leading to a situation where "too much money was chasing too few goods." This imbalance was particularly acute in sectors like housing, where demand far outstripped supply.

The U.S. Consumer Price Index (CPI) climbed steadily, eventually reaching over 9% year-over-year in mid-2022, significantly exceeding the Federal Reserve’s long-term target of 2%. Faced with the mandate to maintain price stability, Federal Reserve Chairman Jerome Powell and the Federal Open Market Committee (FOMC) initiated a series of aggressive interest rate hikes. This marked a sharp pivot from monetary accommodation to tightening, aimed at cooling down an overheated economy and bringing inflation back under control. The metaphor of the "gas pedal" illustrates this shift: after years of pressing down to accelerate growth, the central bank began to ease its foot, applying the brakes to curb inflationary pressures.

Economic Ramifications: A Broad Impact

The rapid increase in interest rates has sent ripples throughout the economy, impacting various sectors in profound ways.

Housing Market Contraction: Perhaps the most immediate and visible impact has been on the housing market. Mortgage rates, which were historically low at around 3% just two years ago, have soared to over 7.5% in many regions. This drastic increase has significantly diminished housing affordability. For an average-priced home requiring a typical 10% down payment, the monthly mortgage payment has increased substantially, effectively pricing out a considerable segment of potential buyers. This has led to a noticeable slowdown in sales, a decline in new construction starts, and a stabilization, and in some areas, a softening of home prices. Existing homeowners with locked-in low-interest mortgages are also less inclined to sell, contributing to lower inventory and further complicating market dynamics for buyers. The intended effect of this "tough medicine" is to reduce speculative demand, bring prices back in line with fundamentals, and increase housing supply over time as construction costs potentially moderate.

Business Investment and Employment Adjustments: Companies are also feeling the pinch of higher borrowing costs. Financing for expansion, capital expenditures, and even day-to-day operations has become more expensive. This has led many businesses to scale back growth plans, postpone new factory constructions, and implement hiring freezes or even layoffs. High-profile examples include major technology firms like Meta (Facebook) and Amazon, which collectively shed tens of thousands of employees in 2022 and 2023, reflecting a broader trend of corporate belt-tightening in response to a less favorable economic climate. Venture capital funding has also tightened, impacting the startup ecosystem.

Financial Sector Volatility: The rapid rate hikes also exposed vulnerabilities within the financial system, culminating in a "miniature banking crisis" in early 2023. Several mid-sized banks, including Silicon Valley Bank, Signature Bank, and First Republic Bank, failed or required emergency intervention. These failures were largely attributed to their exposure to long-dated, low-yielding bonds that depreciated significantly as interest rates rose, coupled with concentrated deposit bases and rapid withdrawals. The crisis prompted swift action from regulators to stabilize the banking system and mitigate broader systemic risks.

The Broader Economic Picture: Conflicting Signals:

Despite these challenging developments, the overall economic picture remains complex and subject to differing interpretations. While some analysts and media outlets portray the current period as "hard economic times," official data often presents a more resilient outlook. For instance, the U.S. unemployment rate has remained remarkably low, hovering around 50-year lows, indicating a strong labor market. This resilience has surprised many economists, suggesting that the economy is still digesting the previous period of robust growth rather than spiraling into a severe downturn. Central banks are striving for a "soft landing"—a scenario where inflation is brought under control without triggering a significant recession—though the path remains precarious.

Navigating the New Investment Landscape

The shift in interest rates necessitates a re-evaluation of investment strategies for individuals and institutions alike.

Equities: The Long-Term View: For stock market investors, the fundamental advice remains consistent: avoid attempting to time the market. While the overall U.S. market saw a decline of approximately 10% from its early 2022 peak to mid-2023, and remained relatively flat for two years excluding dividends, this represents a "sale" opportunity for long-term investors. Historical data consistently demonstrates that equity markets tend to recover and generate significant returns over extended periods, despite intermittent downturns. Selling during a dip often locks in losses and misses subsequent rebounds. Therefore, a consistent, disciplined approach to investing in broad-market index funds is generally recommended.

Fixed Income and Savings Accounts: Renewed Attractiveness: The rise in interest rates has significantly enhanced the appeal of cash and fixed-income investments. High-yield savings accounts and money market funds now offer rates of 4.5% or more, providing a relatively stable and rewarding environment for short-term savings. Longer-term bonds also offer more attractive yields. This presents a nuanced decision for investors: while stocks offer higher potential long-term growth, especially when "on sale," the guaranteed, albeit lower, returns from fixed-income instruments provide a compelling alternative, particularly for those seeking capital preservation or liquidity. The optimal strategy often involves a balanced approach, considering individual risk tolerance and financial goals.

Future Outlook: Interest Rates and Housing Prices

Predicting the future trajectory of interest rates and housing prices is inherently challenging, yet informed analysis offers some insights.

Interest Rate Projections: A Return to Normalcy?

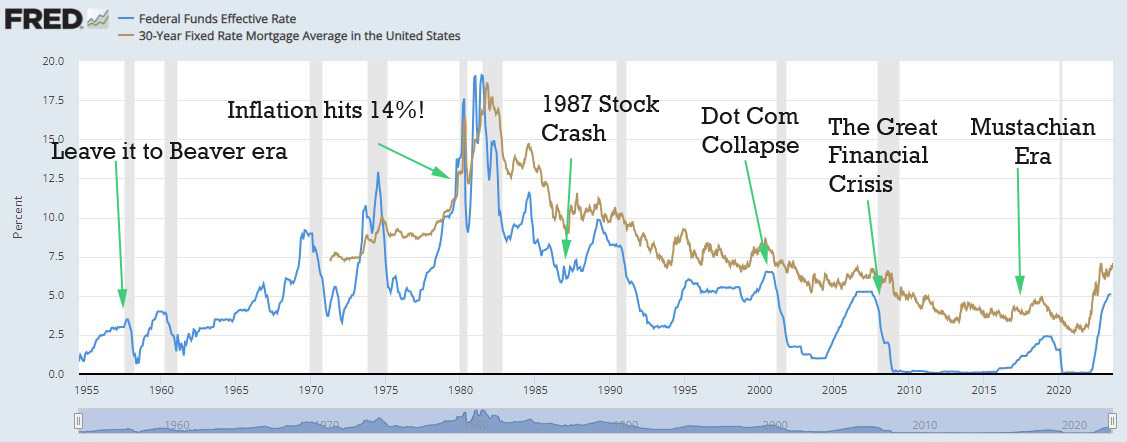

It is crucial to contextualize current interest rates within a broader historical perspective. While the recent surge feels dramatic after a decade of near-zero rates, zooming out over the last seventy years reveals that current rates are, in fact, closer to the historical average rather than being exceptionally high.

The future direction of interest rates will largely depend on key economic indicators, particularly inflation and unemployment. Central banks will continue to monitor these closely, adjusting their policy stance as necessary. Rates are likely to decrease when the Federal Reserve determines that the economy is slowing excessively, potentially signaling the onset of a genuine recession. Such a scenario would typically be characterized by sustained low inflation and rising unemployment.

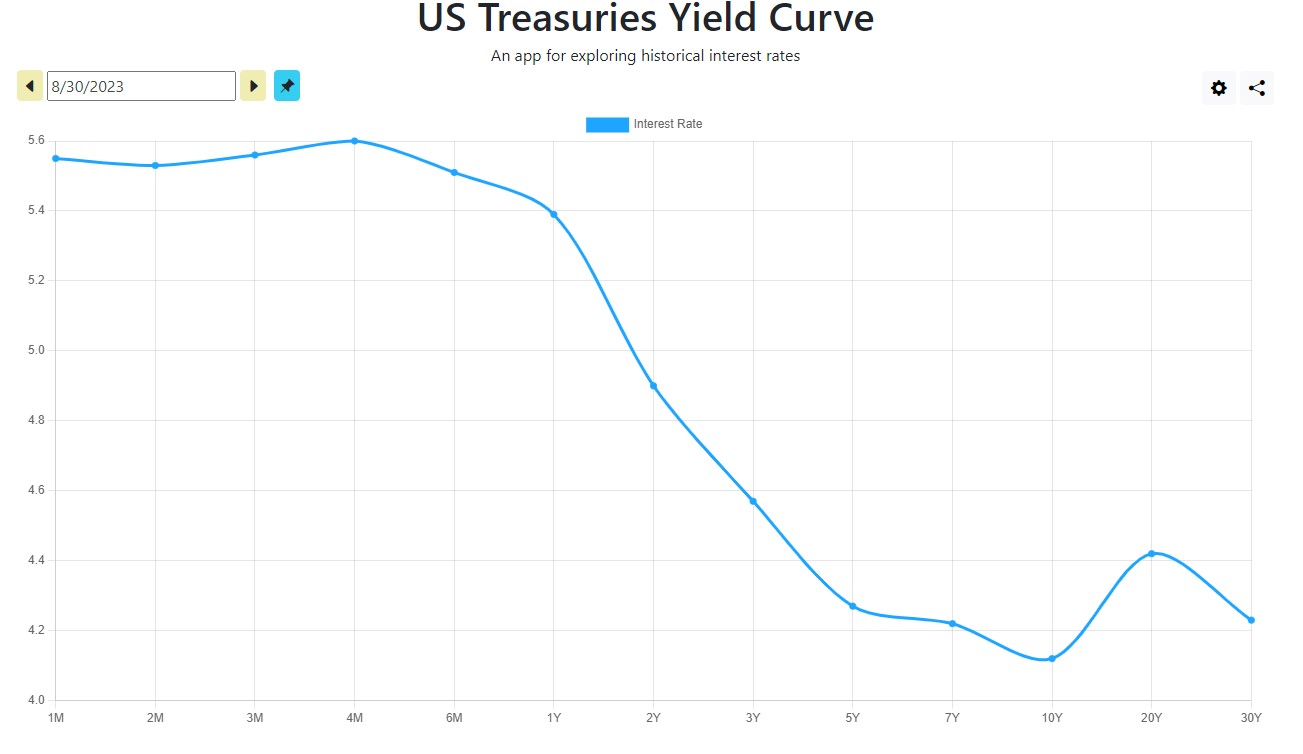

The Inverted Yield Curve: A Recessionary Signal?

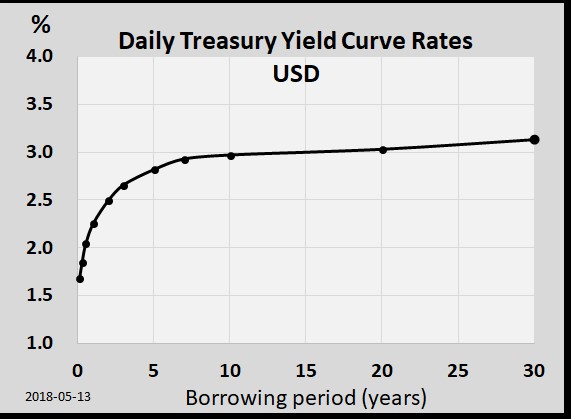

A significant indicator currently drawing attention is the inverted U.S. Treasury yield curve. Typically, long-term bonds offer higher yields than short-term ones, rewarding lenders for locking up their money for longer periods. However, the current environment shows short-term yields (e.g., 1-year Treasury bills at 5.4%) exceeding long-term yields (e.g., 10-year Treasury bonds at 4.05%). This "inverted yield curve" is a historically reliable predictor of future economic slowdowns or recessions. It implies that bond market participants anticipate interest rates will fall in the future, often due to an expected economic contraction and subsequent central bank easing. Historically, an inverted yield curve has preceded ten out of the last eleven U.S. recessions over the past 75 years, suggesting a high probability of an economic downturn and subsequent rate cuts within the next 18-24 months.

Housing Price Forecasts: Supply, Demand, and Regulation:

The future of housing prices is a complex interplay of supply, demand, and regulatory factors. Key determinants include:

- Construction Costs: While technological advancements and global trade can make building materials and processes more efficient over time, local labor costs and regulatory compliance can offset these gains.

- Population Growth and Migration: Continued population growth in desirable areas drives demand for housing.

- Local Zoning and Regulatory Restrictions: Restrictive zoning laws, complicated building codes, and lengthy approval processes (often termed "NIMBYism" – Not In My Backyard) significantly constrain housing supply. These bureaucratic hurdles increase the cost and time involved in construction, ultimately contributing to higher prices by limiting new housing options.

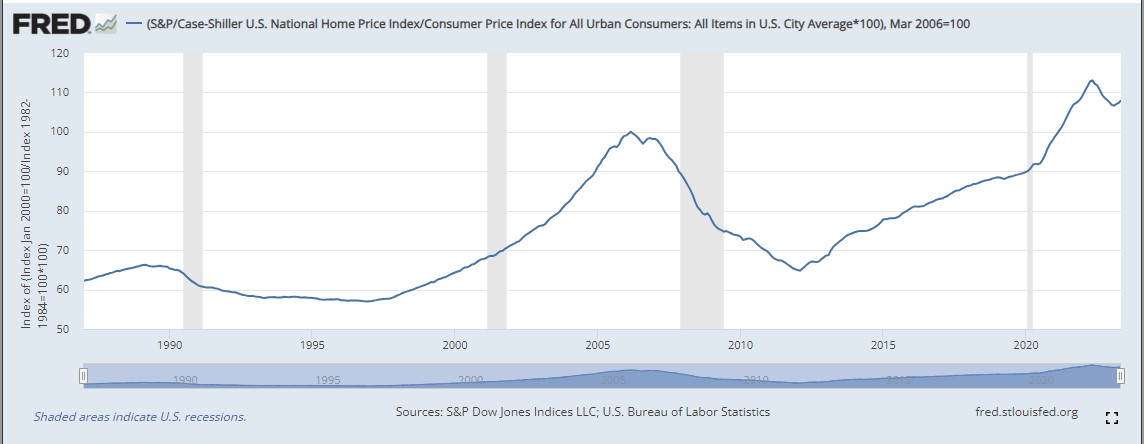

Given that inflation-adjusted U.S. house prices are near an all-time high, a potential correction or period of stagnation is plausible. Analysts suggest a possible easing of prices, perhaps a 25% decline to 2020 levels in some markets, or a prolonged period where prices remain flat, effectively becoming cheaper relative to inflation and rising incomes. The actual outcome will vary significantly by region, depending on local economic conditions and regulatory environments. Some cities, for example, are proactively addressing housing shortages by streamlining approval processes and promoting denser, car-independent developments, which tend to be more affordable to construct.

The Ultimate Strategy: Financial Independence and Adaptability

In an environment of fluctuating interest rates and economic uncertainty, the most robust financial strategy remains consistent: cultivate financial independence. For individuals nearing or in retirement, the impact of interest rate changes on borrowing is often minimal, as they typically have less debt. The simplicity of owning a primary residence and vehicles outright, free of mortgage burdens, offers significant insulation from interest rate volatility.

Furthermore, possessing substantial savings provides a critical advantage. Rather than relying on credit, having readily available cash enables individuals to seize opportune investments, whether it’s a dip in the stock market or a desirable real estate deal. This position of strength reduces financial stress and allows for strategic decision-making, rather than being dictated by prevailing interest rates. Even with ample cash, the option to secure a mortgage remains if rates become favorable for specific financial goals.

Ultimately, maintaining a disciplined and adaptable financial approach is paramount. Prioritizing a lean and sustainable lifestyle, consistent saving, and prudent investment decisions allows individuals to navigate economic shifts with greater resilience. While external factors like interest rates and housing prices are largely beyond individual control, the power of personal financial choices in earning, saving, and healthy living ensures that these broader economic ripples remain secondary to one’s overall financial well-being.