The United States finds itself once again immersed in an election year, a period traditionally marked by heightened political discourse and intense scrutiny of national affairs. While the contest between leading candidates like Kamala Harris and Donald Trump captures significant public attention, a more critical examination reveals that many of the economic arguments presented to voters are often disconnected from fundamental economic realities. For informed citizens, particularly those well-versed in personal finance principles, the emphasis remains on discerning factual economic data from politically motivated rhetoric, ultimately focusing on individual financial prudence within one’s "circle of control" after casting a vote.

This election cycle has seen a particularly pronounced divergence between expert economic assessments and the narratives propagated by political campaigns. While politicians are not typically lauded for their deep understanding of complex technical fields such as science, technology, or economics, the current discourse surrounding the nation’s financial health has reached a concerning level of simplification and emotional manipulation. Candidates frequently appeal to the sentiments of undecided voters in swing states, often employing arguments that prioritize immediate emotional resonance over sound economic principles.

Current Economic Landscape vs. Public Perception

A striking example of this disconnect is the persistent claim by the challenging party, currently led by Donald Trump, that the incumbent administration (Biden/Harris) presides over a "bad economy." This assertion stands in stark contrast to numerous key economic indicators. The U.S. economy, by many measures, is experiencing a period of robust health. Gross Domestic Product (GDP) growth has remained resilient, and perhaps most notably, unemployment rates have reached historic lows, hovering near 3.9% as of recent reports from the Bureau of Labor Statistics (BLS). Such figures historically signal a strong labor market and a thriving economy, challenging the notion of widespread economic distress.

The recent bout of elevated inflation, which peaked in mid-2022, is often cited by critics as evidence of a struggling economy. However, economic analysts frequently interpret this inflation, in part, as a consequence of an economy running "too hot," spurred by factors such as significant government stimulus during the COVID-19 pandemic and robust consumer demand. The Federal Reserve’s subsequent implementation of higher interest rates was a deliberate measure to cool demand and bring inflation back toward its target of 2%. As of late 2024, inflation has significantly moderated, with the Consumer Price Index (CPI) showing a year-over-year increase of approximately 2.4%, a level much closer to the Fed’s target.

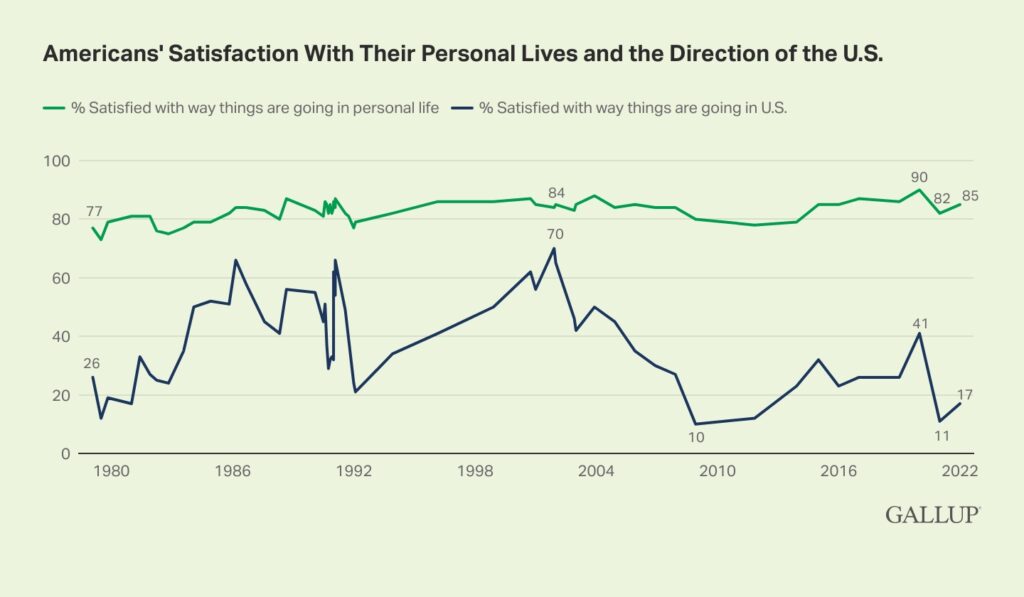

Despite these objective economic indicators, public sentiment often lags or diverges significantly. A Gallup poll highlighted this paradox, revealing that while a substantial majority of Americans (approximately 85%) reported being personally satisfied with their current financial situation, a mere 17% believed the national economy was performing well. This mathematical inconsistency – where individual prosperity does not translate into a positive perception of the broader economy – is a symptom of several factors. Economists and social scientists point to a negativity bias in news consumption, the amplification of selective narratives by social media algorithms, and the pervasive spread of misinformation that can shape public opinion irrespective of verifiable facts.

Debunking Common Economic Myths in Political Discourse

In an environment where accurate information empowers individuals both financially and civically, it becomes imperative to challenge and clarify the pervasive economic fallacies promoted during election campaigns.

1. The President’s Limited Control Over the National Economy

A common political tactic involves presidents claiming credit for economic booms and opposition parties assigning blame for downturns. However, the reality of the U.S. economy is far more nuanced. As the world’s largest economy, accounting for approximately 26% of global economic activity, its immense scale and inherent dynamism make it largely impervious to unilateral presidential control. The U.S. economy operates as a complex, largely free-market system driven by billions of individual decisions regarding production, consumption, and investment.

While presidential administrations and Congress can influence the economy through fiscal policies—such as tax rates, government spending, and regulatory frameworks—the effects of these policies are often delayed, indirect, and subject to numerous other variables. Economic cycles, characterized by periods of "irrational exuberance" (like the 2007 housing boom) followed by fear and pessimism (such as the 2008-2012 financial crisis), are largely driven by market psychology, technological advancements, and global events. These forces exert a far greater short-term influence than any single presidential directive. Furthermore, the U.S. economy is intrinsically linked to the global economic landscape, meaning international trade, geopolitical stability, and the performance of other major economies significantly impact domestic conditions, often beyond the direct influence of Washington.

2. The Federal Reserve’s Independent Role in Setting Interest Rates

Another prevalent misconception is the idea that the President can directly manipulate interest rates to alleviate financial burdens on the middle class. Candidates frequently express sympathy for high borrowing costs on credit cards, auto loans, and mortgages, promising to "fight" to lower them. Such rhetoric fundamentally misunderstands the structure and function of U.S. monetary policy.

Interest rates, particularly the benchmark federal funds rate, are primarily determined by the Federal Reserve, an independent central bank. The Fed’s primary mandate is to achieve maximum employment and stable prices (low and stable inflation). To achieve this, its Federal Open Market Committee (FOMC) adjusts interest rates using sophisticated economic models and data analysis. Raising rates slows economic activity and curbs inflation, while lowering rates stimulates growth. Presidential interference in this process, as suggested by some candidates, would undermine the Fed’s crucial independence and could lead to politically motivated monetary policy, historically a recipe for economic instability and even hyperinflation in other nations. The Fed’s autonomy is a cornerstone of economic stability, shielding monetary policy from the short-term political cycles and ensuring decisions are based on long-term economic health.

3. The Nuance of Inflation and Real Wage Growth

The narrative that inflation has unequivocally made life harder for Americans, and that a president can magically reverse price increases, is often simplistic and misleading. Following the extraordinary circumstances of the COVID-19 pandemic, a confluence of factors—including supply chain disruptions, increased consumer demand fueled by government stimulus, and historically low interest rates—led to a period of elevated inflation. While this initially eroded purchasing power, the situation has evolved.

Critically, recent data from sources like the BLS demonstrate that aggregate wages have largely kept pace with, and in many instances, outstripped inflation. For example, since 2019, overall prices have risen by approximately 19%, while average wages have increased by around 21%. This indicates that, on average, American workers are actually better off in real terms than before the inflationary spike. The political promise to "bring prices back down" is not only economically unrealistic (as deflation can be highly damaging) but also ignores the underlying wage growth that has occurred. The more accurate economic goal is price stability, not a reversal of prices.

Furthermore, the blame often placed on "greedy corporations" for increasing prices to hoard profits, a concept sometimes dubbed "greedflation," also warrants careful scrutiny. While businesses do aim for profit maximization, competitive markets typically limit the extent to which companies can arbitrarily raise prices without losing market share. In-depth analyses, such as a recent report from NPR, have shown that sectors like grocery retail did not experience windfall profits directly attributable to recent inflation, suggesting that price increases were largely driven by rising input costs (labor, raw materials, transportation) rather than opportunistic price gouging.

4. Addressing the Complexities of Housing Affordability

Housing prices and rents have indeed risen significantly faster than general inflation and wages over the past decade, creating a genuine affordability crisis in many regions. The concurrent rise in interest rates, while intended to cool the housing market by dampening demand, has instead created a "double whammy" for prospective homebuyers: higher prices compounded by higher borrowing costs.

Political solutions often propose demand-side interventions, such as subsidies for first-time homebuyers or government-mandated reductions in interest rates. However, many economists argue that such measures, while seemingly beneficial, can exacerbate the problem by further inflating demand without addressing the fundamental issue: insufficient housing supply. The real solution, widely supported by urban planners and economists, lies in increasing the availability of housing. This requires policy changes at local and state levels to streamline and accelerate permitting processes, reduce onerous and expensive building codes, reform or eliminate restrictive suburban-style zoning (e.g., single-family zoning, minimum lot sizes, excessive setback requirements), and limit the power of NIMBY (Not In My Backyard) groups to obstruct new development. Such reforms could significantly reduce construction costs and increase housing availability, making homes more affordable in the long run.

5. The Diminishing Relevance of Gasoline Prices

Gasoline prices, a perennial point of contention in political campaigns, are frequently discussed with an emphasis that disproportionately outweighs their actual economic impact and evolving relevance. On an inflation-adjusted basis, gasoline prices, typically ranging from $3-4 per gallon, are comparable to what they were in the 1950s. Moreover, despite the size of American vehicles, the average household dedicates a relatively small portion of its disposable income—approximately 2.5%—to gasoline. This figure is often overshadowed by the far greater costs associated with vehicle ownership, such as depreciation, insurance, and maintenance.

Perhaps more critically, the very premise of focusing intensely on gasoline prices is becoming increasingly anachronistic. The rapid advancement and adoption of electric vehicles (EVs) have made gasoline an increasingly obsolete fuel for many consumers. Used EVs are now often available at prices competitive with or even below comparable used gasoline cars, and new EV models are increasingly achieving price parity. EVs offer numerous advantages, including superior performance, significantly lower maintenance requirements, and the elimination of gasoline expenses. In this context, political debates over gasoline prices often appear to be relics of a bygone era, akin to discussions about the price of Kodak film or typewriters, rather than forward-looking economic concerns.

6. Beyond "Enough": Re-evaluating Economic Priorities

Perhaps the most profound economic fallacy perpetuated in political discourse is the implicit assumption that endless economic growth and material accumulation are the primary drivers of societal well-being. From a philosophical and sociological perspective, many advanced economies, including the U.S., passed the point of "enough" decades ago, meaning that basic needs and a comfortable standard of living are broadly attainable for the majority. The constant striving for "more" often reflects a societal obsession rather than a genuine need.

While income and wealth inequality remain significant challenges that necessitate progressive tax policies and social safety nets to foster a more equitable and peaceful society, it is also observed that beyond a certain threshold, increased wealth does not correlate with increased happiness. This phenomenon, explored in studies like the Easterlin Paradox, suggests that contentment is more closely tied to mindset, community, health, and life skills than to a larger paycheck. If political leaders were truly committed to enhancing the happiness and well-being of their constituents, their platforms might prioritize investments in public health, education, environmental sustainability, and community building, rather than solely focusing on economic metrics that often fail to capture the nuances of human flourishing.

Ultimately, the political arena is often driven by the imperative to win elections, which can diverge significantly from the pursuit of policies that genuinely serve the long-term best interests of the nation. For informed citizens, the approach remains one of critical engagement: cast an educated vote based on facts and principles, then redirect focus to the aspects of life and personal finance that are within one’s direct control.

Further Resources for Data-Driven Insights:

For those seeking to navigate the complex economic landscape with factual data, resources like "USA Facts" (usafacts.org), founded by former Microsoft CEO Steve Ballmer, offer an invaluable service. This initiative provides well-produced videos and comprehensive data visualizations that present objective U.S. government statistics without political spin, allowing individuals to form their own conclusions based on evidence rather than partisan rhetoric. Such initiatives underscore the critical need for data literacy in an age of abundant information and pervasive misinformation.

The ongoing election season serves as a powerful reminder of the importance of economic literacy and critical thinking. By understanding the underlying mechanisms of the economy and distinguishing fact from fiction, citizens can make more informed decisions, both at the ballot box and in their personal financial lives.