The global financial landscape has undergone a dramatic transformation as interest rates, after an unprecedented period of near-zero levels, have surged to their highest points in over two decades. This abrupt shift, initiated by central banks globally, most notably the U.S. Federal Reserve, marks a significant departure from the economic norms that have prevailed since the 2008 financial crisis and the subsequent COVID-19 pandemic response. The implications are far-reaching, affecting everything from consumer borrowing and housing markets to corporate investment and overall economic stability.

A Decades-Long Era Concludes

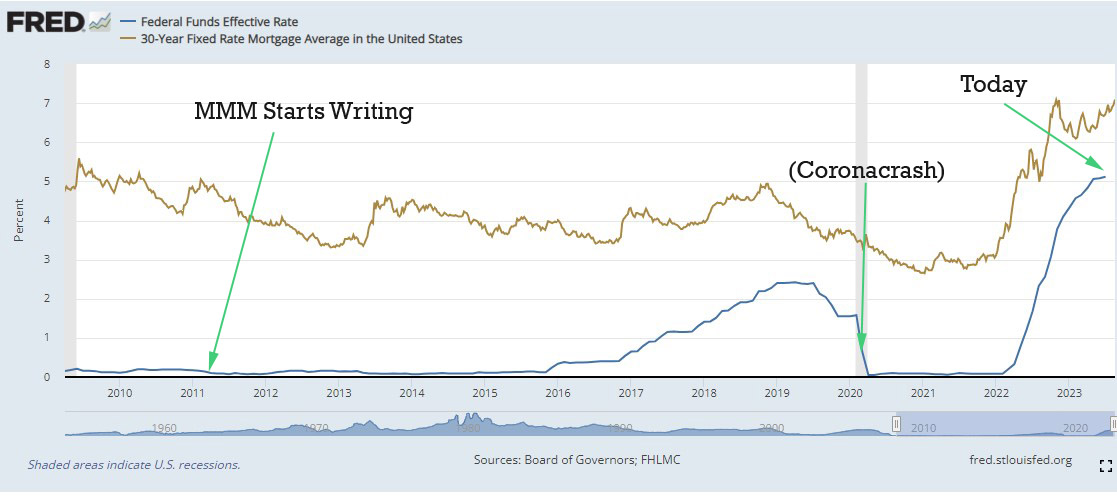

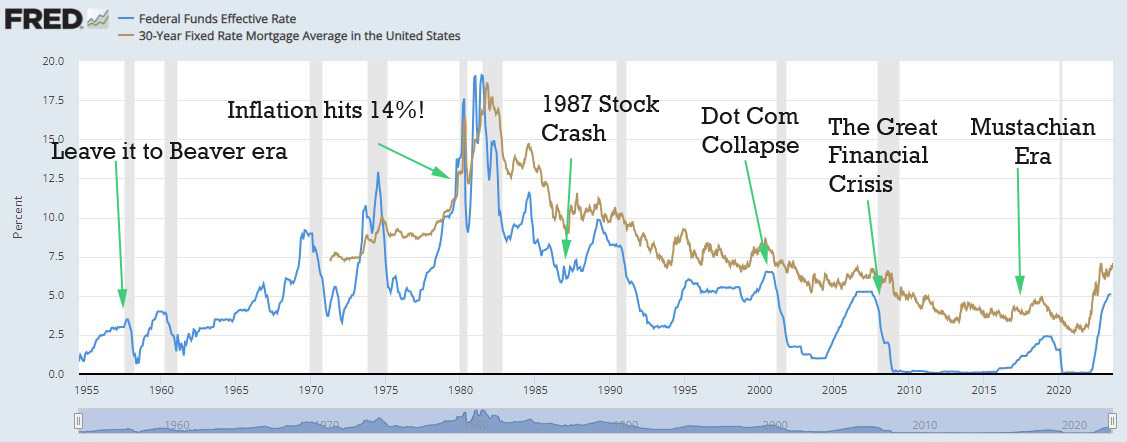

For much of the past fourteen years, and particularly since the Great Recession, central banks pursued accommodative monetary policies characterized by historically low interest rates. The Federal Funds Rate, the benchmark rate set by the U.S. Federal Reserve, hovered near 0% for extended periods, notably from December 2008 to December 2015, and again from March 2020 to March 2022 in response to the COVID-19 pandemic. This era of cheap money was designed to stimulate economic growth, encourage borrowing and investment, and keep inflation at a stable, low level.

These policies made mortgages exceptionally affordable, fueling robust demand in the housing market and driving up home prices. Businesses also benefited from inexpensive capital, leading to increased investment in new ventures, expansion of existing operations, and a surge in hiring. The resulting economic dynamism fostered a period of sustained prosperity, marked by innovation, job creation, and rising living standards in many developed economies.

However, the prolonged period of easy money eventually contributed to an imbalance. By late 2021 and early 2022, a confluence of factors – including persistent supply chain disruptions exacerbated by the pandemic, strong consumer demand bolstered by fiscal stimulus, and geopolitical events – led to a rapid and concerning acceleration of inflation. The U.S. Consumer Price Index (CPI) reached a peak of 9.1% year-over-year in June 2022, far exceeding the Federal Reserve’s target of 2%.

The Federal Reserve’s Aggressive Response to Inflation

Faced with rapidly escalating inflation, central banks pivoted sharply towards monetary tightening. The U.S. Federal Reserve, under Chairman Jerome Powell, began a series of aggressive interest rate hikes in March 2022. The federal funds rate, which started at a target range of 0-0.25%, was systematically increased through eleven consecutive hikes, reaching a range of 5.25-5.50% by July 2023. This rapid increase was the most aggressive tightening cycle in decades, aimed at cooling down the overheated economy and bringing inflation back under control.

The mechanism is straightforward: by raising the federal funds rate, the Fed increases the cost of borrowing for commercial banks, which, in turn, translates into higher interest rates across the economy for consumers and businesses. This "gas pedal" analogy, as sometimes used, illustrates the Fed’s attempt to slow the economic engine by making money more expensive, thereby reducing demand and inflationary pressures.

Broad Economic Implications

The shift to higher interest rates has permeated every corner of the economy, prompting widespread re-evaluation of financial strategies and spending habits.

-

Consumer Impact: For the average consumer, the most immediate and tangible effect has been on borrowing costs. Mortgage rates, particularly for 30-year fixed-rate loans, surged from historical lows of around 3% in 2020-2021 to over 7% by late 2022 and into 2023. This dramatic increase has significantly diminished housing affordability, making homeownership a more distant dream for many prospective buyers. Similarly, interest rates on credit cards, auto loans, and other forms of consumer credit have risen, increasing the financial burden on households. Conversely, savers have seen a silver lining, with higher yields on savings accounts, money market funds, and certificates of deposit (CDs), offering better returns on cash holdings than in years past.

-

Business Sector Adjustments: Companies are facing substantially higher costs for borrowing capital, impacting investment decisions and expansion plans. Startups and businesses reliant on venture capital or debt financing find it more expensive to secure funds, leading to a slowdown in new projects and a greater emphasis on profitability over growth. Major corporations, including tech giants like Meta (Facebook) and Amazon, have announced significant layoffs, shedding tens of thousands of employees. While these actions are often attributed to a re-calibration after pandemic-era hiring sprees, the increased cost of capital and a generally more cautious economic outlook play a significant role. The banking sector also experienced turbulence, with a "miniature banking crisis" in March 2023 seeing the collapse of several mid-sized banks, including Silicon Valley Bank, which had invested heavily in long-term bonds that lost value as interest rates rose.

-

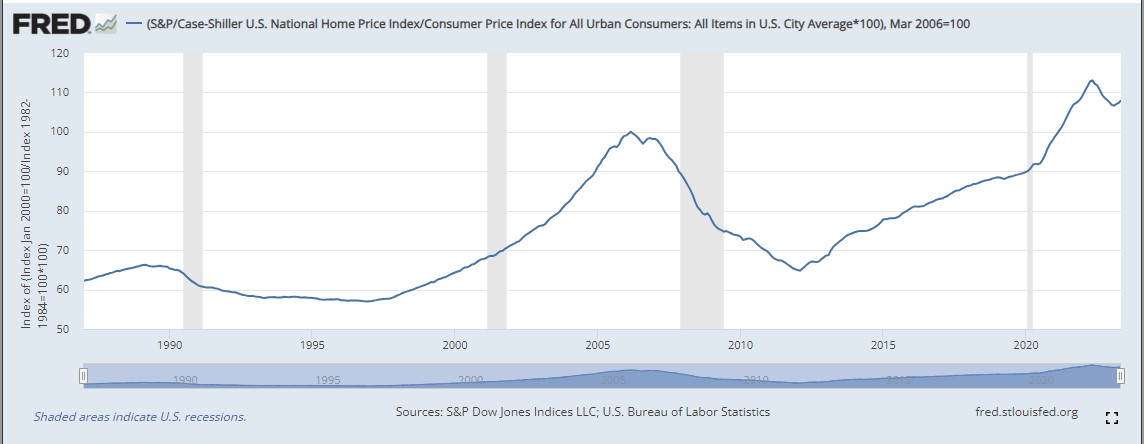

The Housing Market’s New Reality: The housing market, which had seen unprecedented price growth, has begun to cool. Higher mortgage rates have significantly reduced buyer demand and affordability. For instance, a $400,000 home with a 10% down payment, financed at 3% interest, would have an estimated monthly payment of $1,518 (principal and interest). At 7.5%, the same home’s payment jumps to $2,518 – an increase of over $1,000 per month. This stark change has led to a decrease in home sales volume and, in some areas, a moderation or even slight decline in prices. Homeowners with existing low-rate mortgages are reluctant to sell, creating a "lock-in" effect that reduces inventory and can paradoxically support prices in some segments. Economists suggest that the market is undergoing a necessary adjustment, as the tough medicine of higher rates aims to bring prices back into alignment with sustainable affordability levels.

Investment Strategies in a High-Rate Environment

The landscape for investors has also shifted. The stock market, which thrived during the low-rate era, has experienced volatility. From its peak in early 2022 to mid-2023, the overall U.S. market, as represented by indices like the S&P 500, saw a correction, with some periods of significant decline. While market timing remains notoriously difficult, the current "discount" on stock prices makes long-term investing more appealing to some.

The question of allocating between stocks and cash/bonds has become more complex. With savings accounts and short-term Treasury bills offering yields of 4.5% to 5.5%, the opportunity cost of investing in potentially volatile equities has increased. However, financial advisors generally emphasize a long-term perspective, noting that historically, the stock market has consistently outperformed other asset classes over extended periods, even accounting for downturns. A diversified approach, balancing exposure to equities with fixed-income assets, remains a common recommendation.

The Enigma of Future Interest Rates and Economic Trajectory

Predicting the future trajectory of interest rates and the broader economy is inherently challenging. While current rates are considered "high" relative to the recent past, a broader historical perspective reveals they are closer to the long-term average. Examining interest rate trends over the past seventy years shows that rates around 5% have been common for extended periods, suggesting that the near-zero era was an anomaly rather than the norm.

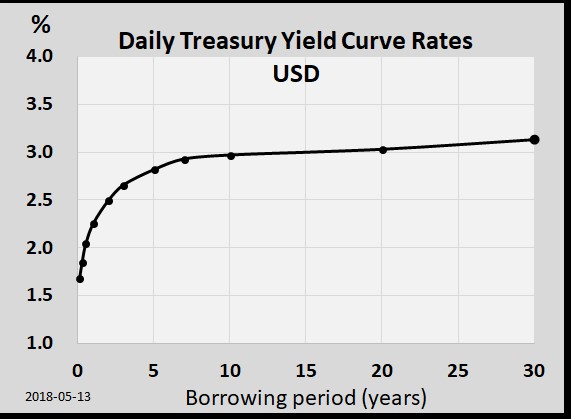

One critical indicator for future interest rate movements is the U.S. Treasury Yield Curve. Typically, lenders expect higher returns for locking up money over longer periods, resulting in an upward-sloping yield curve (long-term rates higher than short-term rates). However, the current environment features an inverted yield curve, where short-term Treasury yields (e.g., 1-year or 2-year) are higher than long-term yields (e.g., 10-year). As of August 2023, for instance, a 1-year Treasury offered around 5.4%, while a 10-year Treasury yielded approximately 4.05%.

An inverted yield curve is a historically reliable predictor of future economic slowdowns or recessions. It has preceded ten of the last eleven U.S. recessions over the past 75 years, indicating that bond market participants anticipate interest rates will fall in the future, typically in response to a weakening economy that prompts the Fed to ease monetary policy.

Economists and analysts widely interpret the inverted yield curve as a strong signal that the economy is likely to experience a downturn in the near future, potentially within the next 12 to 24 months. This recession, if it materializes, would likely be characterized by cooling inflation and rising unemployment, which would then create the conditions for the Federal Reserve to begin cutting interest rates.

Adapting to a New Financial Paradigm

In this evolving economic climate, individuals and businesses are urged to adopt strategies that prioritize financial resilience and adaptability. For individuals, maintaining a lean lifestyle, managing debt effectively, and building emergency savings are paramount. For those contemplating major purchases like homes, the current environment necessitates careful consideration of affordability and the potential for future market adjustments. The ability to act on opportunities, whether in real estate or other investments, is enhanced by having liquid savings and a strong financial position, independent of external borrowing costs.

The current period of higher interest rates is not merely a temporary blip but a significant recalibration of economic forces after a protracted period of unusual monetary policy. While the adjustment can feel challenging, it represents a return to more historically normal conditions. Navigating this landscape successfully will require informed decision-making, a long-term perspective, and a focus on personal financial fundamentals, allowing individuals to weather market fluctuations and capitalize on emerging opportunities. The ultimate lesson from this shift is the enduring importance of sound financial planning and the ability to adapt to changing economic tides.