The global financial landscape has been gripped by a remarkable surge in stock market valuations over the past several years, prompting both excitement among investors and caution from analysts. This sustained ascent, particularly noticeable in the S&P 500 index, has seen retirement portfolios expand dramatically, leading some long-term investors to question the sustainability of current market levels and the underlying drivers of this growth.

An Unprecedented Market Surge

In a period marked by rapid technological advancement and evolving economic conditions, the S&P 500 index, a benchmark for broad U.S. equity performance, has delivered extraordinary returns. Over the past two years, the index has climbed approximately 57%, and over the last five years, its value has more than doubled. This exponential growth has significantly boosted the net worth of many individuals, particularly those with substantial retirement savings allocated to diversified index funds. For some, the journey to financial independence, once a distant aspiration during the "Covid Era," now appears unexpectedly complete. Others, already retired, find themselves with amplified wealth, potentially influencing spending habits or investment decisions.

This rapid appreciation naturally raises fundamental questions: Is this growth a genuine reflection of economic strength and corporate profitability, or does it represent a speculative bubble, a financial illusion poised for correction? Concerns about market overvaluation are not new, but the current environment, heavily influenced by the burgeoning field of Artificial Intelligence (AI), adds a unique layer of complexity.

Decoding Valuations: The Price-to-Earnings Conundrum

To understand the current market dynamics, it’s essential to revisit the fundamental principles of stock valuation. A stock represents a fractional ownership in a company, akin to owning a rental property. Just as a rental property generates income from rent, a stock represents a claim on a company’s future earnings. The value an investor places on these future earnings is often reflected in the Price-to-Earnings (P/E) ratio, which compares a company’s share price to its per-share earnings.

Consider the analogy of a rental house: if a house generates $24,000 in annual profit and sells for $240,000, it has a P/E ratio of 10. If the market price for that same income stream doubles to $480,000, the P/E ratio climbs to 20. While the seller benefits from the higher price, the new investor faces a less attractive return on investment, as their "paycheck" (the rent collected) has not increased proportionally to the purchase price.

Applying this to the stock market, data from financial analysis platforms like multpl.com reveals a similar trend. An initial investment of $100,000 in the S&P 500 in 2019, with dividends reinvested, would today be worth approximately $256,960—a staggering 157% gain. However, the underlying share of company earnings from that same $100,000 investment has only increased from $5,290 to $7,540, a more modest 42% gain. This disparity indicates that the overall S&P 500’s P/E ratio has risen from approximately 20 in 2019 to around 30 in early 2025. This suggests that investors are currently paying a significantly higher premium for each dollar of corporate earnings than they were five years ago, implying potentially lower future returns as a percentage of portfolio value.

The Rise of the "Magnificent Seven"

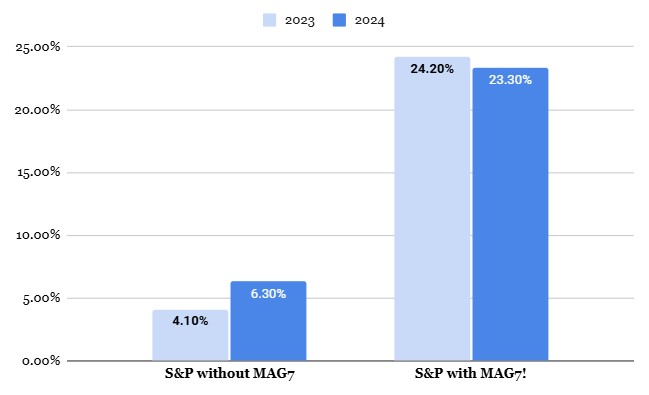

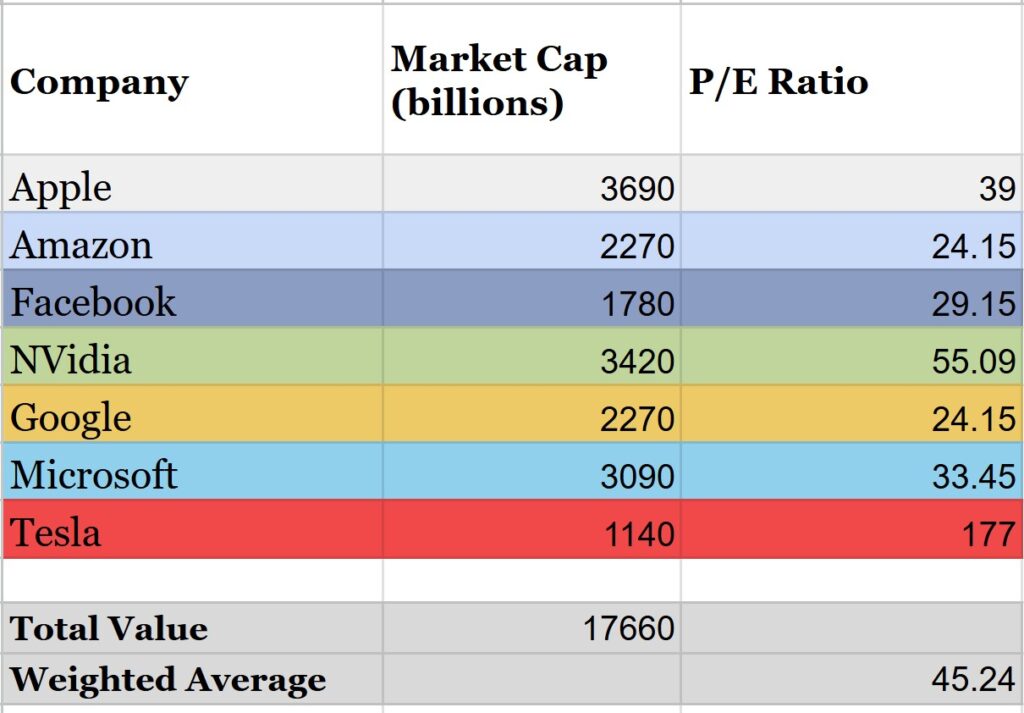

A deeper dive into the S&P 500 reveals that this market exuberance is not uniformly distributed across all 500 constituent companies. A significant portion of the recent growth—estimated at nearly three-quarters—can be attributed to just seven dominant technology companies, collectively dubbed the "Magnificent Seven": Apple, Nvidia, Microsoft, Amazon, Alphabet (Google), Meta Platforms (Facebook), and occasionally Tesla.

These companies, giants in their respective tech domains, have witnessed explosive growth and intense investor hype. Their combined market capitalization now exceeds $17.66 trillion, representing over 25% of the entire S&P 500’s value. Critically, their P/E ratios are considerably higher than the broader market, with a weighted average P/E of around 45. In contrast, if these seven companies are excluded, the remaining 493 companies in the S&P 500 exhibit a more "reasonable" P/E ratio of approximately 20, though still above historical averages. This bifurcation suggests that while the overall U.S. economy is expected to remain robust, investors are forecasting exceptionally rapid and sustained growth specifically from these leading tech firms.

Artificial Intelligence: The Driving Force and Its Implications

The common thread underpinning the stratospheric valuations of the Magnificent Seven, and indeed the broader market’s optimistic outlook, is the transformative potential of Artificial Intelligence. Recent breakthroughs in AI, particularly in generative AI and large language models, have astonished the business world with their ability to perform human-like reasoning across diverse applications. This has ignited a frenzy of investment and innovation, with widespread anticipation of a new era of unprecedented productivity gains.

The initial phase of this AI boom is characterized by massive infrastructure investments. Six of the Magnificent Seven companies are committing hundreds of billions of dollars to construct colossal data centers filled with advanced supercomputers. The seventh, Nvidia, stands as a primary beneficiary, manufacturing the specialized chips (GPUs) essential for AI computation, allowing them to command premium prices amidst insatiable demand.

Beyond infrastructure, the ripple effects of AI are projected to permeate every industry. AI’s capabilities extend from analyzing complex legal documents and novels to identifying software bugs, powering autonomous vehicles, accelerating medical diagnostics, designing novel pharmaceuticals, and even animating humanoid robots for labor. The overarching vision is an "infinite workforce" of highly intelligent AI agents, working tirelessly and freely, thereby removing historical constraints on human intelligence and labor supply.

While many experts, including those closely observing the field, believe these predictions may eventually materialize, the timeline remains uncertain. The critical question for investors is whether the projected profits will truly materialize at the levels currently priced into stock valuations. Potential headwinds include unforeseen cost overruns, intensifying competition, regulatory challenges, and the inherent unpredictability of rapidly evolving technologies. Furthermore, the societal implications of widespread AI adoption, such as potential mass unemployment and significant shifts in wealth distribution, introduce an element of systemic risk that warrants careful consideration. The specter of a future dominated by a few ultra-wealthy AI proprietors, while others struggle with job displacement, is a scenario that some futurists and economists are beginning to explore.

Historical Context and Future Projections

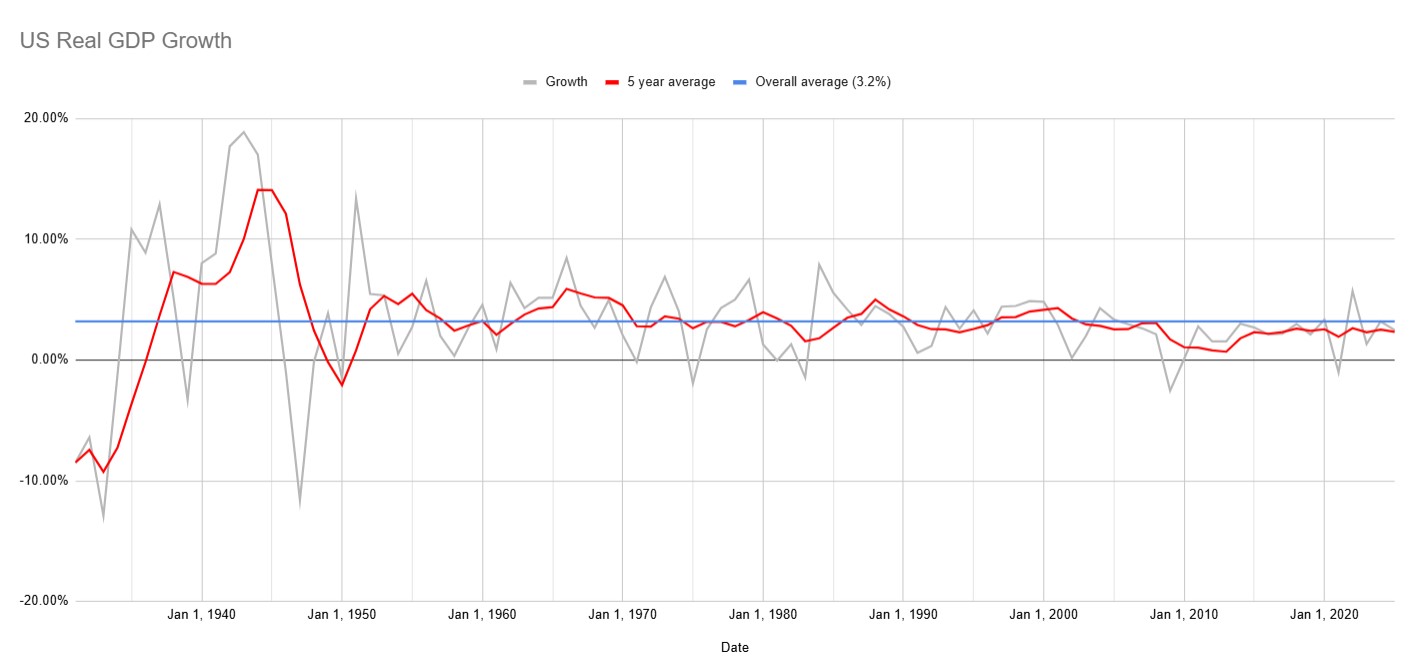

Despite the excitement surrounding AI and the current market surge, historical economic data offers a sobering perspective. Over the long term, U.S. economic growth, as measured by real GDP after inflation, has averaged a surprisingly consistent figure of about 3% per decade. Interestingly, recent decades have shown slightly slower-than-average growth, providing even less historical justification for the current elevated stock market valuations, unless a fundamental paradigm shift is indeed underway due to AI.

Given these dynamics, financial institutions are offering varied outlooks. Vanguard, a leading provider of index funds, issues annual ten-year forecasts for future returns. Their most recent projections indicate that international stocks and even bonds are expected to outperform U.S. stocks over the coming decade. This forecast is partly predicated on the significantly lower P/E ratio of international stocks (e.g., the VXUS fund has a P/E of approximately 15.9), suggesting they are trading at a substantial discount compared to their U.S. counterparts. However, it’s worth noting that Vanguard has made similar predictions in previous years, only for U.S. equities to continue their outperformance, largely driven by the U.S.-centric AI boom.

Navigating the Current Investment Landscape

For individual investors, the current environment presents a paradox: substantial unrealized gains coupled with concerns about future returns. While it is generally accepted that long-term stock ownership remains profitable, the anticipated returns from purchasing equities at today’s higher P/E ratios are likely to be lower than those enjoyed during periods of "discounted" valuations.

Diversification remains a cornerstone strategy. For instance, a diversified portfolio, such as those offered by robo-advisors like Betterment, which allocates across various asset classes including international stocks and bonds, aims to achieve higher risk-adjusted returns with lower volatility. Although a U.S.-only portfolio has historically outperformed over the past decade, largely due to the tech boom, a globally diversified approach could prove more resilient if valuations normalize across markets. The Betterment core portfolio, with its weighted average P/E ratio of approximately 22, represents a more moderate valuation compared to the S&P 500’s current level.

Even seasoned investors like Warren Buffett, the "Oracle of Omaha," signal caution. Berkshire Hathaway, his conglomerate, currently holds a record $334 billion in uninvested cash, a clear indication that Buffett perceives few attractive investment opportunities at current market prices. He has even refrained from significant share repurchases of Berkshire Hathaway stock, deeming it slightly overvalued at its current P/E ratio of around 21.

Another practical consideration for individuals is debt management. While conventionally, maintaining a low-interest mortgage and investing surplus cash into index funds has been a favored strategy, the calculus shifts with higher interest rates. A 7% mortgage, for example, offers a guaranteed return on investment when paid off, potentially making it a competitive alternative to market investments with uncertain future returns. Paying off a mortgage can be likened to acquiring a 7% bond, offering a secure, tax-free yield, which is often preferable to holding large sums in low-yield checking or savings accounts.

Risk and Resilience: Addressing Bubble Concerns

Ultimately, the future trajectory of the market remains unknowable. While occasional market manias, panics, and crashes are an inherent part of financial cycles, attempting to "time the market" by selling assets now in anticipation of a future downturn is a strategy fraught with risk and historically proven to be largely unsuccessful for most investors.

Over the long run, even if stock valuations revert to more typical historical averages, economic growth and corporate earnings are expected to continue their upward trend. This scenario might translate into a less aggressive growth trajectory for portfolios than the recent past, but still a positive one. Investors should manage expectations, understanding that the extraordinary returns of the past five years are unlikely to be sustained indefinitely.

Beyond the immediate financial implications, the rise of AI presents broader societal challenges and opportunities. Ethical considerations surrounding AI development, the need for robust regulatory frameworks, and proactive strategies to address potential job displacement will become increasingly critical policy debates.

In conclusion, while the current stock market exhibits elevated valuations, largely propelled by optimism surrounding Artificial Intelligence, the fundamental principles of long-term investing endure. Diversification, a disciplined savings approach, and a focus on financial well-being rather than short-term market fluctuations remain paramount. Engaging with the natural world and prioritizing personal health and relationships offers a guaranteed "return" that no financial market can replicate.

Further analysis of market trends and economic forecasts is available from reputable sources such as The Economist, which offers comprehensive global economic news and analysis.