In a move that has captured the attention of the financial independence community, Peter Adeney, widely known as Mr. Money Mustache, has announced the acquisition of a 2023 Tesla Model Y. This purchase, a significant investment for any individual, carries particular weight given Adeney’s long-standing public advocacy for extreme frugality and his critical stance on consumerism, especially regarding automobiles. The transition from a 23-year-old, $4,500 Honda van to a new electric crossover with a net cost of approximately $52,000 after taxes and credits, marks a notable shift in Adeney’s approach to personal finance in early retirement, prompting discussions about the evolving landscape of wealth management post-financial independence.

The Paradigm Shift: From Frugality to Strategic Spending

The acquisition of the Tesla Model Y by Mr. Money Mustache is more than just a personal vehicle upgrade; it represents a publicly articulated evolution in his financial philosophy. For over a decade, Adeney has been a leading voice in the Financial Independence, Retire Early (FI/RE) movement, advocating for aggressive savings rates, minimalist living, and a general disdain for what he terms "car culture" and unnecessary expenditure. His blogs have consistently championed cycling, walking, and maintaining older, reliable vehicles as cornerstones of a cost-effective and environmentally conscious lifestyle. This latest purchase, therefore, stands in stark contrast to his established brand, inviting scrutiny and serving as a case study for the psychological and practical challenges of spending after accumulating substantial wealth. Adeney himself acknowledges the apparent contradiction, framing it as an "experiment in spending more" and a deliberate effort to overcome ingrained frugal habits that may, paradoxically, hinder overall life satisfaction in retirement.

Mr. Money Mustache: A Pillar of the FI/RE Movement

Peter Adeney launched the Mr. Money Mustache blog in 2011, quickly becoming one of the most influential figures in the global FI/RE movement. His core message revolved around achieving financial independence through diligent savings, smart investments, and drastically reducing living expenses. Adeney famously retired at age 30, a feat he attributed to living on a mere fraction of his income and optimizing every aspect of his spending. His direct, often provocative writing style, combined with practical advice on topics ranging from DIY home repairs to efficient energy consumption, resonated with millions seeking an alternative to the traditional career path. The FI/RE movement, which gained significant traction during the 2010s, emphasizes high savings rates (often 50-70% of income), intelligent investing, and the aggressive elimination of debt to achieve a "nest egg" sufficient to cover living expenses, typically using the "4% rule" as a guideline for safe withdrawal rates. For many followers, Adeney’s personal decisions and public pronouncements have served as a benchmark for what truly committed frugality looks like.

The New Acquisition: A Detailed Look at the Tesla Model Y

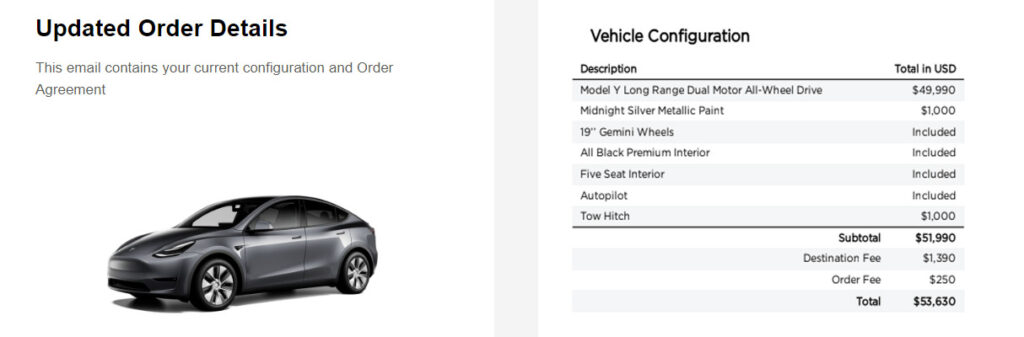

The 2023 Tesla Model Y that Adeney has purchased is a premium electric crossover SUV, renowned for its performance, technology, and environmental credentials. The specific configuration acquired includes all-wheel drive, offering enhanced traction and stability, and boasts acceleration capabilities comparable to high-performance sports cars. With seating for up to seven people, it also provides significant cargo and passenger space, a critical factor for Adeney’s family and his burgeoning "Carpentourism" activities. The vehicle is equipped with advanced computer gadgetry, including a sophisticated infotainment system, comprehensive autopilot features, and over-the-air software updates, positioning it at the forefront of automotive innovation. The choice of an electric vehicle (EV) aligns with broader environmental considerations, offering zero tailpipe emissions and potentially lower operating costs compared to internal combustion engine (ICE) vehicles, particularly when charged using renewable energy sources. This aspect partially reconciles the purchase with Adeney’s long-held values of sustainability, despite the vehicle’s luxury price point.

The Financial Rationale: Cost, Credits, and Long-Term Savings

The financial details of the Tesla Model Y acquisition are particularly illuminating. The net cost to Adeney, after accounting for various taxes and federal tax credits, is approximately $52,000. This figure stands in stark contrast to the $4,500 he paid for his previous vehicle, a Honda van purchased used twelve years ago via Craigslist. The cost difference of over $47,000 underscores the scale of this financial decision.

While the upfront cost is substantial, the long-term financial implications of owning an EV like the Model Y can present a different picture. Operating costs for electric vehicles are typically lower due to reduced fuel expenses (electricity being cheaper than gasoline in many regions, especially when charging at home), fewer moving parts leading to less maintenance, and potential savings on oil changes and other routine services required by ICE vehicles. Government incentives, such as federal tax credits (e.g., up to $7,500 under the Inflation Reduction Act for qualifying EVs), state rebates, and local utility incentives, further reduce the effective purchase price, making premium EVs more accessible.

Adeney estimates the Tesla will cost him an additional $10,000 per year compared to his old van, primarily due to depreciation, higher insurance premiums, increased electricity consumption, and registration fees. However, this calculation omits the significant maintenance costs that an aging vehicle like his 23-year-old Honda van would increasingly incur. The shift to an EV also mitigates exposure to volatile gasoline prices and contributes to a smaller carbon footprint over the vehicle’s lifespan, aligning with broader sustainability goals.

The Catalyst for Change: A Frugalist’s Internal Battle

The decision to purchase the Tesla was not impulsive but rather the culmination of years of internal deliberation and external nudges. Adeney openly discusses his "procrastination" on buying an expensive car for four years, despite suggestions from friends and readers. This hesitancy highlights a common psychological phenomenon among highly frugal individuals: a deep-seated aversion to spending, even when financially capable. He describes the internal conflict using the metaphor of "Grocery Shopping With Your Middle Finger," a mental battle waged over seemingly trivial expenses, like a $6.99 loaf of bread, despite having ample financial resources.

The ultimate catalyst for the purchase was the increasing unreliability of his beloved Honda van, affectionately named "Vanna." After dutifully serving for 12 years, traversing mountains and deserts, and assisting in numerous home renovation projects, Vanna experienced a "final hot and smelly transmission failure on a mountain pass." This mechanical breakdown, occurring on the way home from a new project in Salida, Colorado, provided the necessary impetus for Adeney to finally make the leap. This event transformed a persistent source of "negative stress" and missed opportunities for travel and experiences into a concrete reason for an upgrade.

"What Got You Here Won’t Get You Where You’re Going": A New Framework for Wealth Utilization

Adeney articulates a crucial piece of wisdom – "What got you here, won’t get you where you’re going" – as the philosophical underpinning for his evolving financial perspective. This principle suggests that the strategies and mindsets necessary for wealth accumulation may not be the same as those required for optimal wealth utilization and enjoyment in retirement. He and a similarly wealthy, frugal friend identified three key principles to help individuals, particularly those who have achieved financial independence through extreme frugality, to better enjoy their accumulated wealth:

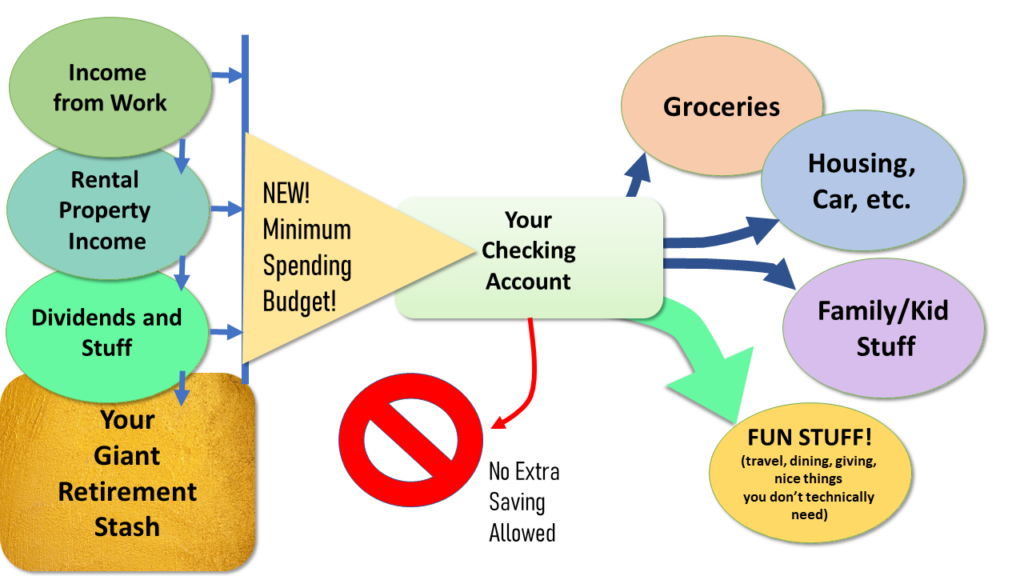

Principle 1: Establishing a Minimum Spending Budget

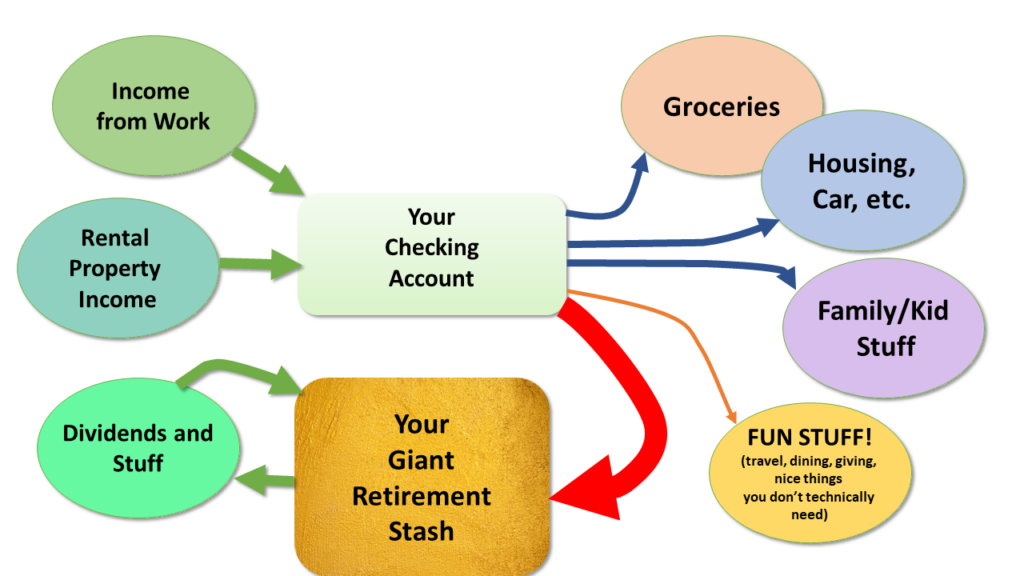

The first principle advocates for setting a "minimum spending level" rather than solely focusing on maximum savings. For someone with a $2 million investment portfolio, for instance, the widely accepted 4% rule suggests a safe annual withdrawal of $80,000. Even with a more conservative 3% withdrawal rate, this still allows for $60,000 in annual spending, often supplemented by side income, inheritances, or Social Security. Many financially independent individuals, however, continue to live on significantly less, often under $40,000 per year, out of habit. This underspending, Adeney argues, can lead to unnecessary self-deprivation and missed opportunities for enhancing life quality. By consciously setting a minimum budget, individuals can challenge their ingrained frugality and ensure they are deriving appropriate benefits from their financial freedom.

Principle 2: The Dedicated "Money Wasting" Account

To overcome the psychological barrier of spending on "frivolous" items, Adeney proposes creating a "Dedicated Money Wasting Account." This concept leverages the psychological phenomenon that people are often more comfortable spending "other people’s money" (e.g., on a business trip) than their own. By consciously allocating a portion of their wealth to this account, individuals can mentally reframe these funds as "permission to spend," thereby reducing the guilt or anxiety associated with discretionary purchases. This dedicated fund makes "splurging" feel less like a transgression against frugal principles and more like a planned, permissible allocation, encouraging enjoyment of accumulated wealth without the mental gymnastics.

Principle 3: The Splurge Accountability Buddy

Recognizing that lifelong habits are difficult to break in isolation, the third principle suggests enlisting a "Splurge Accountability Buddy." This involves teaming up with friends who share similar financial backgrounds and struggles with spending. Through mutual encouragement and constructive questioning, these "buddies" can challenge each other’s ingrained cheapness and celebrate judicious splurges. This social reinforcement mechanism provides external validation for spending decisions that might otherwise feel indulgent or wasteful. Examples cited include a wealthy friend becoming more comfortable treating his family to quality goods and experiences, and Carl (Mr. 1500 Days), another prominent FI/RE blogger, finally replacing his old minivan with a new Chevrolet Bolt EV. This peer support system helps individuals navigate the emotional complexities of spending after years of disciplined saving.

Beyond Personal Indulgence: Broader Implications for the FI/RE Community

Mr. Money Mustache’s public embrace of a "splurge" carries significant implications for the broader FI/RE community. It suggests a maturation of the movement, moving beyond the initial phase of aggressive accumulation to address the equally challenging phase of responsible decumulation and enjoyment. While extreme frugality is effective for achieving early retirement, sustaining it indefinitely can lead to burnout or regret if it prevents meaningful life experiences.

This shift encourages a more nuanced discussion within the FI/RE space: how to balance core values of sustainability and efficiency with a reasonable degree of comfort and convenience that wealth can afford. It challenges the notion that financial independence necessitates perpetual deprivation and instead advocates for a mindful allocation of resources that genuinely enhances well-being. For many followers, seeing a figure like MMM make such a move provides permission to re-evaluate their own spending habits post-FI, potentially leading to a healthier relationship with money that incorporates both disciplined saving and strategic enjoyment.

Addressing Criticisms: Philanthropy and Personal Fulfillment

Anticipating potential criticism regarding the "privileged rich folk talk," Adeney proactively addresses the argument that such funds should be directed towards charity. He underscores his own significant philanthropic contributions, having donated over $500,000 to various causes during his blogging career. This distinction highlights that personal spending and charitable giving are not mutually exclusive but can coexist within a holistic financial strategy.

Adeney argues that an excessive scarcity mindset, even after achieving financial independence and engaging in substantial philanthropy, can be counterproductive. He describes how comparing personal "meager spending" to large donation figures can lead to irrational fears of running out of money, perpetuating an unhealthy cycle of cutting back "on EVERYTHING!" He advocates for a "happy medium" where responsible stewardship of savings, generous charitable giving, and a deliberate allocation for personal enjoyment can all thrive. This perspective emphasizes that self-care and investing in personal experiences are not inherently selfish but contribute to overall happiness and well-being, which in turn can foster a greater capacity for generosity and positive societal contribution.

The Practicalities: Dispensing with the Old, Embracing the New

The practical aspects of this transition also provide useful insights. Adeney utilized an online car salvage service called Peddle to dispose of his old Honda van. The process involved a quick online assessment, resulting in an offer of $715, followed by a convenient tow-truck pickup and cash payment. This experience, framed as part of the "splurge experiment," saw the cash received being deliberately spent on "splurges like dinners out."

A key tip for effective splurging, as outlined by Adeney, is to focus on improving genuinely negative aspects of one’s life rather than merely reducing hardship or upgrading already satisfactory things. For example, a leaky roof or a stressful commute are prime targets for improvement, whereas upgrading an already beloved coffee setup might be counterproductive. For Adeney, the unreliable van represented a consistent source of "negative stress," causing him to avoid certain trips and miss potential "positive lifetime experiences." The new Tesla, with its reliability and range, transforms this dread into excitement for future road trips, camping, and "Carpentourism" ventures, including those related to his new co-ownership of a vacation rental property in Salida, Colorado.

Conclusion: A Redefinition of Financial Freedom

Mr. Money Mustache’s acquisition of a Tesla Model Y marks a significant moment for both the individual and the broader financial independence community. It underscores a pivot from a relentless focus on accumulation to a more balanced philosophy of mindful enjoyment and strategic spending in retirement. By openly discussing his internal struggles and outlining practical principles for wealth utilization, Adeney provides a valuable framework for others grappling with similar challenges.

This move does not abandon the core tenets of financial responsibility or sustainability, but rather expands upon them, demonstrating that financial freedom can encompass both prudent management and the judicious pursuit of personal comfort and experiences. The "Model Y Experiment," an ongoing tracker page for his ownership experience, promises to offer continued transparency and insights into this evolving journey. Ultimately, Mr. Money Mustache’s Tesla purchase is a testament to the dynamic nature of financial philosophy, illustrating that true financial independence is not just about reaching a monetary goal, but about cultivating a healthy, fulfilling relationship with money throughout all stages of life.