The United States Office of the Comptroller of the Currency (OCC) has officially released a notice of proposed rulemaking (NPRM) aimed at implementing the comprehensive requirements of the GENIUS Act, a landmark piece of legislation passed in July 2025. This move marks a pivotal shift in the American financial landscape, transitioning the regulation of payment stablecoins from theoretical statutory language into a concrete, operational framework. By establishing a dedicated regulatory section, the OCC is effectively integrating digital assets into the traditional federal banking system, signaling the end of the "crypto-experiment" era and the beginning of a highly regulated, institutionalized digital dollar ecosystem.

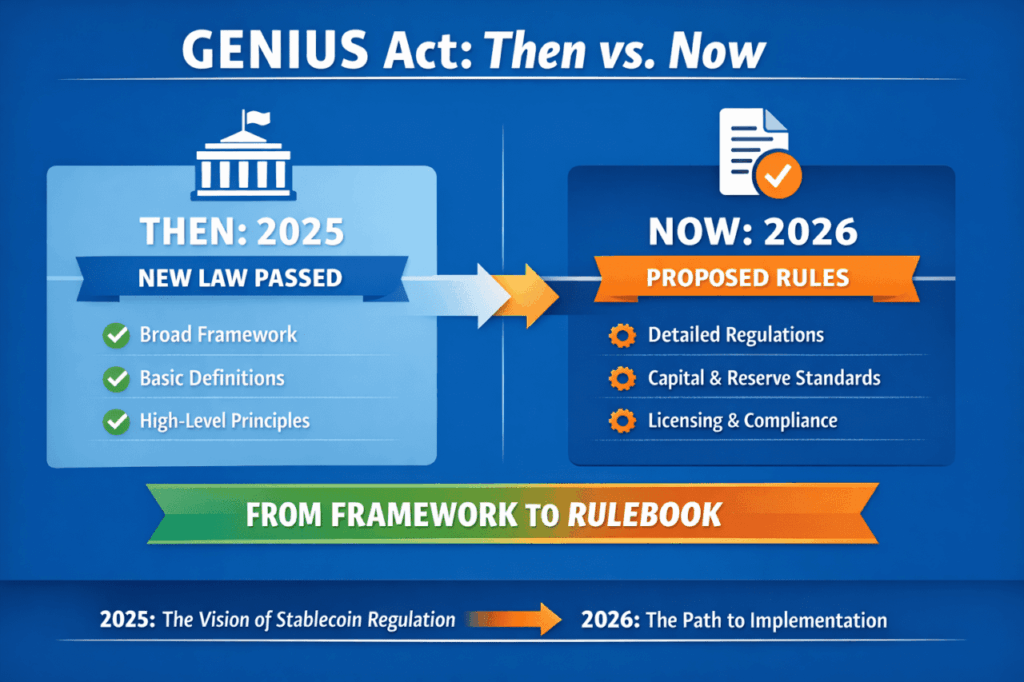

The GENIUS Act, which stands for the "Governing Essential New Infrastructure and Underpinning Stability" Act, was designed to provide the first comprehensive federal framework for stablecoins. While the 2025 Act set the legal boundaries—defining what constitutes a payment stablecoin and who may issue them—it left the technical and procedural "how" to the regulatory agencies. The OCC’s latest proposal, issued as Bulletin 2026-3, serves as the operational manual for this new era. It addresses the licensing mechanics, capital requirements, and supervisory standards that will govern any entity seeking to issue payment stablecoins in the United States.

A Chronology of Stablecoin Regulation

The path to the current NPRM has been marked by several years of intense legislative and market pressure. Following the high-profile collapses of various algorithmic stablecoins and crypto-lending platforms between 2022 and 2024, the U.S. Congress faced mounting pressure to protect the domestic financial system from contagion.

In early 2025, the GENIUS Act was introduced with bipartisan support, aiming to bring stablecoins under a regulatory umbrella similar to that of traditional deposit-taking institutions. The Act was signed into law in July 2025, establishing three core pillars: a requirement for 1:1 liquid reserve backing, a prohibition on interest-bearing stablecoins to avoid their classification as securities, and a dual federal-state oversight structure.

The March 2026 NPRM represents the final phase of this transition. With this proposal, the OCC is moving to codify these requirements into the Code of Federal Regulations (CFR), specifically under a new section: 12 CFR Part 15. This step is critical because it transforms the broad mandates of the GENIUS Act into enforceable supervisory standards that OCC examiners will use to monitor and penalize issuers.

The Four Pillars of the OCC Proposal

The OCC’s rulemaking is structured around four primary objectives designed to ensure that the stablecoin market operates with the same safety and soundness as the traditional banking sector.

1. Creation of 12 CFR Part 15

The proposal establishes a dedicated regulatory section, 12 CFR Part 15, which will house all standards and requirements for stablecoin issuers. This is a significant administrative move. By creating a unique section in the CFR, the OCC is signaling that stablecoin issuance is no longer an "ancillary" banking activity but a core function that requires its own specialized oversight body. This section will detail the ongoing reporting requirements, audit standards, and disclosure obligations that issuers must meet to maintain their status.

2. Formalized Licensing Mechanics

Under the new proposal, the process of becoming a Permitted Payment Stablecoin Issuer (PPSI) will mirror the rigor of applying for a national bank charter. Prospective issuers are required to submit a "substantially complete" application. This is not merely a registration form; it is a comprehensive dossier that must include:

- A detailed business model and three-year financial projections.

- A robust governance structure identifying key personnel and their experience.

- A granular reserve management approach, detailing exactly where and how liquid assets are held.

- Evidence of advanced technological infrastructure capable of handling high-volume transactions with near-zero downtime.

- Comprehensive risk controls, including cybersecurity protocols and anti-money laundering (AML) frameworks.

The OCC has outlined specific timelines for review, ensuring that while the process is rigorous, it remains predictable for market participants.

3. Capital and Operational Requirements

Perhaps the most significant hurdle for many current market participants is the new capital and operational mandate. While the GENIUS Act required 1:1 reserves, the 2026 NPRM goes much further. It stipulates that PPSIs must maintain minimum capital thresholds—essentially a "rainy day fund" of equity—to absorb potential operational losses.

Furthermore, the proposal requires liquidity buffers that go beyond the simple token redemption obligations. Issuers must prove they can handle "run-on-the-bank" scenarios where a significant percentage of token holders seek redemption simultaneously during a period of market stress. For fintech companies that have historically operated with lean balance sheets, these requirements may necessitate significant capital raises or structural reorganizations.

4. Treatment of Foreign Issuers

The OCC has taken a firm stance on cross-border participation. The proposal eliminates the "regulatory gray zone" that allowed offshore entities to market digital assets to U.S. consumers without federal oversight. Under the new rules, any foreign issuer serving U.S. users must:

- Apply for OCC registration.

- Provide a comparability determination from the U.S. Treasury, proving their home jurisdiction has regulations as strict as those in the U.S.

- Consent to U.S. jurisdiction and grant the OCC full access to their books and records.

- Maintain U.S.-available reserves, ensuring that assets are within the reach of U.S. courts in the event of a default.

Industry Reactions and Economic Implications

The reaction from the financial sector has been a mixture of relief and concern, largely split between traditional banks and emerging fintech firms.

Traditional Banking Perspective

Large commercial banks have generally welcomed the NPRM. For these institutions, the "compliance moat" is an advantage. Since banks already operate under heavy OCC supervision, they possess the existing infrastructure for risk management, internal audits, and capital planning. Industry analysts suggest that major banks may now move aggressively into the stablecoin space, viewing it as a more efficient way to handle cross-border settlements and interbank transfers.

"The OCC’s proposal provides the legal certainty we have been waiting for," noted a senior policy advisor at a major Wall Street trade group. "By treating stablecoin issuance as a bank-like activity, the regulator is ensuring that the same risks are met with the same rules, preventing a shadow banking system from undermining financial stability."

Fintech and Crypto Sector Concerns

Conversely, smaller fintech firms and crypto-native issuers have expressed concerns that the high cost of compliance could stifle innovation. The requirement for massive capital buffers and the complexity of the "substantially complete" application could lead to market consolidation. There is a growing fear that only the largest fintechs or those with significant venture capital backing will be able to afford the entry price into the PPSI market.

Market data suggests that the cost of maintaining the required compliance and governance infrastructure could range from $5 million to $15 million annually for mid-sized issuers, not including the opportunity cost of sidelined capital held in liquidity buffers.

Fact-Based Analysis of Broader Impacts

The implementation of the GENIUS Act through this NPRM is expected to have several long-term effects on the U.S. economy and the global digital asset market:

Institutional Adoption: With a federal "seal of approval," institutional investors who were previously sidelined due to regulatory uncertainty are likely to increase their exposure to stablecoin-based products. This could lead to a significant increase in the total market capitalization of U.S.-regulated stablecoins, which currently sits at approximately $160 billion.

Reduced Transaction Costs: As stablecoins become a standardized tool for payment, the friction in the U.S. payment system could decrease. The use of blockchain-based "programmable money" for B2B transactions could save businesses billions in wire fees and settlement delays.

Strengthening the Dollar: By creating a rigorous framework for dollar-backed stablecoins, the U.S. is effectively exporting the "digital dollar" to the global stage. This reinforces the dollar’s status as the global reserve currency in the digital age, countering the rise of central bank digital currencies (CBDCs) from competing nations.

Consumer Protection: The 1:1 reserve requirement and the prohibition of interest-bearing tokens (which often involve risky lending practices to generate yield) significantly lower the risk for the average consumer. The stablecoin becomes a true "payment tool" rather than a speculative investment.

Conclusion

The OCC’s notice of proposed rulemaking is the final bridge between the legislative intent of the GENIUS Act and the reality of the American financial system. While the transition will be challenging for many fintech players, the result is a more stable, transparent, and credible digital asset environment. By imposing bank-like standards on stablecoin issuers, the OCC is ensuring that as money evolves, the fundamental principles of safety, soundness, and consumer protection remain unchanged. The public comment period for the NPRM is expected to last 60 days, with final implementation likely by the end of 2026.