The Financial Independence, Retire Early (FIRE) movement, a philosophy centered on aggressive saving and investing to achieve financial autonomy and early retirement, has faced renewed scrutiny in the wake of recent economic shifts. A recent critique, echoing sentiments from a segment of the public, highlighted concerns that the movement’s advice may be increasingly inaccessible to those without high-income tech salaries or pre-2019 homeownership. This perspective suggests that the current economic climate, marked by escalating housing costs and complex real estate markets, presents unique hurdles for aspiring FIRE adherents.

The Core Critique: Shifting Sands of Attainability

The recent commentary, originating from a reader of a prominent FIRE blog, articulated a growing sentiment among individuals perceiving themselves as disadvantaged by current economic realities. The critique posited that many established FIRE bloggers and early retirees had benefited from advantageous conditions decades ago, specifically citing high-paying tech jobs and the ability to purchase homes at significantly lower prices before 2019. This historical context, the critic argued, renders much of the traditional FIRE advice, such as "house hacking" or "buying a fixer-upper," impractical in today’s market. The challenges cited include prohibitively high prices, elevated interest rates, and restrictive local zoning ordinances that prevent the subdivision of properties or the establishment of alternative housing solutions like Accessory Dwelling Units (ADUs). The commenter expressed a desire to hear from a new generation of FIRE advocates who can navigate these contemporary constraints.

Historical Resilience of Financial Independence Principles

The notion that the FIRE movement or its underlying principles are becoming obsolete is not unprecedented. Throughout its evolution, the pursuit of financial independence has consistently adapted to various economic landscapes. Previous periods, including the dot-com bust of the early 2000s, the 2008 global financial crisis, and subsequent periods of market volatility and inflation, have each prompted questions about the movement’s viability. In each instance, proponents have emphasized the core tenets of frugality, strategic saving, and disciplined investing as robust frameworks capable of weathering diverse economic storms. This historical adaptability suggests that the fundamental principles underpinning financial independence are less susceptible to obsolescence than the specific tactics or market conditions prevalent at any given time.

Income vs. Expenditure: A Foundational Debate

A central tenet of the FIRE philosophy, particularly as articulated by its foundational figures, revolves around the optimization of spending rather than solely the maximization of income. While acknowledging that high salaries can undeniably accelerate the journey to financial independence, the argument maintains that even substantial incomes can be squandered without prudent financial management. The existence of high-earning professionals, such as software engineers and doctors, who experience financial stress despite decades of high earnings, serves as a testament to the fact that lavish spending can negate almost any income advantage.

The emphasis, therefore, remains on streamlining expenditures, eliminating waste, and cultivating a lifestyle that prioritizes value and joy over conspicuous consumption. These "Mustachian" principles – focusing on efficiency, resourcefulness, and mindful spending – are considered universally applicable. They are not only crucial for high earners seeking to avoid lifestyle inflation but become even more indispensable for individuals on more modest incomes, enabling them to build wealth and achieve financial goals more effectively.

The Housing Conundrum: Data and Discrepancies

The most significant contemporary challenge highlighted by critics is the state of the housing market in 2024. To assess this, an examination of national and local data is imperative.

National Trends in Housing Affordability

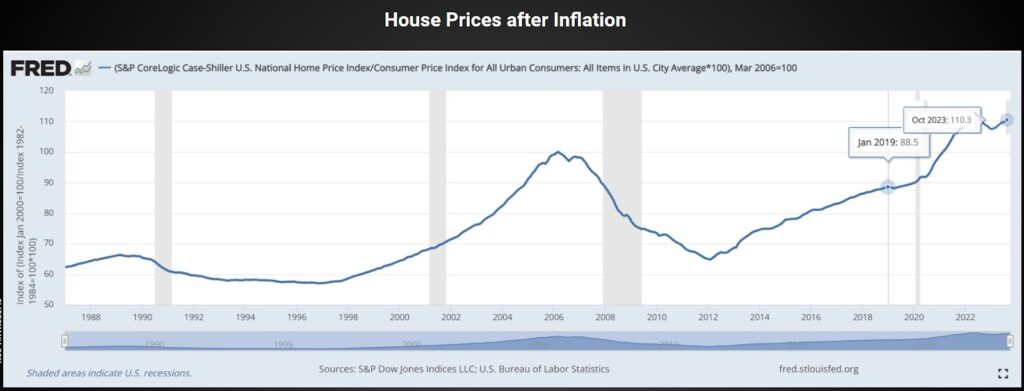

Data from the Federal Reserve Bank of St. Louis (FRED) provides a clear picture of inflation-adjusted U.S. house prices. This analysis reveals that, relative to average salaries and the overall cost of goods and services, housing prices have increased by approximately 25% since the beginning of 2019. This surge underscores a significant shift in affordability. However, it is also notable that current prices are only about 10% higher than the peak observed in early 2006, nearly two decades prior. While this offers some historical perspective, the rapid ascent since 2019, coupled with rising interest rates, presents a formidable barrier for new entrants to the housing market.

Local Market Extremes

National averages, however, often mask extreme variations in local markets. Highly desirable urban and suburban areas have experienced far more dramatic price increases. For instance, Longmont, Colorado, a city cited as an example, saw its median home price escalate from approximately $200,000 in 2005 to a staggering $540,000 in 2024. This represents a tripling of prices in less than two decades, significantly outpacing average salary growth in the region. Such localized surges render homeownership increasingly unattainable for the average person in these specific areas, challenging traditional FIRE strategies that often rely on home equity and low housing costs.

Geographical Arbitrage: A Strategic Imperative for Affordability

In response to these localized housing crises, a key strategy for maintaining the attainability of financial independence is geographical arbitrage. This involves leveraging differences in living costs by relocating from a high-cost area to a more affordable one, thereby extending the purchasing power of one’s income and savings. This approach shifts the perspective from being a victim of local market forces to actively making a strategic choice about one’s living environment.

Housing, like any other commodity, is subject to supply and demand, resulting in a wide spectrum of prices across different locations. The notion that one must reside in a specific location, even if it’s one’s birthplace, is challenged by this principle. Instead, individuals are encouraged to analyze their housing options critically, considering whether renting, buying, or implementing "house hacking" strategies is most beneficial in their current city, but also expanding this analysis to other cities and even countries.

Empowering Relocation Decisions: Data-Driven Approaches

Making informed relocation decisions requires access to comprehensive data and practical tools. Several resources can assist individuals in identifying locations that offer a better balance of lifestyle and affordability.

Domestic Exploration with FRED Data

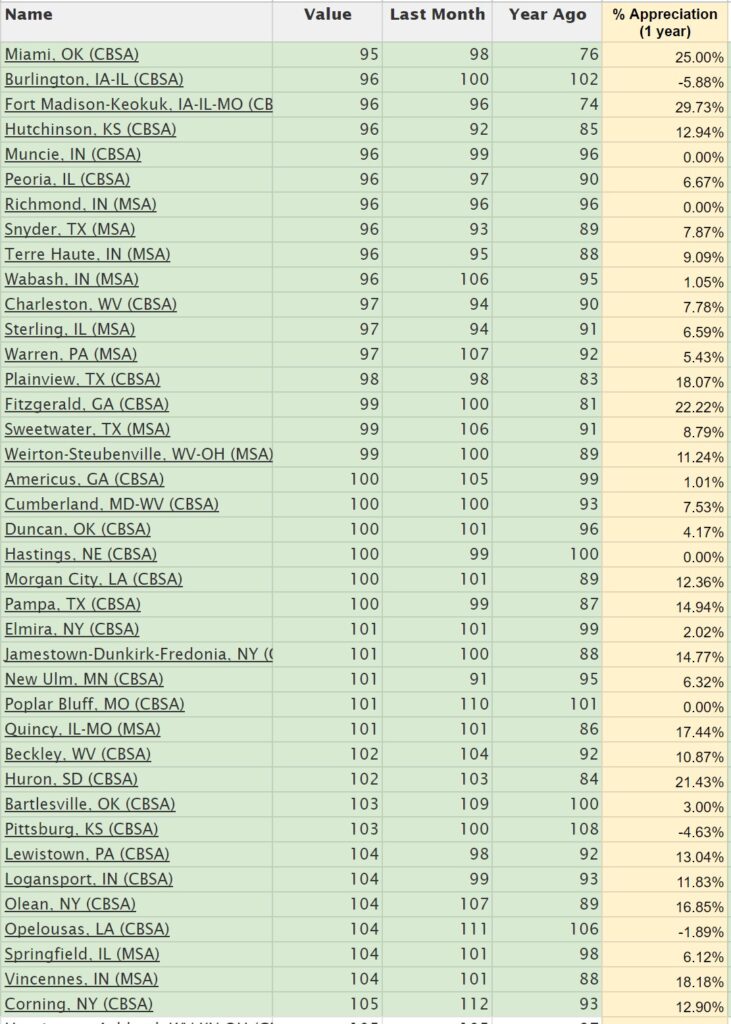

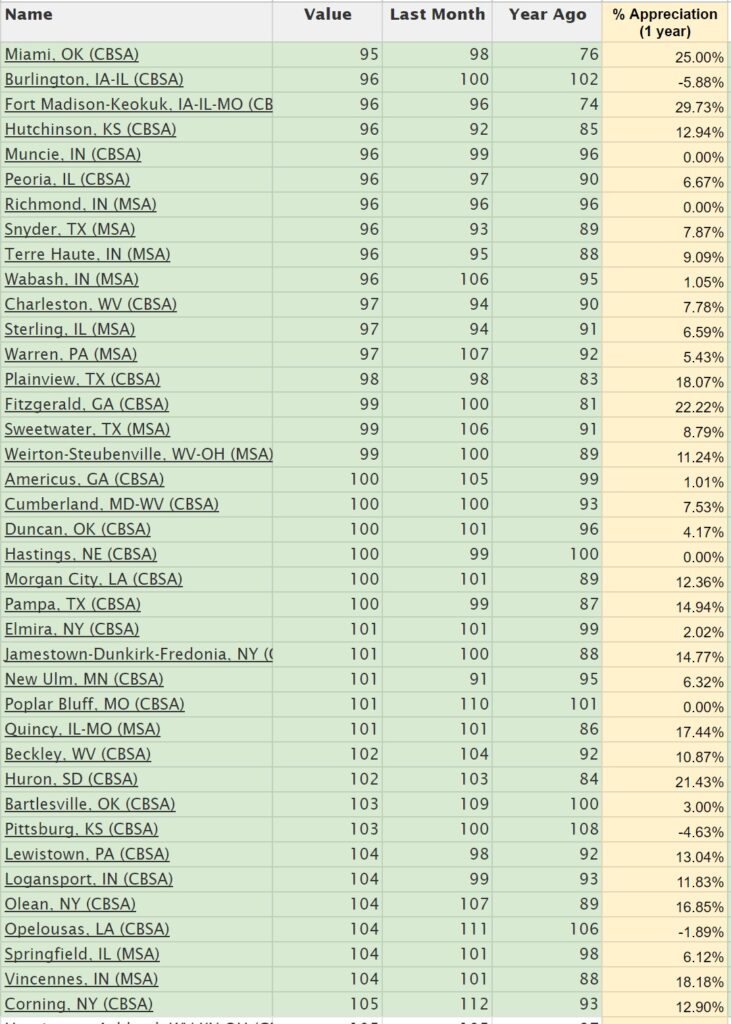

The FRED database, maintained by the Federal Reserve Bank of St. Louis, offers an invaluable list of the top 1,000 U.S. metro areas, including data on price per square foot. This metric allows for a standardized comparison of housing costs across different regions. By sorting this data, individuals can identify bands of affordable cities. For example, a focus on cities with housing costs centered around $100 per square foot could reveal numerous locations where a 2,000-square-foot home might be purchased for approximately $200,000. Additionally, analyzing the year-over-year change in house prices can offer insights into whether a market is appreciating rapidly or experiencing a plateau, aiding in future planning.

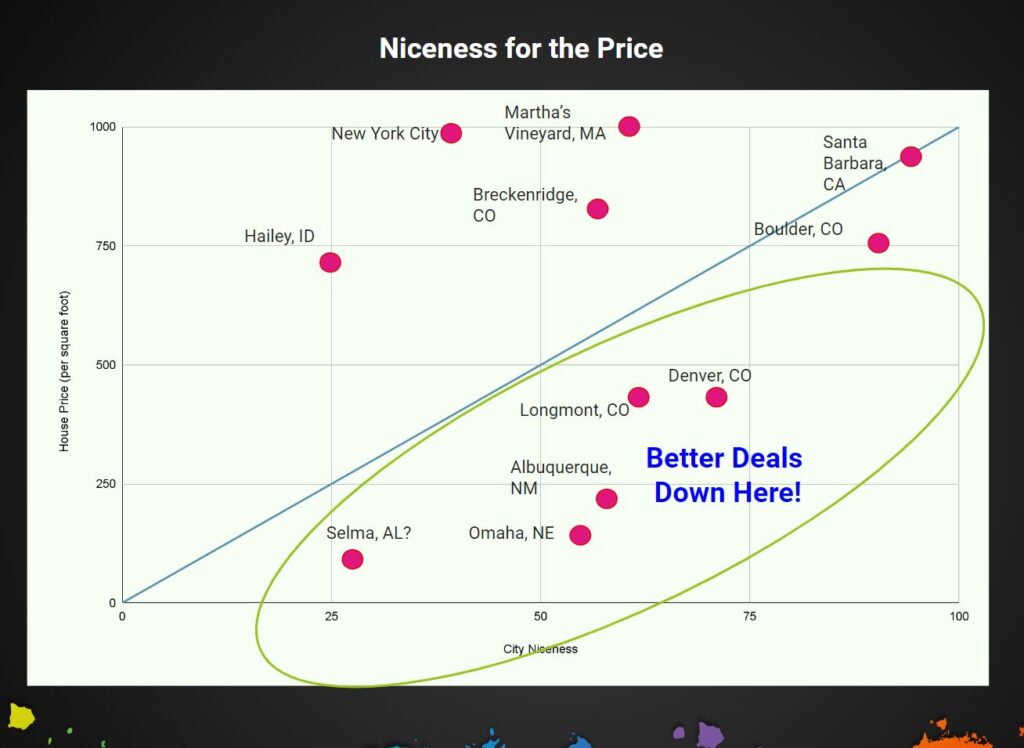

A hypothetical search, comparing cities based on a subjective "desirability" index against their price per square foot, illustrates this. While Longmont, CO, might be priced at $450 per interior square foot, a city like Albuquerque could offer lower costs, while Denver might provide a perceived nicer lifestyle at a similar price point. Boulder, CO, on the other hand, would command a significantly higher premium for an even more enhanced lifestyle. Such comparisons empower individuals to align their housing budget with their lifestyle preferences.

Comparative Analysis: Phoenix vs. Denver

A practical application of this data-driven approach involves comparing two distinct metropolitan areas. For instance, comparing the Phoenix, Arizona, metro area with the Denver, Colorado, metro area reveals that Phoenix averages approximately $272 per square foot, while Denver averages around $299 per square foot. While Denver is about 10% higher on average, the variations within neighborhoods in any major city often exceed this difference. Consequently, qualitative factors become paramount. Both regions boast abundant sunshine and access to mountain recreation, but their climates and urban characteristics differ significantly. Denver is generally more compact, while Phoenix offers sprawling towns in its foothills. The optimal choice ultimately hinges on personal preference and how one weights these various factors, with some individuals even considering a split-year residency to enjoy the benefits of both.

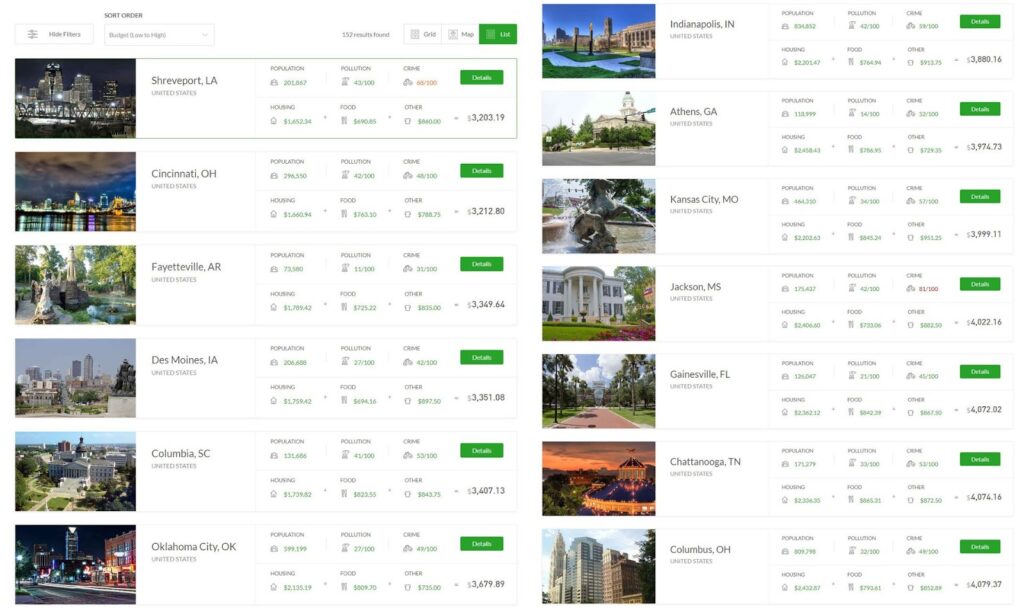

International Horizons with "The Earth Awaits"

For those willing to cast a wider net, platforms like "The Earth Awaits" offer comprehensive cost-of-living data for cities worldwide. Users can input specific criteria such as geographic area, monthly budget, family size, apartment type, and preferred temperature ranges. A search for North American cities, for example, might reveal options like Fayetteville, Columbia, or Athens, offering a desirable small-to-mid-sized city feel at an affordable price point. Similarly, extending the search to South America could yield numerous cities with significantly lower living costs, providing a rich array of options for further research. These platforms not only offer financial data but also provide population figures, giving a sense of a city’s character and potential lifestyle.

Overcoming the Inertia of Relocation

Despite the compelling financial arguments for geographical arbitrage, the prospect of relocating, especially internationally, often elicits apprehension. Individuals frequently develop strong emotional and practical ties to their current locations, making the idea of change daunting. However, it is crucial to differentiate between genuine, positive bonds and simple fear of the unknown.

The challenges associated with moving, such as navigating new laws, traditions, citizenship requirements, passports, driver’s licenses, and the administrative processes of crossing international borders, can appear formidable. Yet, these are often a series of manageable "Adulting Puzzles" rather than insurmountable obstacles. These tasks typically involve online research, phone calls, and occasional visits to official offices. While requiring some effort, the long-term benefits of moving to a more suitable and affordable environment often far outweigh the temporary inconvenience. The alternative — remaining in an unsuitable or unaffordable location, potentially requiring years of additional work to compensate for higher living costs — often represents a far greater "hassle."

Broader Implications for Lifestyle and Well-being

Strategic relocation is not solely a financial maneuver; it is a profound lifestyle choice with significant implications for overall well-being. The physical environment – encompassing community, access to nature, urban amenities, and climate – is arguably one of the most critical determinants of a happy and fulfilling life. While cost is a factor, it should not be the sole determinant. By carefully evaluating various locations, individuals can strategically position themselves along a "niceness for the price" spectrum, optimizing their living conditions to gain more value and satisfaction from their lives. This could involve a major international move or simply a relocation within the same city to be closer to work, nature, or cherished social networks.

Expert Perspectives and Future Outlook for FIRE

The increasing adoption of remote work, accelerated by the pandemic, has further empowered geographical arbitrage. This trend allows individuals to maintain their income levels while drastically reducing their cost of living by moving away from high-salary, high-cost metropolitan hubs. Economists and urban planners are increasingly observing these migration patterns as a natural market response to housing imbalances. Financial advisors are also recognizing and recommending strategic relocation as a legitimate and powerful tool within a comprehensive financial independence plan. The future of the FIRE movement will likely be characterized by greater flexibility, a global perspective on living arrangements, and an emphasis on lifestyle design that integrates financial prudence with personal well-being.

Conclusion

The criticisms regarding the attainability of financial independence in the current economic climate, particularly concerning housing, are valid and reflect genuine challenges. However, the core principles of the FIRE movement demonstrate a historical capacity for adaptation. By shifting focus from perceived external limitations to internal choices, and by leveraging data-driven approaches to housing decisions, individuals can actively shape their financial trajectories. Whether through rigorous spending optimization, strategic domestic relocation, or adventurous international moves, the pursuit of financial independence remains fundamentally a choice. The rewards for thoughtful consideration and proactive effort in these decisions are substantial, fostering a life that is both financially secure and personally enriching.