The financial technology landscape across East and Southern Africa is undergoing a period of rapid transformation, characterized by significant capital injections, the modernization of national payment infrastructures, and the formalization of small business financial services. In a series of landmark developments this month, fintech enterprises in Zambia, Ethiopia, and Rwanda have secured new funding and launched critical infrastructure projects aimed at narrowing the financial inclusion gap. These initiatives reflect a broader regional trend where digital-first solutions are increasingly replacing traditional banking hurdles, particularly for unbanked populations and small-to-medium enterprises (SMEs) that have historically been excluded from the formal economy.

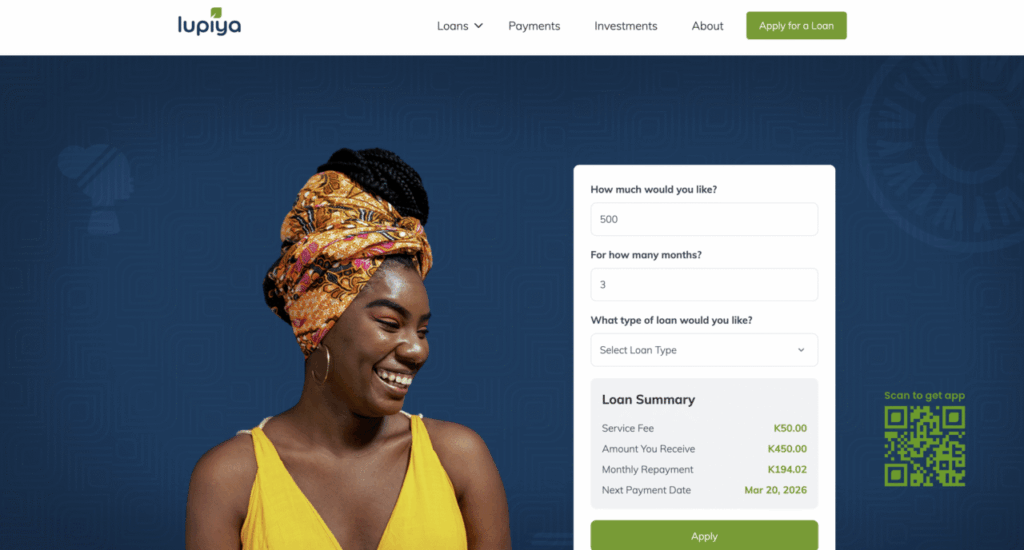

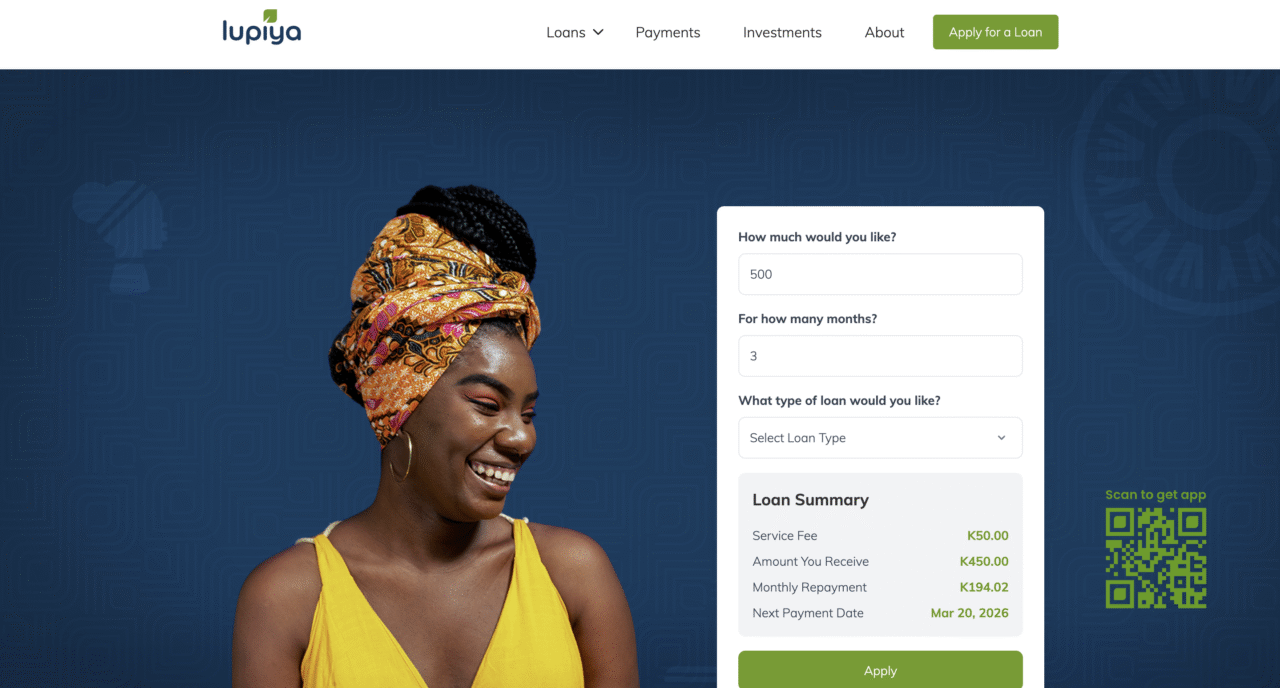

In Zambia, the digital banking sector reached a new milestone with Lupiya, a prominent neobank, successfully closing an $11.25 million Series A funding round. This capital raise, which was nearly two years in development, represents a vote of confidence in the Southern African nation’s burgeoning tech ecosystem. The investment was led by Alitheia IDF Fund, managed by IDF Capital, with significant participation from international development finance institutions including the German-based KfW DEG and INOKS Capital. This influx of capital is earmarked for several strategic objectives, primarily the enhancement of Lupiya’s proprietary technological infrastructure and the expansion of its product suite to better serve the unique needs of the Zambian market and beyond.

Founded in 2016 by Evelyn Chilomo Kaingu and Muchu Kaingu, Lupiya has positioned itself as a critical link between traditional capital and the underbanked. The company’s core offering, Lupiya Pay, provides credit products and digital payment services designed to be accessible via mobile devices. By partnering with Mastercard, Lupiya has gained access to global payment rails, allowing it to facilitate digital transactions that were previously impossible for many of its users. This partnership is a cornerstone of the company’s growth strategy, aligning with Mastercard’s broader goal of integrating millions of individuals into the digital economy. Beyond the Series A, Lupiya is also pursuing an additional funding round this year specifically dedicated to scaling its lending business and enhancing its embedded finance offerings as it prepares to enter neighboring markets in the Southern African Development Community (SADC) and East Africa.

The necessity for such services is underscored by data from the World Bank and the Bank of Zambia. While Zambia’s overall financial inclusion rate improved from 59.3% in 2015 to 69.4% in 2020, the progress remains uneven. In the Lusaka Province, which encompasses the capital city, the inclusion rate exceeds 87%. However, in rural provinces, this figure often hovers around 40%. Lupiya’s focus on peer-to-peer (P2P) lending—becoming one of the first companies to receive approval from the Zambian Securities and Exchange Commission for such services—is a direct attempt to address this disparity. By offering collateral-backed loans, salary advances, and specialized "agriloans" for the farming sector, the platform provides a financial lifeline to those without traditional credit histories.

Further north, Ethiopia is witnessing a fundamental shift in its national monetary policy and infrastructure. The National Bank of Ethiopia, in collaboration with the national switch EthSwitch, has officially launched the National Instant Payment System (NIPS), branded as EthioPay-IPS. This system, powered by the SmartVista platform from the Swiss-based technology firm BPC, represents a massive leap forward for the Horn of Africa’s largest economy. The system currently connects 32 commercial banks, 12 microfinance institutions (MFIs), three payment system operators (PSOs), and three payment instrument issuers (PIIs), creating a unified ecosystem for real-time financial transactions.

The implementation of EthioPay-IPS allows for centralized automated reconciliation and the introduction of modern payment rails that are both faster and more cost-effective than previous methods. The system supports account-to-account and wallet-to-wallet transfers, interoperable QR code payments, and "request-to-pay" functionalities. One of the most significant features for the general public is the alias-based payment system, which allows users to transfer funds using a simple identifier, such as a phone number, rather than cumbersome bank account details. This move is part of the "Digital Ethiopia 2025" strategy, which seeks to modernize the country’s economy through digital transformation.

EthSwitch was established in 2011 with the mandate to modernize the national payment system. Owned by a consortium of public and private banks alongside the National Bank of Ethiopia, the organization has been the driving force behind the interoperability of ATMs and Point-of-Sale (POS) terminals since 2016. Abeneazer Wondwossen, Chief Portfolio Officer at EthSwitch, noted that the goal of the new instant payment system is to provide a simple, affordable, and secure infrastructure that is "locally governed yet future-ready." The involvement of BPC, which serves over 500 customers in 140 countries, ensures that Ethiopia’s new system meets international standards for fraud management and financial inclusion.

In Rwanda, the focus has shifted toward the formalization and empowerment of the SME sector. Kayko, a Kigali-based fintech founded in 2021 by brothers Crepin and Kevin Kayisire, recently announced a $1.2 million seed funding round. The investment included participation from Burrow Capital, the Luxembourg Development Agency, and Hanga Ignite. This funding coincided with a major regulatory achievement: the acquisition of an Electronic Money Issuer (EMI) license from the National Bank of Rwanda (NBR). This license is a transformative step for Kayko, allowing it to transition from a software provider to a regulated financial entity capable of managing merchant wallets and processing regulated payments.

Kayko currently serves more than 8,500 Rwandan SMEs, providing tools for bookkeeping, inventory management, and tax compliance. In many emerging markets, small businesses struggle to secure credit because they lack formal financial records. Kayko’s platform addresses this "information asymmetry" by converting everyday business activities—such as sales and expense tracking—into structured financial data. This data can then be used to generate credit scores, enabling banks and other lenders to assess the risk of lending to micro-enterprises with greater accuracy. The new capital will be used to further develop these data capabilities and expand the company’s lending tools.

The broader implications of these developments across Zambia, Ethiopia, and Rwanda are significant for the African continent’s economic trajectory. For decades, the primary hurdle to economic growth in these regions was the "unbanked" status of the majority of the population. However, the current trend suggests a shift from basic mobile money transfers toward sophisticated "Mobile Money 2.0" ecosystems. These ecosystems include complex credit products, insurance, and investment opportunities delivered via smartphone apps and USSD codes.

In Zambia, the expansion of Lupiya signifies the maturing of the Southern African fintech market, which has often been overshadowed by the tech hubs in Nigeria, Kenya, and South Africa. The focus on "agriloans" is particularly vital, as agriculture remains a primary employer in Zambia. By providing farmers with the capital needed for seeds and equipment through digital channels, fintech is directly contributing to food security and rural poverty reduction.

In Ethiopia, the launch of an instant payment system is a prerequisite for the entry of more international players into the market. As the country continues to liberalize its telecommunications and banking sectors—evidenced by the entry of Safaricom Ethiopia—the existence of a robust, interoperable payment switch like EthSwitch becomes the backbone upon which all other digital services will be built. It reduces the "friction" of doing business, allowing for the rapid movement of capital that is essential for a modern economy.

Rwanda’s Kayko illustrates the importance of the "SME engine" in African development. By providing the digital tools necessary for formalization, Kayko is helping to move thousands of businesses from the informal shadow economy into the regulated financial system. This not only helps the businesses grow but also increases the national tax base and provides the government with better data for economic planning.

As these three nations continue to innovate, the regulatory environment will remain a critical factor. The proactive stance of the National Bank of Rwanda in issuing EMI licenses and the National Bank of Ethiopia’s involvement in EthSwitch suggest a growing alignment between regulators and innovators. This "regulatory sandboxing" and cooperative approach are likely to attract further foreign direct investment (FDI) into the region’s tech sector.

In conclusion, the recent activities of Lupiya, EthSwitch, and Kayko represent more than just isolated business successes; they are indicators of a regional pivot toward a fully integrated digital economy. By addressing the specific needs of their respective markets—whether it is rural credit in Zambia, national interoperability in Ethiopia, or SME bookkeeping in Rwanda—these organizations are building the infrastructure that will define African commerce for the next decade. The successful deployment of over $12 million in new capital across these ventures, combined with the launch of nationwide payment rails, sets a high bar for fintech innovation in 2026 and beyond. As these technologies scale, the focus will likely shift toward cross-border interoperability, potentially paving the way for a more unified and digitally-driven African Continental Free Trade Area (AfCFTA).