Brian and Michael, both 34-year-old residents of central Connecticut, represent a significant demographic of American professionals who, despite earning a combined household income well above the national median, find themselves navigating the complexities of consumer debt and the barriers to homeownership. Brian, a quality assurance manager for a state-run hospital, and Michael, a project coordinator for a state behavioral health agency and a disability advocacy coordinator, have been partnered since 2013. While the couple has achieved career stability and possesses robust retirement vehicles through state employment, their current financial profile is characterized by approximately $28,259 in consumer debt and a recent doubling of housing expenses. This case study explores the strategic adjustments required to transition from a cycle of debt to a trajectory of long-term wealth accumulation and real estate acquisition.

The Evolution of Financial Challenges: A Chronological Overview

The financial trajectory of Brian and Michael over the past decade reflects a period of significant achievement followed by recent environmental and situational stressors. Since the inception of their relationship in 2013, the couple focused on career development within the public and non-profit sectors. A major milestone was reached several years ago when Brian successfully liquidated $58,000 in student loan debt, a move that theoretically cleared the path for aggressive savings.

However, the period between August 2022 and late 2023 introduced a series of "financial shocks" that disrupted their progress. The couple had previously resided in a 600-square-foot studio apartment with a monthly rent of $945, allowing for a high degree of capital preservation. The termination of this living arrangement forced them into the 2023 rental market, which has seen unprecedented price inflation across the Northeastern United States. They eventually secured a two-bedroom, two-bathroom apartment in a refurbished industrial mill at a cost of $2,000 per month—a 111% increase in housing expenditure.

Concurrent with the move, the couple faced unplanned veterinary expenses for two new kittens and the costs associated with uprooting an eight-year residency. These factors, combined with Brian’s transition from the private non-profit sector to a state-run hospital, created a period of financial volatility. While the move to state employment provided superior benefits, including a pension and lifetime healthcare, the immediate liquidity crunch resulted in the accumulation of over $28,000 in high-interest-potential credit card debt.

An Anatomy of Household Finances: Income and Expenditure

A detailed analysis of the couple’s balance sheet reveals a robust earning capacity. Their combined annual gross income is approximately $167,544. After accounting for taxes, healthcare premiums, and pre-tax retirement contributions, their annual net (take-home) income stands at $109,455.42.

Annual Net Income Breakdown:

- Brian’s Primary Income: $60,953.36 (Net)

- Michael’s Primary Income: $27,716 (Net)

- Michael’s Secondary Advocacy Role: $18,293.86 (Net)

- Variable/Consulting Income: $2,500 (Net)

- Total Annual Net: $109,455.42

Despite this six-figure net income, the couple’s reported annual spending is $96,414.36, leaving a theoretical surplus of $13,041.06 per year. However, the couple reports feeling "behind" their peers, a sentiment exacerbated by the lack of liquid savings. Their current cash reserves total approximately $9,000, which represents roughly one month of expenses—a level significantly below the recommended three-to-six-month emergency fund buffer.

The couple’s expense profile is dominated by rent ($24,000/year), debt servicing ($24,000/year at current rates), and transportation costs. Brian’s vehicle maintenance and commuting costs have averaged $1,064 per month over the last year due to the age of their vehicles—a 2007 Mercedes C280 and a 2007 Subaru Outback, both with 175,000 miles.

The Consumer Debt Catalyst and Interest Rate Pressures

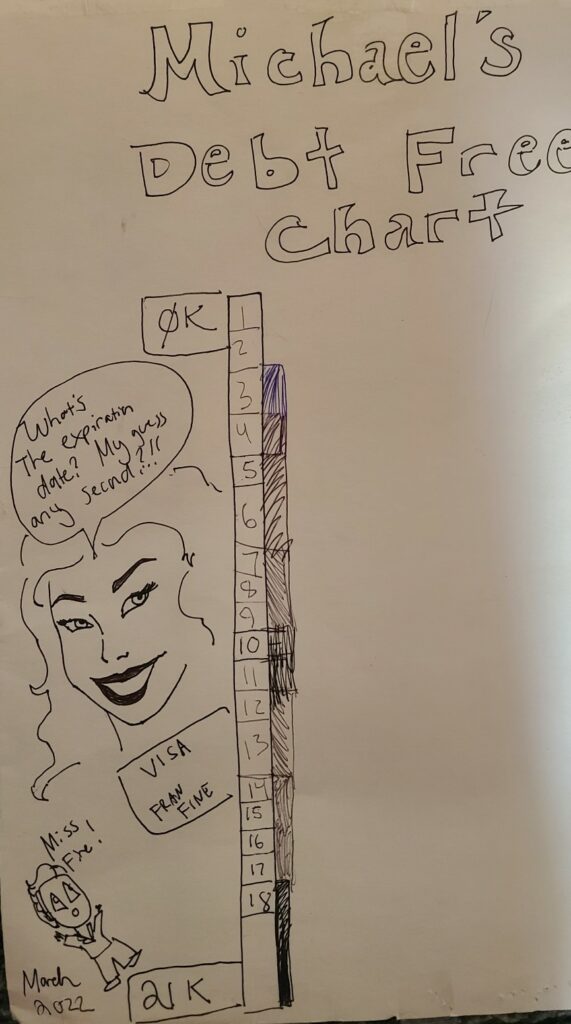

The most pressing threat to the couple’s financial health is the structure of their $28,259 consumer debt. A significant portion of this debt is currently held in 0% or low-interest introductory windows that are set to expire in November 2023.

Debt Portfolio:

- Visa (SCU): $16,057 at 0% (Rising to 17.99% in November 2023)

- Visa Platinum (NFCU): $9,700 at 10.99%

- Visa Platinum (Navy Federal): $2,503 at 0.99% (Rising to 17.74% in November 2023)

Financial analysts note that if these balances are not significantly reduced before the expiration of the introductory rates, the annual interest charges alone could exceed $4,500. The couple’s current strategy involves Michael paying $1,400 per month toward his balance, while Brian focuses on "snowballing" the smaller $2,503 balance. However, without a reduction in discretionary spending, the $16,057 balance remains a substantial "interest rate bomb" that could derail their homeownership goals for several years.

Asset Analysis and the "Triple Crown" of Retirement

In contrast to their liquid savings deficit, the couple’s retirement outlook is exceptionally strong for their age group, largely due to their employment within state agencies. Brian’s benefits package includes a 403(b), a 457(b) deferred compensation plan, and a state pension. This combination, often referred to as the "triple crown" of retirement, provides multiple layers of post-career security.

Current Asset Holdings:

- Michael’s 401(k): $36,992 (Vanguard Target Retirement 2055)

- Brian’s Rollover 401(k): $19,305

- Brian’s Pension Fund (Vested Value): $8,953

- Brian’s 457(b) and 403(b): $9,275

- HSAs and IRAs: $6,518

- Liquid Savings: $9,000

- Total Invested Assets: $91,250

Brian’s projected pension, estimated at $4,150 per month starting in 2054, represents a significant "fixed" asset that reduces the total amount they need to save in traditional brokerage accounts. Furthermore, the 457(b) plan offers a unique advantage: unlike 401(k) or 403(b) plans, funds in a 457(b) can be withdrawn penalty-free upon separation from service, regardless of age, providing a potential bridge for early retirement.

Strategic Recommendations for Debt Liquidation and Wealth Building

To achieve their goal of becoming "permanently debt-free" and purchasing a home, financial experts recommend a multi-phase intervention. The primary focus must be on maximizing the $13,041 annual surplus and identifying further "leakage" in discretionary spending.

Phase I: The Spending Detox

An analysis of the couple’s expenses identifies approximately $1,370 per month in discretionary spending that can be temporarily suspended to accelerate debt repayment. This includes:

- Dining Out: $200

- Gifts and Home Goods: $460

- Personal Care and Subscriptions: $220

- Non-Essential Travel/Hobbies: $490

By redirecting these funds toward their debt, the couple could increase their monthly debt payments to over $4,400. At this rate, the entire $28,259 balance could be eliminated in approximately 6.5 months, largely avoiding the high-interest triggers scheduled for November.

Phase II: The Emergency Buffer

Once the consumer debt is retired, the $4,400 monthly "debt payment" should be redirected into a High-Yield Savings Account (HYSA). Within four months, the couple would have an emergency fund of nearly $27,000, providing a robust shield against future "lifestyle shocks" like car repairs or medical bills.

Phase III: Homeownership Readiness

Only after debt liquidation and the establishment of an emergency fund should the couple begin aggressive saving for a down payment. In the current Connecticut real estate market, where the median home price has risen significantly, a 20% down payment on a $400,000 property would require $80,000. With their debt cleared, the couple could feasibly save this amount within 18 to 24 months.

Broader Economic Context: The Millennial Financial Landscape

The situation faced by Brian and Michael is emblematic of the "Millennial Middle Class Trap." Despite high earnings, this cohort often struggles with the "all-at-once" nature of mid-30s financial demands: retiring student loans, escalating housing costs, and the need to catch up on retirement savings.

In Connecticut, the economic climate adds specific pressures. The state has some of the highest electricity rates in the continental United States, and property taxes in many municipalities are significant. Furthermore, the 2023 housing market is characterized by low inventory and high mortgage rates, making the "buy low" strategy Brian desires difficult to execute in the near term. Experts suggest that for couples in this position, the most effective "investment" is often the guaranteed return of paying off double-digit interest rate debt, which outperforms almost any traditional market investment.

Future Outlook and Implications

The long-term outlook for Brian and Michael is positive, provided they transition from a reactive to a proactive financial stance. Their access to state-sponsored retirement plans and Michael’s secondary income streams provide a high ceiling for wealth accumulation.

The couple’s concerns regarding Social Security and political volatility are common, but Brian’s pension and their diverse array of tax-advantaged accounts (401k, 403b, 457b, HSA) offer a level of redundancy that most Americans lack. If they can successfully implement a rigorous expense-tracking system and eliminate the cycle of consumer debt, they are well-positioned to achieve homeownership and business ventures within the next three to five years. The key to their "next level of adulting" lies not in earning more, but in aligning their high earning capacity with disciplined capital allocation.