The implementation of financial literacy programs within the domestic sphere has gained significant traction as parents seek to insulate their children from the pressures of modern consumerism. In a recent pedagogical exercise conducted during the annual county fair in Vermont, a specific framework for early childhood money management was observed, focusing on children aged five and seven. This methodology, often referred to as a "family money philosophy," bifurcates household expenditures into essential needs and discretionary wants, effectively creating a micro-economy where children must earn, save, and manage their own capital. By utilizing high-stimulus environments like county fairs and museum gift shops as real-world laboratories, proponents of this model aim to demystify the abstract nature of currency and instill a labor-to-value correlation before children reach adolescence.

The Structural Framework of the Family Money Philosophy

The core of this financial education model rests on a clearly defined division of fiscal responsibility. Under this system, parents assume the role of the primary economic providers, covering all "essential" costs. This includes traditional necessities such as shelter, healthcare, and nutrition, but extends to educational and developmental "needs" like clothing, books, and admission fees to cultural institutions. By removing the burden of survival costs from the child, the framework allows the minor to focus entirely on discretionary spending, which serves as the primary vehicle for financial instruction.

Discretionary items are categorized into three main sectors: supplemental food (such as desserts at restaurants), souvenirs (trinkets from fairs or museums), and luxury educational materials (such as items from the Scholastic Book Fair). This categorization forces the child to prioritize their desires against a finite pool of resources. For instance, while a parent provides a home library through second-hand acquisitions and public library visits, the child is responsible for any "new" acquisitions from commercial book fairs. This distinction teaches the child that while information is a necessity, the format and "newness" of the medium are luxuries subject to market forces.

The Domestic Labor Market: Chores and Compensation

To facilitate this micro-economy, a performance-based compensation system is established. Unlike a flat allowance, which many financial experts argue can decouple the link between effort and reward, this model utilizes a "fair market value" chore system. Children are offered the opportunity to perform tasks that go beyond the baseline expectations of family membership.

The labor market is divided into "unpaid daily work" and "paid contractual labor." Unpaid tasks are defined as those that contribute to the child’s own well-being or the basic maintenance of the household, such as cleaning one’s room, making beds, clearing the table, and basic animal husbandry like collecting eggs. Paid tasks, conversely, are those that provide a service to the parents or the broader household infrastructure. These include:

- Organizing communal spaces (kitchen cabinets or drawers).

- Cleaning high-traffic areas (porches or entryways).

- Seasonal maintenance (clearing brush, stacking wood, or weeding gardens).

- Administrative assistance (shredding documents or filing).

Compensation is strictly contingent upon the quality of the work. If a task is completed poorly—such as spilling refuse while emptying trash cans—the "contractor" must rectify the error before payment is rendered. This instills a sense of professional accountability and emphasizes that in a market economy, value is derived from the successful completion of a service, not merely the time spent attempting it.

Chronology of Financial Milestones and the Debt Lesson

The efficacy of this hands-on approach is best illustrated through a series of chronological events that forced the children to interact with complex economic concepts such as debt, joint ventures, and asset security.

In the summer of the previous year, the elder child (then age six) encountered the "Unicorn Debt Crisis" at a local fair. Desiring an inflatable toy priced at $13 while only possessing $9, the child was permitted to enter into a credit agreement with the parents. The parents provided the $4 shortfall on the condition that it would be repaid through mandatory labor. The subsequent realization—that performing chores to pay for a previously consumed item yielded no new capital—provided a visceral lesson in the "negative utility" of debt. The child noted that working without receiving a physical payout felt unrewarding, a sentiment that led to a year-long avoidance of credit-based purchases.

The following year, the focus shifted to asset security and responsibility. During a visit to a science museum, the child misplaced her wallet containing her accumulated earnings. The resulting emotional distress and the subsequent recovery of the wallet through the museum’s lost-and-found served as a practical lesson in the physical risks associated with capital. The parents utilized this moment to explain that in the adult world, lost cash is rarely recovered, emphasizing the importance of organizational systems and vigilance.

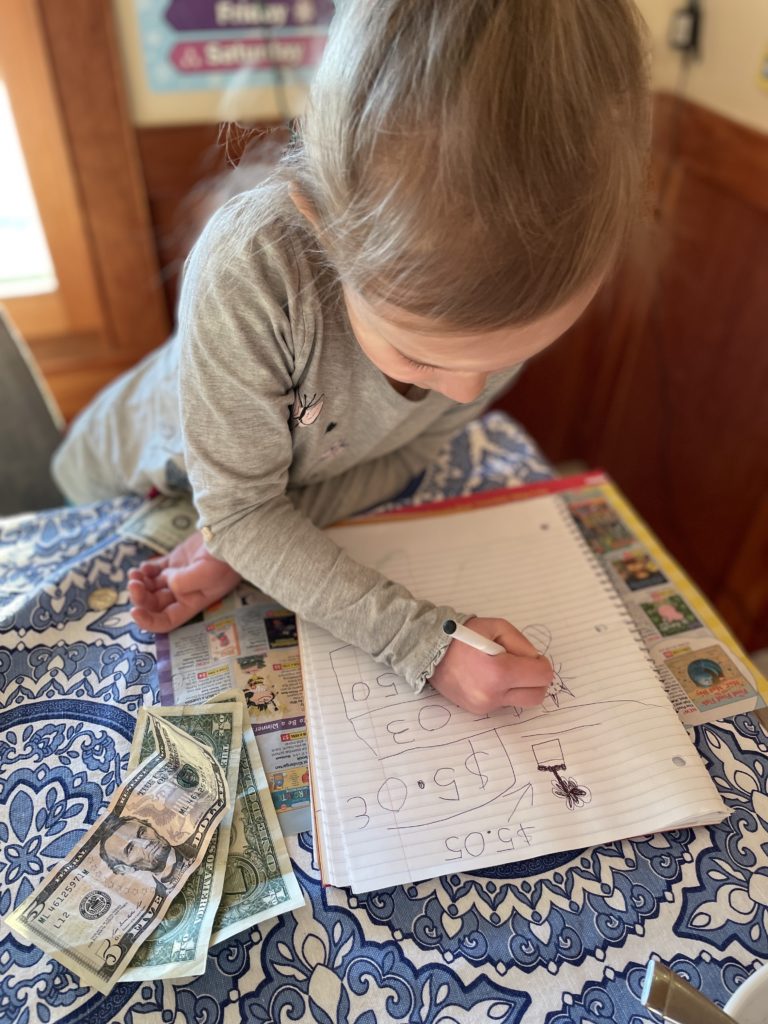

Most recently, the children demonstrated an understanding of "joint ventures" and "cost-sharing." When faced with a $7 dessert at a local farm, the siblings negotiated a deal to split the cost. This led to a secondary lesson in denominations and mathematics, as the odd-numbered price required them to calculate how to divide the cost using coins of various values. By ordering and paying for the item themselves, the children navigated the entire transaction cycle: earning, saving, planning, and executing a purchase.

Supporting Data and Psychological Context

The implementation of financial literacy at ages five and seven is supported by significant developmental research. A landmark study from the University of Cambridge found that many of the habits that will help or hinder a child’s financial future are formed by age seven. According to the researchers, by this age, most children can grasp basic economic concepts such as the exchange of money for goods and the understanding that some choices are irreversible.

Furthermore, data from the "T. Rowe Price Parents, Kids & Money Survey" indicates that nearly half of all parents miss opportunities to talk to their children about financial matters, often due to a belief that the topic is too complex or may cause anxiety. However, financial educators argue that "scaffolding"—the process of teaching simple concepts before moving to abstract ones—is essential. By explaining that a parent’s job is a source of income that pays for the family’s groceries, the mystery of the "ATM" or the "credit card" is replaced by a concrete understanding of labor-based sustainability.

Broader Impact and Long-Term Implications

The "Frugalwoods" model, as observed in this Vermont case study, serves as a microcosm for broader economic education. By treating money as a "tool" rather than a measure of self-worth or emotional wellness, the framework prepares children for the complexities of adult financial systems.

Experts suggest that children who participate in such systems are less likely to fall victim to "kid-directed consumerism"—a marketing strategy that targets minors to exert "pester power" over parental spending. When a child is responsible for their own discretionary funds, they become more critical consumers, often choosing to forgo low-quality trinkets in favor of saving for higher-value items.

The next phase of this specific educational journey involves the introduction of interest rates and long-term savings accounts. By establishing a "Parental Bank" that pays interest on saved chore earnings, the parents intend to teach the concept of "passive income" and the "time value of money." This transition from a "spending-and-earning" economy to a "savings-and-investment" economy represents the final stage of early childhood financial scaffolding.

Conclusion

The Vermont county fair exercise demonstrates that financial literacy is not merely a classroom subject but a series of lived experiences. By allowing children to fail—whether through losing a wallet or feeling the weight of debt—parents provide a safe environment for high-stakes lessons. As the children move toward more complex financial instruments like savings accounts and interest-bearing deposits, the foundation of labor, responsibility, and critical thinking established in these early years will likely serve as a buffer against the financial volatility of adulthood. In an era of digital transactions and invisible currency, returning to the basics of physical coins, negotiated chores, and the "Unicorn Debt" may be the most effective way to raise fiscally responsible citizens.