The global financial landscape has undergone a dramatic transformation, as interest rates, long anchored near historic lows, have surged to levels not seen in over two decades. This abrupt shift, orchestrated primarily by the Federal Reserve and other major central banks, marks the end of an extended era of inexpensive capital and is sending ripples through housing markets, investment strategies, and corporate balance sheets worldwide. The move is a direct response to persistent, elevated inflation, forcing policymakers to recalibrate their approach to economic management.

The End of Easy Money: A Policy Reversal

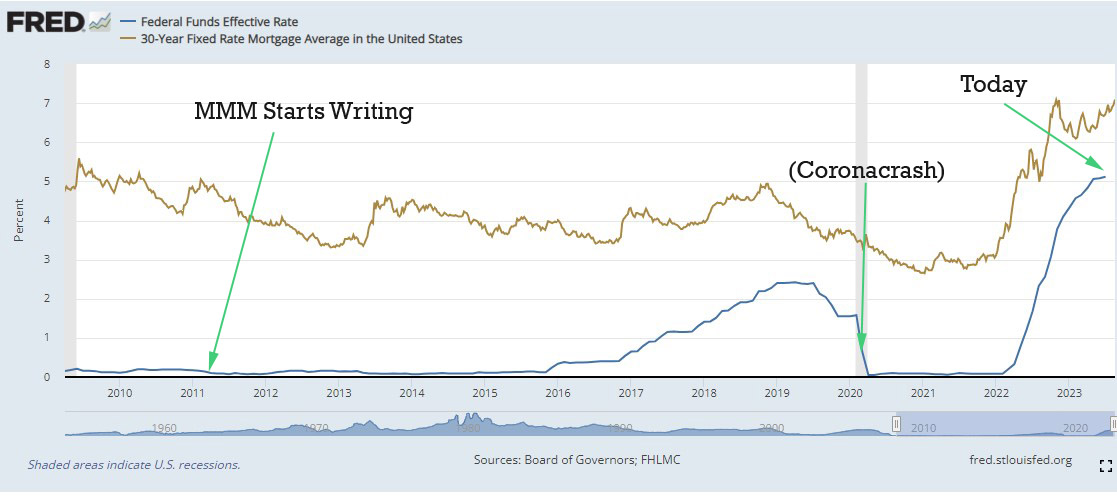

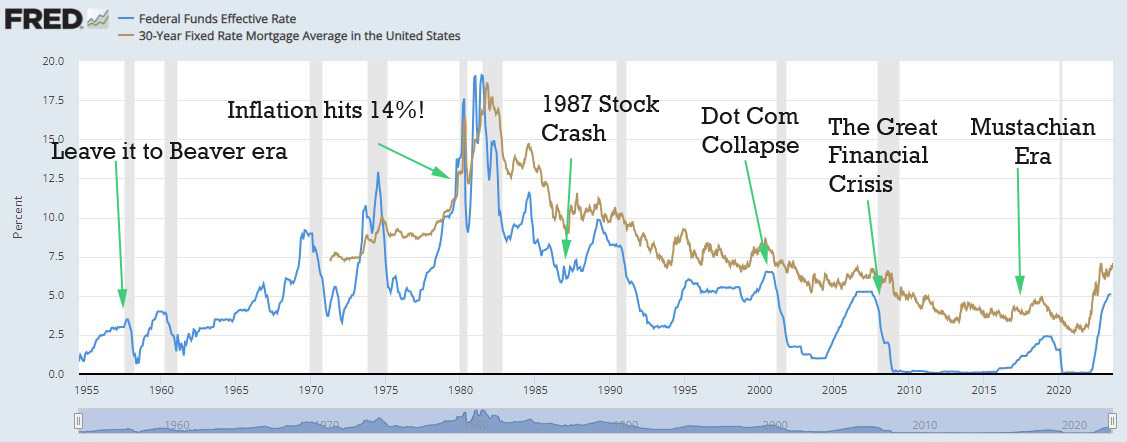

For nearly fourteen years, following the 2008 global financial crisis, the financial world operated under a paradigm of exceptionally low interest rates, often hovering close to zero. This period, characterized by quantitative easing and a deliberate strategy to stimulate economic recovery and growth, made borrowing remarkably cheap for consumers and corporations alike. Mortgages were more affordable, fueling a robust housing market, and businesses found it easy to secure capital for expansion, innovation, and hiring. This sustained period contributed to significant economic prosperity, technological advancement, and a prolonged bull market in equities.

However, the unprecedented monetary stimulus, combined with supply chain disruptions exacerbated by the COVID-19 pandemic and surging consumer demand, eventually led to an unwelcome consequence: inflation. By late 2021 and early 2022, inflation rates in many developed economies, particularly the United States, had reached multi-decade highs, eroding purchasing power and creating economic instability. The U.S. Consumer Price Index (CPI) peaked at 9.1% year-over-year in June 2022, a level not witnessed since the early 1980s.

Recognizing the urgent need to restore price stability, the Federal Reserve, under the leadership of Chairman Jerome Powell, initiated a series of aggressive interest rate hikes beginning in March 2022. The federal funds rate, which had been near zero since early 2020, was steadily increased, often by 75 basis points at consecutive meetings, reaching a target range of 5.25% to 5.50% by mid-2023. This rapid tightening cycle aimed to cool down an overheated economy by making borrowing more expensive, thereby reducing demand and bringing inflation back towards the Fed’s 2% target.

Economic Ramifications: From Housing to Hiring

The shift from an accommodative monetary policy to a restrictive one has had profound and varied impacts across the economy:

-

Housing Market Dynamics: Perhaps the most immediate and visible impact has been on the housing sector. The average 30-year fixed-rate mortgage, which stood around 3% at the beginning of 2022, quickly surged past 7%, reaching levels last seen in 2001. This dramatically increased the cost of homeownership. For a median-priced home, a buyer with a 10% down payment could see their monthly mortgage payment jump from approximately $1,265 to over $2,000, excluding taxes and insurance. This surge in financing costs has led to a significant slowdown in home sales, reduced affordability, and a "lock-in" effect where homeowners with ultra-low existing mortgage rates are reluctant to sell and buy a new home at much higher rates. The National Association of Realtors (NAR) reported a substantial decline in existing home sales, with the median home price seeing its first year-over-year declines in over a decade in early 2023, though prices have shown some resilience in subsequent months due to tight inventory.

-

Business Investment and Employment: Higher interest rates translate to increased borrowing costs for businesses, deterring new investments, expansions, and hiring. Venture capital funding, which thrived in the low-rate environment, has seen a notable decline, impacting startups and growth-stage companies. Major tech companies, including Meta (Facebook’s parent), Amazon, and Microsoft, announced tens of thousands of layoffs in 2022 and 2023, citing slowing growth and the need for cost efficiencies in a tighter economic climate. However, despite these high-profile cuts, the broader labor market has remained surprisingly robust, with the U.S. unemployment rate hovering near 50-year lows, confounding some economists’ predictions of a significant economic downturn.

-

Consumer Spending and Debt: Consumers face higher interest rates on credit cards, auto loans, and other forms of financing, impacting their disposable income and purchasing power. While this is intended to curb inflation by reducing demand, it also puts pressure on household budgets. Data from the Federal Reserve indicates a rise in credit card debt and delinquencies, particularly among lower-income households.

-

Banking Sector Vulnerabilities: The rapid increase in interest rates also exposed vulnerabilities within the banking sector. Banks holding long-dated, low-yielding bonds saw the market value of those assets plummet as interest rates rose. This contributed to a "miniature banking crisis" in early 2023, with the collapse of Silicon Valley Bank (SVB), Signature Bank, and First Republic Bank. These institutions faced significant deposit outflows as customers sought higher yields elsewhere and concerns mounted over their asset portfolios. Federal regulators swiftly intervened to stabilize the system, preventing a wider contagion.

The Economic Narrative vs. Reality

Despite the significant adjustments and the emergence of challenges like banking sector stress and corporate layoffs, the overall economic picture remains complex and, in some aspects, surprisingly resilient. While media headlines often highlight the "hard economic times" and differing political interpretations of the economic trajectory, key indicators present a nuanced view. As noted, the unemployment rate has remained remarkably low, suggesting underlying strength in the labor market. Gross Domestic Product (GDP) growth has also shown resilience, particularly in the latter half of 2023, indicating that the economy is absorbing the rate hikes better than many initially feared.

This period is largely seen by many economists as a necessary "digestion" phase for an economy that had consumed too much cheap money. The intention of the rate hikes is to engineer a "soft landing" – bringing inflation down without triggering a severe recession. Whether this delicate balancing act will succeed remains a central question for policymakers and market observers.

Investment Strategies in a New Rate Environment

The shift in interest rates necessitates a re-evaluation of investment strategies, though core principles often remain steadfast.

-

Stock Market Performance: The stock market experienced a significant correction from its peak in early 2022, with major indices like the S&P 500 entering bear market territory. However, historical data consistently demonstrates that the stock market tends to appreciate over the long run, despite unpredictable short-term fluctuations. Attempts to "time the market" by moving in and out based on economic forecasts are notoriously difficult and often lead to missed gains. For long-term investors, periods of market downturns, when valuations are lower, can present opportunities for accumulating assets at more favorable prices.

-

Fixed Income and Cash: With interest rates on savings accounts, money market funds, and short-term U.S. Treasury bills rising to over 4% or even 5%, these instruments have become attractive alternatives for preserving capital and generating income, particularly compared to the near-zero rates of previous years. This presents a more competitive yield environment against equities, prompting some investors to rebalance portfolios towards less volatile assets. However, the potential for long-term capital appreciation in equities, especially after a market correction, often outweighs the fixed returns of cash or short-term bonds for investors with a long time horizon.

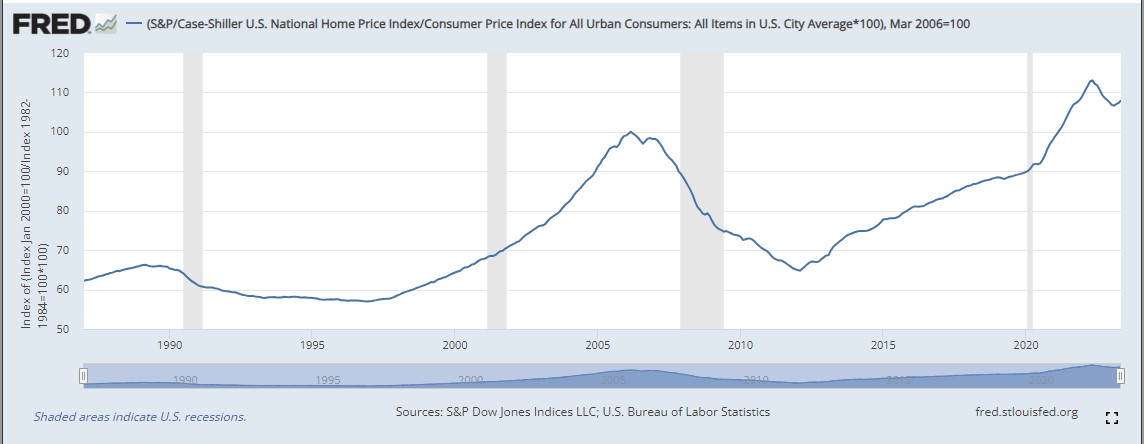

The Housing Market’s Future and the Question of Affordability

The trajectory of housing prices remains a critical concern. While higher mortgage rates have cooled demand, a persistent shortage of housing supply in many regions continues to exert upward pressure on prices. The "value" of a house is fundamentally determined by supply and demand dynamics, which are influenced by several factors:

- Population Growth and Household Formation: Continued demographic growth and the formation of new households sustain demand for housing.

- Construction Costs: The cost of labor, materials, and land impacts the feasibility and profitability of new construction. While some technological advancements may reduce component costs, overall construction expenses, including labor, have generally risen.

- Regulatory Environment: Local zoning laws, permitting processes, and other bureaucratic hurdles significantly impact the speed and volume of new housing development. Restrictive regulations, often driven by "Not In My Backyard" (NIMBY) sentiments, can severely limit supply, artificially inflating prices. Some cities are actively working to reform these regulations to encourage more diverse and affordable housing options.

Given the current economic environment, marked by high interest rates and tight supply, many analysts predict that house prices may either stabilize or see modest declines in some markets, rather than a widespread crash. A more probable scenario for broader affordability improvement might involve a period of flat prices that do not keep pace with inflation and wage growth, making homes relatively cheaper over time.

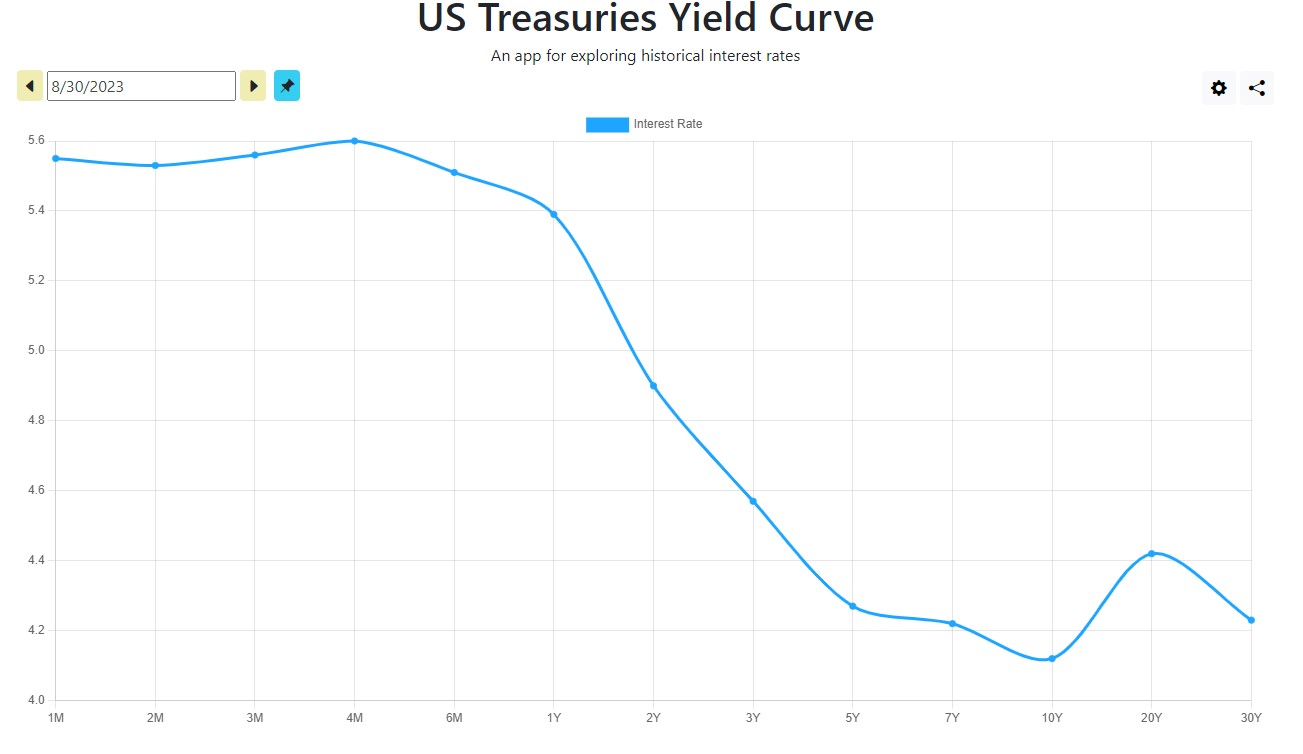

When Will Interest Rates Decline? The Inverted Yield Curve Signal

A key question for markets and consumers alike is when interest rates might begin to recede. Historically, the current "high" interest rates are actually closer to the long-term average when viewed over several decades, rather than just the post-2008 period.

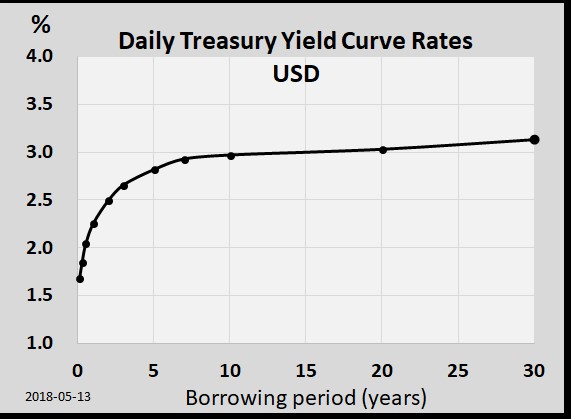

A significant indicator for future interest rate movements is the U.S. Treasury yield curve. Typically, long-term bonds offer higher yields than short-term ones, compensating lenders for locking up their money for longer periods. However, the current environment features an inverted yield curve, where short-term Treasury yields (e.g., 1-year) are higher than long-term yields (e.g., 10-year). As of late 2023, for instance, a 1-year Treasury might yield around 5.4%, while a 10-year Treasury yields closer to 4.05%.

This inverted yield curve is a historically reliable predictor of economic slowdowns or recessions. It implies that bond investors anticipate that the Federal Reserve will eventually cut interest rates in the future, likely in response to a cooling economy or an outright recession. This phenomenon has preceded 10 of the last 11 U.S. recessions over the past 75 years. While not a guaranteed forecast, it strongly suggests that market participants expect interest rates to begin declining, potentially within the next 18 to 24 months, possibly accompanied by some degree of economic contraction. Federal Reserve officials, through their "dot plot" projections, have also begun to signal potential rate cuts in the coming years, contingent on inflation returning sustainably to target levels.

Navigating the New Financial Normal

The current economic landscape, shaped by higher interest rates, represents a return to a more historically conventional monetary policy environment after an extended period of extraordinary accommodation. While the transition has brought adjustments and challenges across various sectors, it is also a testament to the dynamic nature of market forces and policy responses.

For individuals and businesses, the emphasis shifts towards financial resilience and strategic planning. Managing debt effectively, maintaining adequate savings, and making informed decisions about major investments like real estate become even more crucial. The focus remains on sustainable economic growth and price stability, with the Federal Reserve committed to navigating the economy through this period of recalibration. The eventual trajectory of interest rates and their broader economic impact will depend on the ongoing interplay of inflation, employment, and global economic conditions, all closely monitored by policymakers and market participants.