As the United States enters another pivotal election year, the national economic discourse has once again become a central battleground for political candidates. While citizens are encouraged to conduct thorough research and cast informed votes, a critical examination reveals that much of the economic rhetoric employed by competing parties often diverges significantly from verifiable data and established economic principles. This phenomenon, particularly pronounced in swing states where voter sentiment is highly sought, frequently prioritizes emotional appeals over sound economic analysis, obfuscating a clearer understanding of the nation’s financial health.

The Disconnect: Public Perception Versus Economic Reality

A striking characteristic of the current election cycle is the pronounced disparity between objective economic indicators and public sentiment regarding the economy. Despite claims from opposition parties of a "bad economy," data from various credible sources paints a robust picture. The U.S. economy has demonstrated remarkable strength, marked by historically low unemployment rates, sustained GDP growth, and significant wage increases. For instance, recent reports indicate unemployment hovering near five-decade lows, consistently below 4% for an extended period, a feat not seen in decades. The Gross Domestic Product (GDP) has shown consistent expansion, with Q3 2023 recording a robust annualized growth rate of 4.9%, reflecting a dynamic and productive economic environment.

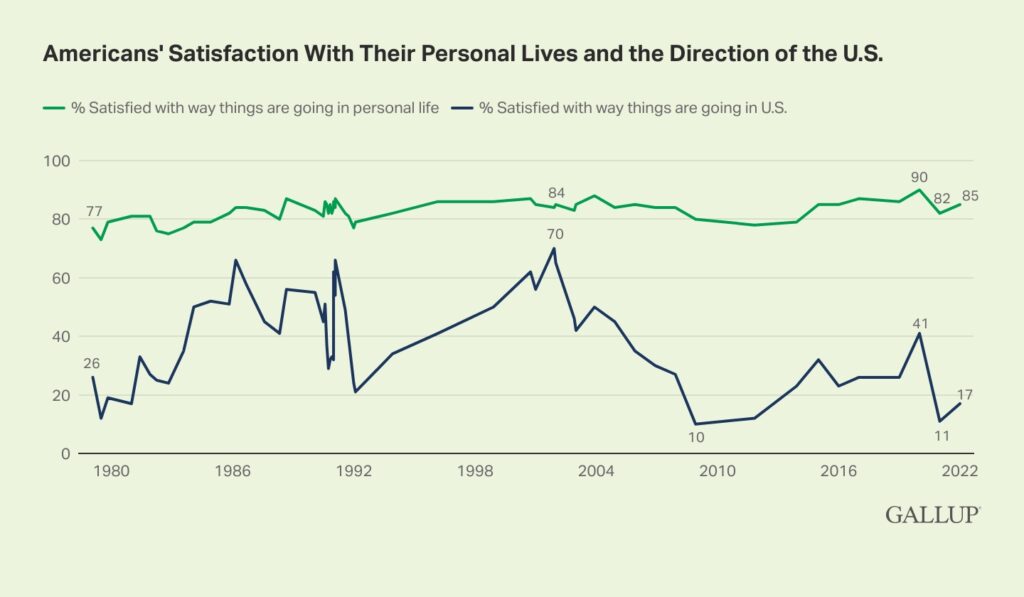

This period of economic vigor has, paradoxically, been accompanied by a public perception of struggle. A Gallup poll cited in recent analyses highlighted this divergence, revealing that while a significant majority of Americans (approximately 85%) reported personal financial stability, only a small fraction (around 17%) believed the national economy was performing well. This mathematical incongruity—where widespread individual prosperity coexists with collective pessimism—suggests that external factors, notably the proliferation of misinformation across social media platforms and politically charged narratives, heavily influence public opinion, overriding direct personal experience. The brief period of elevated inflation experienced post-COVID-19, often framed negatively by political challengers, was in fact a symptom of an overheated economy—strong demand meeting supply chain constraints—necessitating corrective measures such as interest rate adjustments by the Federal Reserve to stabilize prices. The annual inflation rate, as measured by the Consumer Price Index (CPI), has largely receded from its peak of over 9% in mid-2022 to approximately 2.4% recently, indicating a substantial return to price stability.

The Pervasive Misinformation: Six Economic Myths Debunked

The consistent misrepresentation of economic facts by political figures underscores a broader challenge to informed public discourse. Understanding the actual mechanics of the economy is paramount for citizens, as accurate knowledge empowers better financial decisions and fosters a more resilient society. To that end, a systematic debunking of common economic myths propagated during election campaigns is essential.

1. The President’s Limited Control Over the National Economy

A recurring theme in political campaigning is the attribution of economic booms or busts directly to the sitting president. When economic conditions are favorable, the incumbent administration often claims credit; during downturns, the opposition is quick to assign blame. However, this narrative oversimplifies the complex reality of the U.S. economy. The American economic system, characterized by its immense scale, diverse sectors, and fundamentally free-market orientation, is far too vast and intricate for any single individual, including the President, to exert direct, comprehensive control or short-term influence.

The U.S. economy, representing roughly 26% of global economic activity and powered by over 330 million people and countless businesses, operates within a larger international framework, making it susceptible to global trends, geopolitical events, technological advancements, and the economic performance of other nations. Economic cycles—periods of growth (often fueled by investor optimism and consumer confidence) followed by contractions (triggered by factors like asset bubbles, external shocks, or shifts in sentiment)—are largely intrinsic to market dynamics. While governmental fiscal policies (taxation, spending) can certainly play a role in shaping economic conditions, their effects are often delayed, indirect, and subject to numerous unpredictable variables. Major policy changes can take months or even years to fully materialize and interact with other economic forces. This complexity makes a direct causal link between a president’s actions and immediate economic outcomes largely tenuous. The government, through its policies, acts more like a rudder on a colossal ship, attempting to guide its course amidst the powerful and often unpredictable waves and storms of the global economic ocean, rather than being the engine or the wind itself.

2. The Federal Reserve’s Independence: Beyond Presidential Influence on Interest Rates

Another prevalent misconception is the idea that the President directly controls interest rates. Political candidates frequently express sympathy for middle-class Americans burdened by higher borrowing costs for mortgages, car loans, and credit cards, often promising to "fight" to lower these rates. Some even suggest direct intervention in the Federal Reserve’s operations, advocating for greater presidential authority over this independent body. This stance fundamentally misunderstands the role and structure of the Federal Reserve (the Fed).

The Federal Reserve is the independent central bank of the United States, tasked by Congress with a dual mandate: achieving maximum employment and maintaining stable prices (controlling inflation). To fulfill these objectives, the Fed utilizes monetary policy tools, primarily adjusting the Federal Funds Rate. This benchmark rate directly influences other interest rates across the economy, including prime rates, savings rates, and indirectly, mortgage and auto loan rates. Granting a sitting president direct control over monetary policy would be fraught with peril, as history has shown in nations where political leaders have manipulated central banks for short-term gains, often leading to hyperinflation, currency devaluation, and a severe loss of investor confidence. The Fed’s independence is crucial to its ability to make data-driven decisions necessary for long-term economic stability, acting as an essential "gas and brake pedal" for the economy. When inflation rises above its target, the Fed raises rates to cool demand and temper price increases; when the economy slows and unemployment rises, it lowers rates to stimulate growth and investment. The recent increase in the Federal Funds Rate from near zero in early 2022 to over 5% by mid-2023, for example, was a deliberate and necessary measure by the Fed to combat the post-COVID inflation surge and bring price stability back to the market, a decision made independently of presidential directives.

3. Deconstructing the Inflation Narrative: Wages Outpacing Prices

The narrative that recent inflation has universally made life harder for Americans, coupled with promises from politicians to "magically reverse" it, is one of the most significant distortions of current economic realities. The period immediately following the COVID-19 pandemic did indeed see a rapid rise in inflation, peaking in mid-2022. This was driven by a confluence of factors: significant government stimulus spending boosting aggregate demand, global supply chain disruptions causing goods shortages, and shifts in labor patterns due to remote work and factory closures. However, these transient factors have largely dissipated, and inflation has since moderated significantly, returning to near the Federal Reserve’s target of 2%. As of recent reports, the Consumer Price Index (CPI) has shown a year-over-year increase of approximately 2.4%, indicating a substantial return to price stability.

Crucially, the political narrative often overlooks the accompanying wage growth. Data from the Bureau of Labor Statistics indicates that average nominal wages have risen faster than inflation over the past few years. For instance, from the end of 2019 to late 2024, overall consumer prices have increased by approximately 19%, while average wages for private sector employees have surged by about 21%. This means that, on average, American workers’ real purchasing power—their wages adjusted for inflation—has increased, not decreased, since the pre-inflationary period. While some individual households may have experienced different outcomes based on their specific income and spending patterns, the aggregate data demonstrates a net gain. Politically driven promises to "bring prices back down" also ignore fundamental economic principles; while controlling inflation is desirable, outright deflation (a sustained decrease in prices) can be detrimental, leading to reduced consumer spending, deferred investments, and economic stagnation. Furthermore, the argument that "greedy corporations" are solely responsible for price increases to hoard profits, often termed "greedflation," has been largely unsupported by empirical evidence. A detailed analysis by NPR, for example, examining the grocery sector, found no evidence that these companies achieved windfall profits during the recent inflationary period; rather, price increases largely reflected genuine increases in input costs (labor, raw materials, transportation) and market dynamics in a competitive environment.

4. Housing Affordability: Beyond Presidential Control and Misguided Policies

Housing affordability has emerged as a critical concern, with U.S. house prices and rents having risen significantly faster than general inflation and wages over the last decade. The national median home price has climbed substantially, creating barriers for many aspiring homeowners. This situation is compounded by rising interest rates, which have pushed average 30-year fixed mortgage rates from historically low levels below 3% to above 7% in recent years, making mortgage borrowing significantly more expensive. The political discourse surrounding housing often proposes solutions that, while seemingly sympathetic, risk exacerbating the problem. Candidates frequently suggest subsidies for first-time homebuyers or schemes to artificially reduce interest rates.

These proposals, however, primarily stimulate demand without addressing the fundamental root cause: a severe, chronic shortage of housing supply. When demand outstrips supply, prices inevitably rise. The current housing deficit is estimated to be in the millions of units. The actual levers for improving housing affordability lie largely at the local and state levels, focusing on increasing the housing stock. Effective solutions include:

- Streamlined Permitting: Expediting and simplifying the often-arduous bureaucratic process for construction permits, which can add significant time delays and cost to development projects.

- Modernized Building Codes: Revising outdated and overly expensive building codes that unnecessarily inflate construction costs without proportional safety benefits.

- Zoning Reform: Eliminating restrictive suburban-style zoning laws (e.g., single-family exclusive zoning, minimum lot sizes, excessive setback requirements, stringent car parking mandates) that limit density and prevent the development of diverse, more affordable housing types like duplexes, townhouses, and multi-family units.

- Reducing NIMBYism: Reforming laws that grant disproportionate power to Not In My Backyard (NIMBY) groups, enabling them to block necessary housing developments on privately owned land, even when such projects align with broader community needs.

Implementing such reforms could substantially reduce the cost of building new homes, making housing more accessible and affordable for a broader population, a goal that direct presidential intervention or demand-side subsidies cannot achieve without inflationary side effects.

5. The Obsolescence of Gasoline Price Debates

Few economic topics generate as much political theater as gasoline prices. Candidates frequently blame opponents for "high" gas prices or promise to lower them, despite the limited influence any U.S. president has over global energy markets. This focus is increasingly anachronistic for several reasons.

First, when adjusted for inflation, current gasoline prices, typically ranging from $3-4 per gallon, are comparable to what they were in the 1950s. The U.S. Energy Information Administration (EIA) data on inflation-adjusted gasoline prices confirms that current levels are within historical norms and not an unprecedented burden. This historical context reveals that today’s prices are not exceptionally high in real terms. Second, despite the perceived burden, the average American household dedicates a relatively small portion—approximately 2.5%—of their disposable income to gasoline. This figure is dwarfed by other costs associated with vehicle ownership, such as depreciation, insurance, and maintenance, which collectively represent a far greater financial outlay for most drivers. According to AAA, the average annual cost of owning a new car exceeds $12,000, with fuel being a fraction of that.

Third, and most critically, gasoline as a primary vehicle fuel is becoming increasingly obsolete. The rapid advancements and widespread availability of electric vehicles (EVs) have fundamentally altered the transportation landscape. Used EVs are now often more affordable than comparable used internal combustion engine (ICE) vehicles, and many new EV models are competitively priced, even offering significant cost savings over their gasoline counterparts when factoring in lower fuel and maintenance expenses. EVs offer a superior driving experience—quieter operation, faster acceleration, and significantly reduced maintenance needs due to fewer moving parts—while eliminating the need for gasoline altogether. The continued political fixation on gasoline prices, therefore, represents a failure to acknowledge and adapt to a fundamental technological and economic shift, akin to debating the price of outdated technologies like Kodak film or typewriters in a digital age.

6. Shifting Focus: Beyond Perpetual Economic Worry to Well-being

Perhaps the most profound misconception perpetuated by political discourse is the notion that constant worry about "the economy" is a necessary or productive endeavor for most citizens in a developed nation like the United States. While diligence, innovation, and economic progress are valuable, American society collectively surpassed the threshold of providing for basic needs and achieving widespread affluence many decades ago. The incessant political focus on incremental economic gains or perceived shortfalls often resembles affluent individuals at a lavish buffet lamenting the absence of "one more flavor of donuts," rather than addressing genuine scarcity.

This perspective is not to dismiss legitimate concerns such as income and wealth inequality. It is undeniable that the wealthy often accrue assets and income at a faster rate, contributing to societal disparities. According to the Federal Reserve, the wealthiest 10% of Americans hold over 70% of the nation’s wealth, a disparity that necessitates attention. A progressive tax system and thoughtful wealth redistribution policies are crucial for fostering a more equitable, peaceful, and ultimately happier society. However, empirical evidence, such as studies by economists like Daniel Kahneman and Angus Deaton, suggests that beyond a certain level of income (often cited around $75,000-$100,000 annually, adjusted for cost of living), additional wealth does not proportionally increase individual happiness or emotional well-being. This phenomenon highlights that "enough" is often more a function of mindset, personal resilience, and a robust collection of life skills than merely the size of one’s paycheck.

If political leaders genuinely sought to enhance the happiness and overall well-being of their constituents, their platforms might shift from pandering to specific interest groups or stoking economic anxieties. Instead, they would advocate for principles that foster financial literacy, encourage mindful consumption, promote community engagement, and emphasize the development of practical life skills—strategies that empower individuals to thrive within their "circle of control" regardless of external economic fluctuations. Such an approach would prioritize long-term societal health over short-term electoral gains.

The Imperative of Economic Literacy for an Informed Electorate

In conclusion, the current U.S. election cycle demonstrates a clear pattern of economic rhetoric that often distorts reality for political gain. From misrepresenting the President’s influence on the economy and interest rates, to mischaracterizing inflation’s impact and overlooking fundamental drivers of housing and energy costs, these narratives serve to manipulate voter sentiment rather