In the rural landscapes of Vermont, a burgeoning movement toward early childhood financial literacy is taking shape, exemplified by a structured pedagogical framework implemented by the founders of the Frugalwoods project. By utilizing high-traffic consumer environments, such as local county fairs and museum gift shops, as live-action classrooms, this methodology seeks to demystify the complexities of the modern economy for children as young as five and seven years old. This report examines the specific strategies employed to transition children from passive consumers to active financial agents, focusing on labor-based earning, discretionary spending boundaries, and the psychological impacts of debt.

The Foundational Framework: Needs Versus Wants

The core of the Vermont-based "Family Money Philosophy" rests on a clear demarcation between parental obligations and individual discretionary spending. In this model, the parents—identified as the primary economic providers—assume full responsibility for "needs." This category includes essential expenditures such as housing, healthcare, nutrition, clothing, and foundational education. Furthermore, the parents subsidize entry into cultural and educational venues, including museum admissions and county fair tickets.

The secondary tier of the framework involves "wants," which are categorized as discretionary items. Children are required to fund these purchases independently. Common examples identified in the Frugalwoods case study include:

- Supplemental Nutrition: While basic meals are provided, "luxury" items such as restaurant desserts must be purchased by the child.

- Souvenirs and Trinkets: While admission to a venue is paid for, any secondary consumer goods—such as toys from a gift shop or inflatable items from a fair—are the child’s financial responsibility.

- Non-Essential Media: Books are provided through libraries and used sales, but new items from commercial vendors like the Scholastic Book Fair require personal capital.

The Labor Market: Implementing a Chore-Based Economy

To facilitate this self-funded model, the household operates a micro-economy based on a "fair market value" chore system. This system is designed to teach children the direct correlation between labor and capital. Unlike "daily unpaid work"—which includes self-maintenance tasks like making beds or clearing one’s own table setting—paid chores are defined as tasks that provide a broader benefit to the family unit.

The current labor list includes seasonal and skill-appropriate tasks such as:

- Vacuuming and floor maintenance.

- Agricultural assistance, including weeding and garden preparation.

- Waste management, including emptying household bins.

- Organizational projects, such as kitchen cabinet restructuring.

A key component of this model is the negotiation process. Children are encouraged to propose "chore bundles" or negotiate lump-sum payments for larger projects. For instance, a recent agreement involved a $10 payment for a comprehensive reorganization of the kitchen’s storage spaces. However, the system maintains strict quality control standards. Payments are only disbursed upon completion of the task to a professional standard, reinforcing the concept that in a market economy, substandard work does not command full compensation.

Case Study: The Psychological Burden of Debt

Perhaps the most significant milestone in this educational timeline occurred during a previous county fair, involving the purchase of a $13 inflatable unicorn. When the eldest child, aged seven, found herself $4 short of the purchase price, the parents opted to act as a lending institution rather than a benefactor.

The child was allowed to enter into a debt agreement, receiving the item immediately in exchange for future labor. The subsequent "debt-servicing phase" provided a visceral lesson in the opportunity cost of credit. The child expressed frustration that she was "working for nothing," as the labor performed post-purchase did not result in new capital but merely satisfied a past obligation.

Economic analysts suggest that this early exposure to the "unfun" nature of debt is a critical deterrent against future high-interest consumer credit reliance. Since this incident, the children have reportedly avoided debt entirely, opting instead for a "save-first" approach.

Chronology of Financial Maturity

The development of financial literacy in the Frugalwoods household follows a distinct chronological progression:

- Ages 3–4 (Introduction): Recognition of physical currency and the basic concept that "Mama works for money to buy groceries."

- Ages 5–6 (The Earning Phase): Introduction of paid chores and the management of a physical wallet.

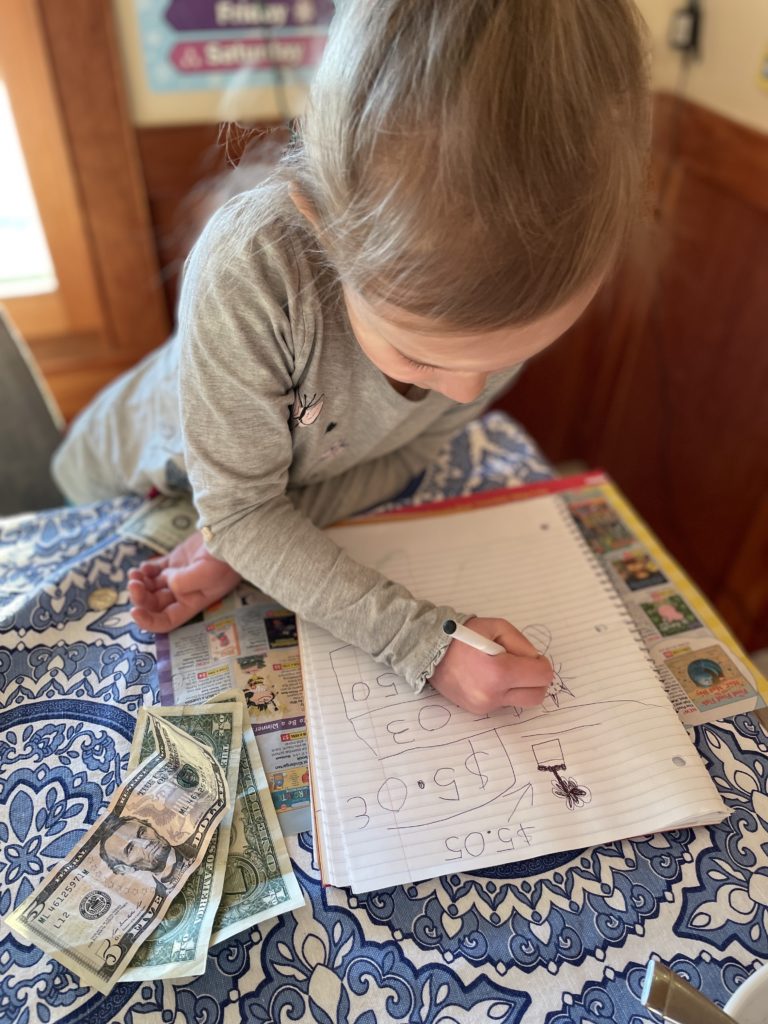

- Age 7 (Market Strategy): Introduction of comparison shopping and cost-sharing. A recent example involved the purchase of a $7 dessert at a local farm. The eldest child identified that the purchase benefited her younger sister and successfully negotiated a cost-splitting arrangement, which required the children to calculate non-even divisions of currency.

- Future Phase (Capital Growth): The parents intend to launch the "Bank of Parental Units," a system that will introduce the concept of interest rates on savings to encourage long-term capital retention over immediate consumption.

Supporting Data and Broader Impact

The Frugalwoods methodology aligns with broader national trends regarding early childhood education. According to the 2023 T. Rowe Price "Parents, Kids & Money Survey," nearly 40% of parents feel "very" or "extremely" concerned about their children’s future financial well-being, yet many struggle to find practical ways to teach these concepts.

Data from the Consumer Financial Protection Bureau (CFPB) suggests that children who begin learning about money between the ages of five and eight are significantly more likely to exhibit "pro-savings" behaviors in adulthood. By demystifying the "adult world" of money—viewing it as a tool rather than a source of anxiety or status—parents can foster a sense of agency in their children.

The "scaffolding" approach used in Vermont—starting with basic counting and moving toward debt management and interest—prevents the cognitive overload that often occurs when financial topics are introduced too late. It also removes the "taboo" nature of money, allowing children to ask questions and make mistakes in a controlled, low-stakes environment.

External Perspectives and Expert Analysis

Financial educators often emphasize that "real-world" consequences are the most effective teachers. Dr. Elena Rossi, a child psychologist specializing in developmental milestones, notes that "the transition from abstract numbers to the physical loss of a wallet or the physical labor required to pay off a loan creates neural pathways that abstract lessons cannot replicate."

In the Frugalwoods case, a "near-loss" incident at a science museum—where a child misplaced her wallet—served as a high-stakes lesson in asset protection. The emotional relief of recovering the wallet through an "official" channel (the lost and found) reinforced the importance of personal responsibility and the role of community institutions in financial security.

Implications for Future Financial Education

The success of these localized strategies suggests a potential shift in how American families approach consumerism. By treating the county fair or the grocery store as a laboratory for economic theory, parents are able to counter the "annoying instances of kid-directed consumerism" that are prevalent in modern marketing.

The broader implication is the creation of a generation of "conscious consumers." If a child understands that a $7 dessert represents an hour of weeding or vacuuming, they are less likely to fall prey to impulsive purchasing habits later in life. Furthermore, by involving children in the mechanics of payment—having them order, pay, and collect change independently—they develop the social and mathematical confidence required to navigate the global economy.

As the Frugalwoods children move toward the "savings account" phase of their education, the focus will shift from the mechanics of the transaction to the mechanics of wealth building. The introduction of interest rates via the "Bank of Parental Units" will mark the transition from labor-based income to capital-based growth, providing a comprehensive foundation for lifelong fiscal health.

This model serves as a scalable example for families seeking to integrate financial literacy into daily life, proving that even the most "boring" meetings or the most "annoying" consumer environments can be transformed into invaluable educational opportunities.