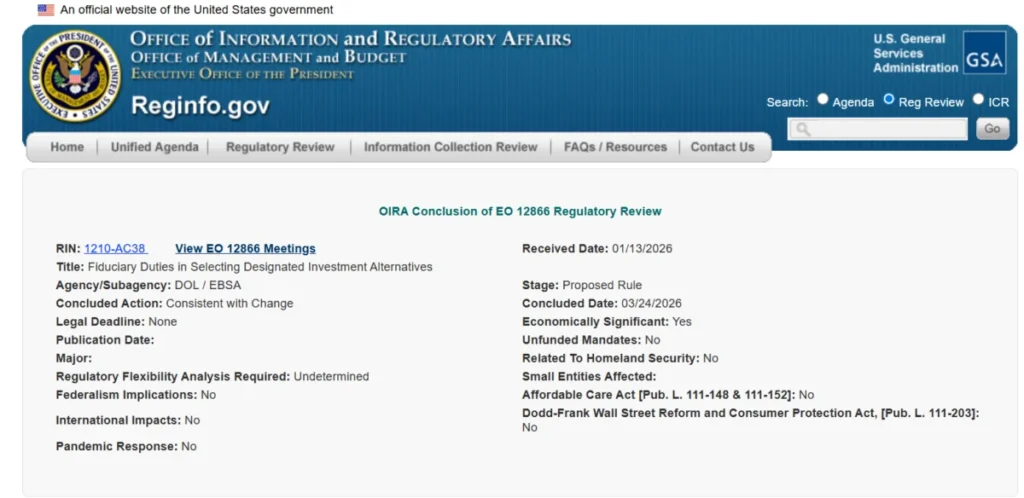

The Office of Information and Regulatory Affairs (OIRA), a division within the White House that oversees regulatory policy, has concluded its review of a significant proposal from the Department of Labor (DOL). This proposal has the potential to fundamentally alter how fiduciaries responsible for 401(k) plans assess and incorporate alternative assets, including exposure to digital assets. The conclusion of OIRA’s review, as indicated on its official website, occurred on March 24th. The action was categorized as "consistent with change" and the proposal itself was designated as "economically significant," signaling its potential for substantial impact on the financial landscape. The Department of Labor is now expected to formally publish the proposed rule, initiating a standard 60-day public comment period. This period is a crucial step in the regulatory process, typically followed by revisions based on feedback and the eventual issuance of a final rule.

The impetus for this DOL proposal can be traced back to an executive order issued by President Donald Trump on August 7, 2025. This directive mandated federal agencies to explore and facilitate expanded access to alternative assets within 401(k) plans. A key component of this order was the explicit encouragement of exploring exposure to digital assets through carefully selected investment vehicles. The executive order specifically directed the DOL to re-evaluate existing restrictions concerning alternative assets in defined-contribution retirement plans. This re-evaluation was not limited to digital assets but also encompassed other asset classes such as private equity and real estate. Furthermore, the order emphasized the importance of inter-agency collaboration, calling for coordinated efforts between the U.S. Treasury Department and the Securities and Exchange Commission (SEC) to support potential rule changes. The successful completion of OIRA’s review marks a critical interagency hurdle cleared, paving the way for a proposal that could significantly broaden the accessibility of alternative investments for millions of Americans participating in defined-contribution retirement plans across the United States.

A Shifting Regulatory Landscape for Crypto in Retirement Accounts

The recent developments signify a notable shift in the federal government’s stance on digital assets within the context of retirement savings. On May 28, 2025, the Department of Labor rescinded a 2022 compliance release. This earlier release had strongly cautioned plan fiduciaries, urging them to exercise "extreme caution" when considering the inclusion of cryptocurrencies in 401(k) plans. The withdrawal of this cautionary guidance is a clear signal of a broader reevaluation and a potential easing of restrictions, suggesting a more open approach to digital asset exposure in retirement planning.

This policy evolution occurs against the backdrop of a robust and expanding U.S. retirement market. As of September 30, 2025, the total financial assets held within the U.S. retirement market reached a record-breaking $48.1 trillion, according to a comprehensive report by the Investment Company Institute (ICI). This vast pool of capital represents a significant opportunity for asset managers and investment providers looking to introduce new investment options. The sheer scale of this market underscores the potential impact of any regulatory changes that permit or encourage the inclusion of novel asset classes like digital assets.

The Road to Regulatory Clarity: A Chronology of Key Events

The journey towards potentially greater access to alternative assets in 401(k) plans has been marked by several key milestones:

- August 7, 2025: President Donald Trump issues an executive order directing federal agencies, including the Department of Labor, to examine and expand access to alternative assets in 401(k) plans, with a specific mention of digital assets.

- May 28, 2025: The Department of Labor rescinds its 2022 compliance release that had advised extreme caution regarding cryptocurrency investments in 401(k) plans. This action signals a significant policy pivot.

- March 24, 2026: The White House Office of Information and Regulatory Affairs (OIRA) completes its review of the Department of Labor’s proposed rule on alternative asset evaluation for 401(k) fiduciaries. The proposal is classified as "economically significant" and deemed "consistent with change."

- Following OIRA Review (Expected): The Department of Labor is anticipated to publish the proposed rule for a 60-day public comment period. This will be followed by a period of analysis of public feedback, potential revisions, and the eventual issuance of a final rule.

This timeline illustrates a deliberate and phased approach to regulatory reform, starting with executive direction and progressing through agency actions and interagency reviews.

Analysis of Implications: Broadening Investment Horizons and Fiduciary Responsibilities

The DOL’s proposed rule, if finalized, could have profound implications for the retirement savings landscape. By providing clearer guidelines for 401(k) fiduciaries on how to evaluate alternative assets, the proposal aims to reduce perceived risks and administrative burdens associated with offering such investments. This could lead to a wider array of investment options becoming available to plan participants, potentially including those seeking exposure to digital assets like Bitcoin and Ether, as well as private equity funds and real estate investment trusts.

For plan participants, this could mean greater diversification opportunities and the potential for enhanced returns, though it also introduces new considerations regarding risk management. Fiduciaries, on the other hand, will face the critical task of navigating these new opportunities responsibly. The proposed rule is expected to outline standards for due diligence, risk assessment, and the selection of suitable alternative investment vehicles. This may involve requiring fiduciaries to demonstrate a thorough understanding of the unique characteristics and risks associated with assets like cryptocurrencies, which have historically been characterized by high volatility.

The "economically significant" classification by OIRA suggests that the rule is anticipated to have a substantial annual effect on the economy, likely exceeding $100 million in direct or indirect costs or benefits. This underscores the broad impact this regulatory shift could have on the investment management industry, retirement plan providers, and ultimately, the retirement security of millions of American workers.

State-Level Initiatives: Indiana Paves the Way for Crypto in State Retirement Plans

While federal action is progressing, several U.S. states have also been proactively exploring ways to provide their citizens with greater access to digital assets within their retirement portfolios. Indiana stands out as a leader in this regard, having recently passed landmark legislation.

On February 25, 2026, Indiana lawmakers approved a bill that mandates certain state retirement and savings plans to offer a self-directed brokerage option. Crucially, this option must include at least one cryptocurrency investment choice by July 1, 2027. This pioneering legislation will empower Indiana citizens to hold digital assets, such as Bitcoin (BTC), as a component of their retirement plans for the first time. This move by Indiana reflects a growing recognition of digital assets as a legitimate investment class and a willingness by some governmental entities to embrace innovation in retirement planning.

Industry Reactions and Expert Perspectives (Inferred)

While specific official statements from industry stakeholders regarding this particular DOL proposal were not immediately available, the broader trend towards greater acceptance of alternative assets in retirement plans has been met with a range of reactions.

Financial advisors and asset managers specializing in alternative investments are likely to view this development positively, seeing it as an opening for expanded product offerings and client services. They may anticipate increased demand for educational resources and investment solutions that cater to the evolving needs of 401(k) participants.

Conversely, some institutional investors and retirement plan consultants may express a more cautious optimism. Their focus would likely be on the robustness of the regulatory framework, the clarity of fiduciary responsibilities, and the availability of reliable and secure custodianship solutions for digital assets. Ensuring participant protection and preventing potential for fraud or mismanagement will remain paramount concerns.

Organizations advocating for investor protection might emphasize the need for comprehensive disclosure requirements and robust oversight mechanisms to safeguard retirement savings. They would likely advocate for stringent standards regarding the selection of digital asset service providers and the security protocols employed.

The Investment Company Institute (ICI), a prominent trade association for the U.S. investment management industry, has historically engaged with regulatory bodies on issues affecting retirement savings. It is plausible that the ICI, in conjunction with other industry groups, will provide detailed feedback during the public comment period, focusing on market structure, investor protection, and the practical implementation of any new rules.

The Broader Context: A Global Trend Towards Digital Assets in Pensions

The developments in the United States are occurring within a broader global context of increasing interest in digital assets as an investment class, including within pension and retirement funds. In Australia, for instance, major pension funds have been reported to be considering the inclusion of cryptocurrency options amid growing demand from their members. This suggests that the conversation around integrating digital assets into long-term investment strategies is not confined to a single nation but is a burgeoning global trend.

The inclusion of alternative assets, particularly digital assets, in 401(k) plans represents a significant evolution in the retirement savings landscape. As regulatory bodies like the DOL continue to refine their frameworks, the accessibility and acceptance of a wider range of investment vehicles are likely to grow. This shift necessitates a careful balance between fostering innovation, ensuring robust investor protection, and empowering individuals to make informed decisions about their financial futures. The coming months, with the public comment period and subsequent final rule issuance, will be critical in shaping the future of alternative assets within America’s defined-contribution retirement system.