The discourse surrounding the Financial Independence, Retire Early (FIRE) movement has recently intensified, prompted by a candid critique from a reader of the popular blog, Mr. Money Mustache. The reader’s comment, reflecting a growing sentiment among aspiring FIRE enthusiasts, highlighted the perceived disconnect between foundational FIRE advice and the current economic realities of the post-pandemic world. Specifically, concerns were raised about the historical context of early FIRE adopters—often high-earning tech professionals who bought homes at significantly lower prices—and the challenges faced by individuals today who do not possess six-figure salaries or homeownership in an era of escalating housing costs and high interest rates. This critique underscores a pivotal question: are the core tenets of financial independence truly becoming obsolete, or do they simply require reinterpretation for a new economic landscape?

The Evolving Landscape of Financial Independence: A Historical Context

The FIRE movement, popularized in the early 21st century, advocates for aggressive saving and investing to achieve financial independence and early retirement. Its foundational principles—high savings rates, prudent spending, and strategic investing, often in low-cost index funds—gained significant traction, particularly among those with disposable income. Many early proponents, frequently from the burgeoning tech sector, leveraged substantial salaries in a period characterized by relatively stable economic growth, low inflation, and a more accessible housing market. This confluence of factors allowed for rapid accumulation of wealth, often culminating in the purchase of affordable homes that appreciated significantly, further accelerating their path to financial independence.

This "golden age" for early FIRE adopters, roughly spanning the decade leading up to 2019, presented an environment where a diligent application of Mustachian principles—a philosophy emphasizing extreme frugality and conscious consumerism—could yield accelerated results. Property acquisition, often through methods like "house hacking" (renting out portions of a primary residence) or purchasing fixer-uppers, was a cornerstone strategy, providing both reduced living costs and a significant appreciating asset. The economic backdrop was largely favorable, fostering a sense of attainable financial freedom for many who committed to the lifestyle.

Post-Pandemic Economic Shifts: A New Reality

The global economic landscape underwent a dramatic transformation following the onset of the COVID-19 pandemic. Supply chain disruptions, unprecedented fiscal and monetary stimuli, and shifts in consumer demand fueled a surge in inflation not seen in decades. In response, central banks, most notably the U.S. Federal Reserve, initiated a series of aggressive interest rate hikes. This swift policy shift had profound implications for various sectors, particularly housing and borrowing costs.

The reader’s comment directly addresses these shifts, lamenting that advice like "house hack" or "buy a fixer-upper" now seems "out of reach and/or complex to navigate with current prices and interest rates." This sentiment is well-founded. Mortgage rates, which hovered at historical lows for years, have climbed significantly, making homeownership considerably more expensive even for properties whose nominal prices haven’t skyrocketed. Furthermore, local zoning regulations, as the reader noted, often complicate innovative housing solutions like Accessory Dwelling Units (ADUs) or multi-unit conversions, limiting options for those seeking creative ways to reduce housing burdens.

The Housing Conundrum: A Data-Driven Perspective

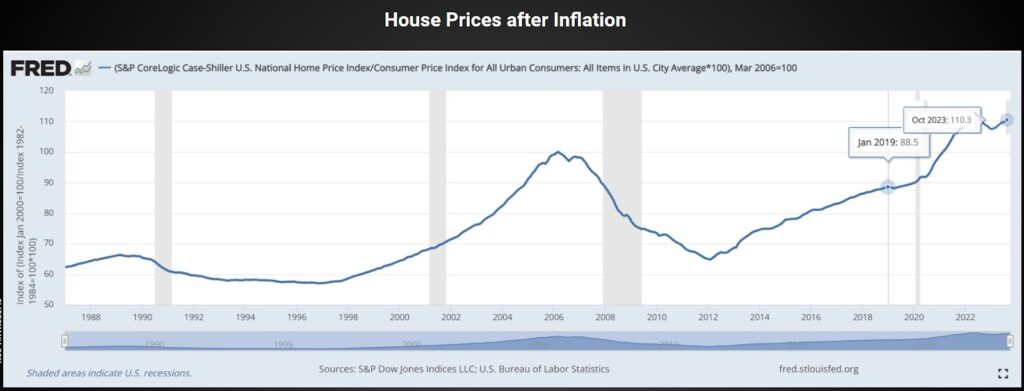

Housing affordability has emerged as a central challenge. To quantify this, data from the Federal Reserve Economic Data (FRED) shows that U.S. house prices, adjusted for inflation, have indeed risen notably since the beginning of 2019. While the national average indicates approximately a 25% increase relative to average salaries and the cost of other goods, it is crucial to note that this figure masks significant regional disparities. Intriguingly, when looking at a broader historical window, current inflation-adjusted prices are only about 10% higher than their peak in early 2006, nearly two decades ago. This suggests that while the recent surge is impactful, the long-term trend, when adjusted for inflation, is not as extreme as perceived in some narratives.

However, localized markets tell a different story. In areas like Longmont, Colorado, a case study cited by Mr. Money Mustache, the median home price has soared to approximately $540,000. This represents a threefold increase since 2011, far outpacing average salary growth and making homeownership significantly less accessible for the average person in that region. Such localized surges highlight that while national data provides a broad overview, individual experiences are heavily influenced by their specific geographic location. The combined effect of elevated housing prices and higher interest rates means that the monthly mortgage payment for a median-priced home has increased dramatically, diminishing purchasing power and making the traditional path to homeownership a much steeper climb.

Rethinking Housing Strategies: Beyond Traditional Ownership

In light of these challenges, the response from seasoned financial independence advocates emphasizes a return to fundamental Mustachian principles, particularly flexibility and data-driven decision-making. The core argument is that housing, like any other commodity, is subject to supply and demand, and consumers must adapt their expectations and strategies accordingly. This involves a critical evaluation of personal constraints versus market realities.

The first step, often termed "house shopping with your middle finger" (a provocative phrase emphasizing consumer empowerment), involves a dispassionate analysis of housing costs relative to value. This framework encourages individuals to consider a broader spectrum of options beyond their immediate locale. While emotional ties to a specific city or region are understandable, the financial implications of remaining in an unaffordable market can be substantial, potentially extending one’s working life by years or even decades.

This strategy necessitates a systematic approach:

- Needs Assessment: Clearly define essential housing requirements (size, amenities, location features).

- Market Analysis: Research rental versus buying costs, interest rates, and property values in the current desired location.

- Broadened Horizon: Extend the search to other cities, regions, or even countries where financial goals align better with housing costs.

- Decision: Make an informed choice between renting, buying, or implementing alternative strategies like geographical arbitrage.

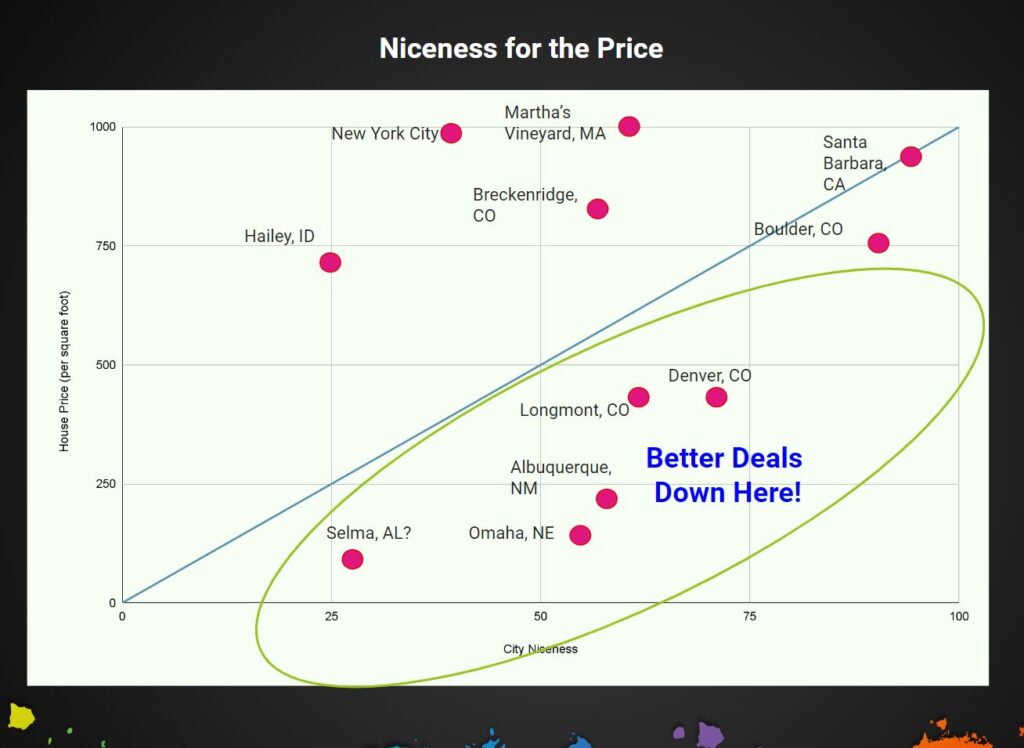

The concept of geographical arbitrage, moving from a high-cost-of-living area to a lower one while maintaining similar income or lifestyle quality, gains significant relevance here. This challenges the deeply ingrained societal expectation of remaining in one’s birth or current city, urging individuals to overcome the "fear of change" and explore opportunities where their money goes further. The observed irrational patterns in house prices across the country—ridiculously high in some desirable areas, yet surprisingly affordable in others with comparable amenities—present a clear opportunity for strategic relocation.

For instance, comparing Longmont, Colorado, with its $450 per interior square foot, to other cities, one might find a more desirable life at a similar price in Denver, or a significantly cheaper life in Albuquerque, as suggested by the Mr. Money Mustache analysis. This requires individuals to define their own metrics of "niceness" (e.g., climate, access to nature, urban amenities, community feel) and then actively seek out locations that offer an optimal balance of cost and quality of life.

Global Perspectives on Affordable Living

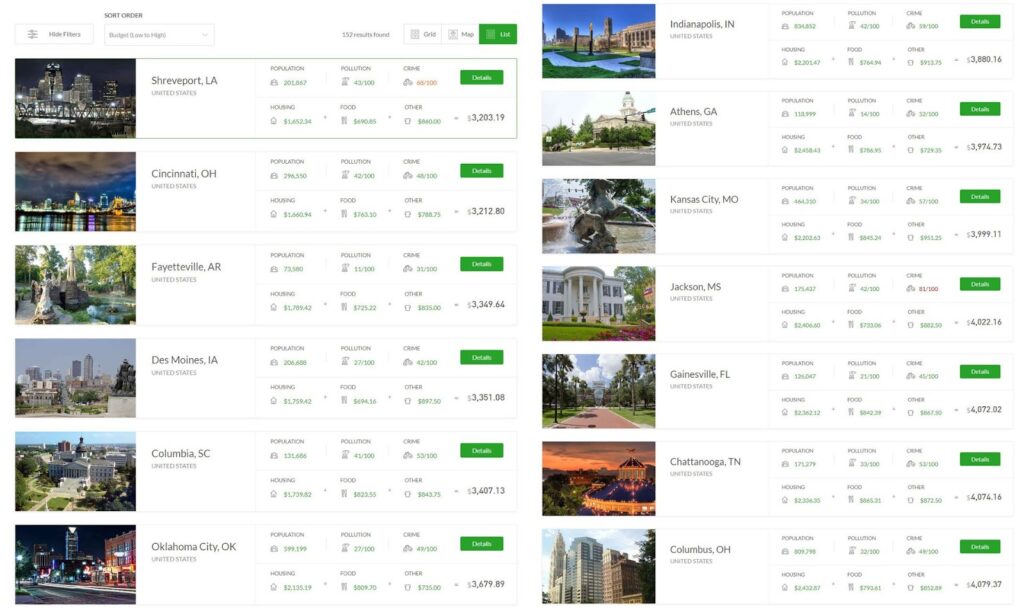

The strategy of geographical arbitrage extends beyond national borders. Tools like "The Earth Awaits," a site developed by FIRE bloggers, facilitate global searches based on personalized criteria such as budget, family size, housing type, and even climate preferences. A hypothetical search for a two-person family seeking a two-bedroom apartment outside a city center in North America, with January lows no colder than 10°F and a monthly budget of $0-$6000, yields diverse options. Cities like Fayetteville (AR), Columbia (MO), Athens (GA), and Chattanooga (TN) emerge as potential candidates, offering varied populations and amenities at significantly lower costs than prime metropolitan areas.

Venturing internationally further expands these possibilities. A similar search in South America reveals numerous cities where a comfortable life can be achieved on a fraction of a North American budget. While international relocation introduces complexities—navigating visas, legal systems, cultural differences, and maintaining ties with family—these are framed not as insurmountable obstacles but as "Adulting Puzzles." The argument is that the temporary "hassle" of paperwork and adjustment pales in comparison to the long-term burden of working for an additional decade or more simply to afford an expensive, but perhaps not optimally chosen, location. This perspective challenges individuals to embrace new experiences and recognize that adaptability is a powerful asset in the pursuit of financial independence.

The Enduring Principles of Mustachianism

Despite the shifting economic sands, the core principles of Mustachianism remain robust and, arguably, more vital than ever. The focus on streamlining spending, reducing waste, and living joyfully and efficiently without compromise is universally applicable, irrespective of income level or housing market conditions. The existence of high-earning professionals experiencing financial stress underscores the fact that income alone does not guarantee financial security; rather, it is the management of that income—minimizing wasteful expenditures and maximizing purposeful spending—that truly builds wealth.

The challenge of today’s economy demands a heightened commitment to these principles. When housing costs are higher and interest rates are less favorable, the margin for error in personal finance shrinks. This necessitates an even sharper focus on identifying and eliminating unnecessary expenses, seeking value in all purchases, and being strategically nimble with major life decisions, particularly housing. The fundamental lesson remains: financial independence is less about a specific income figure or asset price, and more about developing a mindset of resourcefulness, conscious consumption, and strategic flexibility.

Expert Commentary and Broader Implications

The Mr. Money Mustache blog’s analysis, while acknowledging the validity of the reader’s concerns, ultimately reinforces the adaptability of FIRE principles. The expert perspective suggests that while the specific tactics for achieving financial independence might evolve, the underlying strategy of maximizing savings and optimizing living costs remains timeless. The current environment may make the path more challenging for some, but it simultaneously highlights the power of proactive decision-making and geographical flexibility.

For young individuals entering the workforce today, especially those without six-figure salaries or existing home equity, the implications are clear:

- Income Optimization: While not the primary focus of Mustachianism, actively seeking to increase income through skill development, career advancement, or side hustles remains a powerful lever.

- Radical Frugality: The commitment to conscious spending and waste reduction becomes even more critical.

- Geographical Awareness: A willingness to consider relocation, both domestically and internationally, could be the most impactful strategy for achieving housing affordability and overall lower cost of living.

- Data-Driven Decisions: Relying on tools like FRED and "The Earth Awaits" empowers individuals to make informed choices based on facts rather than assumptions or emotional ties.

The current economic climate serves as a crucial test for the FIRE movement, demonstrating its resilience and adaptability. It challenges aspiring individuals to look beyond conventional advice and embrace a more dynamic, globally aware approach to financial planning.

Conclusion

The critique from a discerning reader has opened an important dialogue within the financial independence community, highlighting the very real challenges posed by current economic conditions, particularly in the housing market. While the "golden age" for some early FIRE adopters may be a historical artifact, the fundamental principles of conscious spending, efficient living, and strategic resource allocation are far from obsolete. Indeed, they are more pertinent than ever.

The key to navigating this new economic reality lies in adaptability and a willingness to challenge deeply ingrained assumptions. Housing, as the largest expense for most individuals, becomes the primary battleground. By embracing geographical arbitrage, leveraging data-driven research, and maintaining a flexible mindset towards where and how one lives, the path to financial independence, though perhaps more complex, remains attainable. The conversation initiated by the reader’s comment serves not as a dismissal of FIRE, but as a timely reminder that the pursuit of financial freedom is an ongoing journey requiring continuous learning, strategic adjustment, and a bold willingness to make choices that align with one’s long-term well-being, even if those choices mean moving to new horizons.