A recent commentary from a reader of the prominent Financial Independence, Retire Early (FIRE) blog, Mr. Money Mustache, has ignited a crucial discussion regarding the accessibility and relevance of FIRE strategies in the current economic climate, particularly for those not benefiting from historical advantages like high tech salaries or pre-2019 housing prices. The reader’s critique underscored a prevailing sentiment that much of the established FIRE advice, such as "house hacking" or "buying a fixer-upper," has become increasingly out of reach due to soaring housing costs, elevated interest rates, and restrictive local zoning laws in a post-pandemic world. This challenge, articulated by an individual who did not achieve early financial independence, raises valid questions about whether the movement’s foundational tenets can adapt to contemporary financial landscapes.

The Evolving Landscape of Financial Independence

The FIRE movement, a lifestyle philosophy centered on aggressive saving and investing to achieve financial independence and early retirement, gained significant traction in the early 21st century. Its core principles, often popularized by figures like Mr. Money Mustache (real name Pete Adeney), emphasize frugality, conscious spending, maximizing savings rates, and strategic investment. However, as the global economy has undergone profound transformations, particularly since 2019, the practical application of these principles has faced new hurdles. The reader’s comment reflects a growing concern that the "golden era" of FIRE, characterized by booming tech salaries and more affordable housing markets, may have passed, leaving newer aspirants struggling to replicate past successes.

This isn’t the first time the FIRE movement has faced questions about its longevity or adaptability. Throughout its history, critics have periodically declared FIRE "obsolete" in the face of various economic shifts, from market downturns to periods of high inflation. Yet, proponents argue that the fundamental principles of financial prudence, income optimization, and waste reduction remain timeless, requiring only strategic adaptation rather than wholesale abandonment. The current debate centers specifically on two significant factors: the perceived necessity of high, six-figure incomes and the dramatic escalation in housing prices and interest rates.

Income Generation: A Foundational Pillar

The reader’s observation that many early FIRE success stories originated from high-earning tech backgrounds highlights a persistent perception that substantial income is a prerequisite for achieving financial independence. While it is undeniable that higher incomes accelerate the path to FIRE by enabling larger savings rates, Mr. Money Mustache and other advocates consistently emphasize that income alone is not the sole determinant of financial success. The phenomenon of high-earning professionals, such as software engineers and doctors, experiencing financial stress despite decades of substantial income, serves as a stark reminder. This paradox underscores the crucial role of spending habits: even astronomical incomes can be squandered if not managed purposefully.

The core philosophy, therefore, pivots from merely earning more to efficiently managing what is earned. Strategies focus on streamlining spending, identifying and eliminating waste, and extracting maximum value and joy from expenditures. This approach, termed "Mustachianism," posits that financial independence is less about the absolute amount of income and more about the gap between income and expenses. These spending optimization skills become increasingly vital as one descends the income ladder, making them universally applicable, not exclusive to the affluent.

Decoding the Housing Market: 2019 vs. 2024

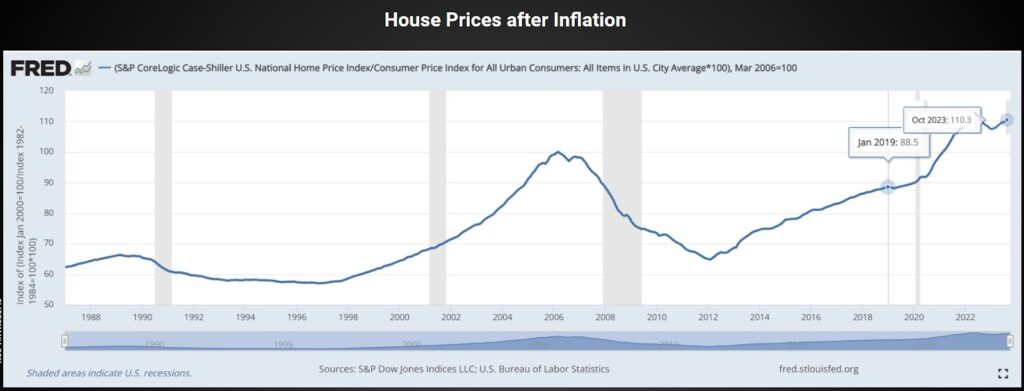

The most significant contemporary challenge highlighted by the reader is the state of the housing market. Post-2019, the United States has witnessed an unprecedented surge in housing costs, compounded by rising interest rates. Data from the St. Louis Federal Reserve (FRED) provides a quantitative perspective on this trend. Inflation-adjusted U.S. house prices have indeed risen, appearing approximately 25% more expensive in 2024 than at the beginning of 2019 relative to average salaries and the cost of other goods and services. This real increase in housing expense significantly impacts affordability, particularly for first-time homebuyers and those without substantial existing equity.

However, a broader historical view reveals a nuanced picture. Despite the sharp increase since 2019, inflation-adjusted house prices are only up about 10% since their last peak in early 2006, nearly two decades ago. This suggests that while the recent spike is substantial, the long-term trend, when adjusted for inflation, shows less dramatic appreciation than often perceived. Nevertheless, this national aggregate masks significant regional disparities. Highly desirable urban centers and rapidly growing suburban areas, such as Longmont, Colorado—where the median home price has surged to $540,000, roughly triple its 2011 value—have experienced much more accelerated growth than the national average. This disproportionate increase renders homeownership increasingly unattainable for average-income individuals in these specific locales.

The confluence of elevated prices and higher interest rates—with the average 30-year fixed mortgage rate, for instance, climbing from below 3% in early 2021 to over 7% by late 2023 and early 2024—further exacerbates the affordability crisis. A higher interest rate on an already inflated home price drastically increases monthly mortgage payments, pushing homeownership out of reach for many who might have qualified just a few years prior. This reality necessitates a re-evaluation of traditional homeownership strategies within the FIRE framework.

Geographic Arbitrage: A Mustachian Solution

In response to the localized housing crises, a cornerstone Mustachian principle resurfaces: geographic arbitrage. This strategy involves relocating to an area where the cost of living, particularly housing, is significantly lower while maintaining or improving one’s quality of life or income potential. The premise challenges the conventional attachment to a specific location, often driven by familial ties, historical roots, or a general fear of change. While these emotional bonds are valid, the FIRE philosophy encourages questioning assumptions and weighing the financial and lifestyle benefits of relocation against the comfort of familiarity.

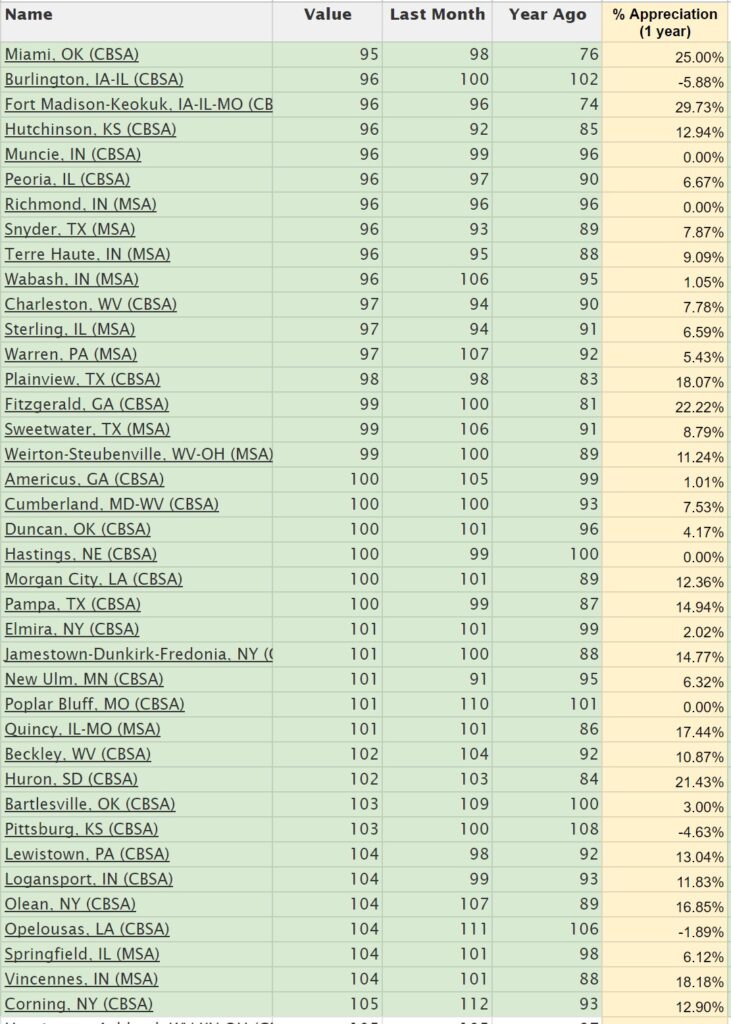

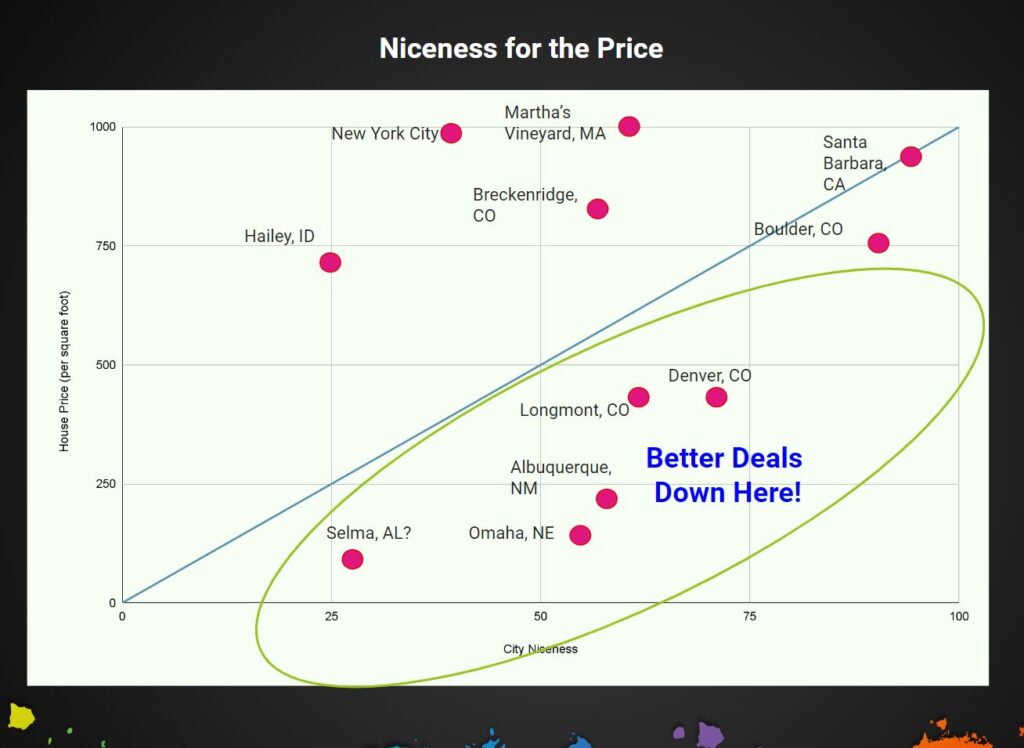

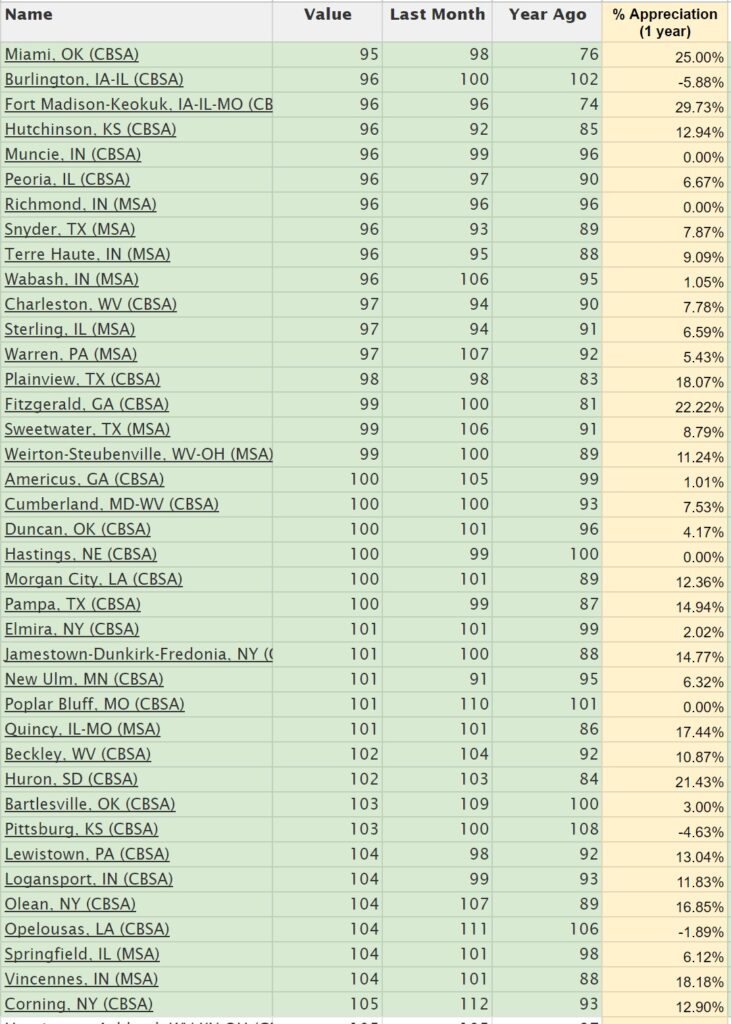

The irrational patterns of house prices across the United States, with some areas experiencing exorbitant costs and others offering remarkable affordability, create a distinct opportunity. This disparity isn’t always perfectly correlated with "niceness," as individual preferences for climate, culture, amenities, and community vary widely. For instance, a city like Longmont, Colorado, with its $450 per interior square foot average, now competes with a broader range of cities offering comparable or superior amenities at a similar or lower cost. Tools like FRED’s list of top 1000 metro areas, which provides price per square foot data, empower individuals to conduct data-driven searches for more financially advantageous locations. By sorting this data, one can identify a "band of affordability," for example, cities where a 2,000-square-foot home might cost around $200,000 (roughly $100 per square foot). This empirical approach allows for informed decisions, moving beyond anecdotal perceptions to concrete comparisons.

For example, a hypothetical comparison might pit Longmont against a city like Albuquerque, New Mexico, which could offer similar sunny climates and outdoor access at a significantly lower housing cost. Alternatively, for those willing to pay a premium for specific amenities, a move to a nearby, more expensive but potentially "nicer" city like Boulder, Colorado, might represent a better value proposition than staying in an increasingly costly Longmont if the perceived lifestyle upgrade justifies the expense.

Tools for Strategic Relocation

To facilitate this geographic arbitrage, several digital tools have emerged as invaluable resources. Beyond FRED’s housing data, "The Earth Awaits" is a notable example of a FIRE blogger-created platform designed to assist in identifying affordable living destinations, both domestically and internationally. Users can input specific criteria—such as geographic area, monthly budget range, family size, preferred apartment type (e.g., two-bedroom outside city center), and even climate preferences (e.g., January lows not colder than 10°F)—to generate a curated list of potential cities.

A search using these parameters for North America might yield a diverse list of cities like Fayetteville (Arkansas), Columbia (Missouri), Athens (Georgia), or Chattanooga (Tennessee). The platform often includes population data, offering a quick glimpse into the "feel" of a city, allowing users to narrow down choices based on preferences for smaller towns (e.g., 50k-200k population) versus larger metropolitan areas. This initial data serves as a launching pad for deeper research, encouraging individuals to explore local economies, job markets, cultural scenes, and community vibes before committing to a physical visit.

The example of comparing Tempe/Phoenix, Arizona, with Denver, Colorado, further illustrates the process. While their average housing costs per square foot might be relatively close ($272 for Phoenix vs. $299 for Denver metro), the qualitative differences become paramount. Both offer ample sunshine and mountain recreation, but their climates are distinct, and urban layouts vary. Such analysis underscores that the "best" location is subjective, often involving a trade-off between cost, climate, amenities, and personal preference. The concept of "seasonal arbitrage"—spending winters in a warmer, potentially more affordable locale like Phoenix and summers in a cooler, preferred region like Colorado—also emerges as a creative strategy for optimizing lifestyle and cost.

Navigating International Relocation

The concept of geographic arbitrage extends beyond national borders. For those seeking even greater financial advantages, particularly in housing and general cost of living, international relocation presents a compelling, albeit more complex, option. A similar search on "The Earth Awaits" for South America, for instance, might reveal numerous cities with significantly lower living costs than many parts of North America, alongside unique cultural experiences and diverse natural environments. Cities like Medellín (Colombia), Quito (Ecuador), or Cuenca (Ecuador) often appear on such lists, offering attractive cost-of-living profiles for those open to global exploration.

Moving to a new country introduces a new layer of "Adulting Puzzles": navigating citizenship and visa requirements, understanding foreign laws and traditions, adapting to new banking systems, and managing international travel for family visits. While these logistical challenges can seem daunting, they are often a series of solvable tasks rather than insurmountable obstacles. Proponents argue that the long-term benefits—a drastically reduced cost of living, exposure to new cultures, and an expanded worldview—far outweigh the initial administrative "hassle." The alternative, for many, is working an additional decade or more to afford an expensive life in a less-than-ideal location, a trade-off that often pales in comparison to the effort required for a strategic international move.

Conclusion: The Enduring Principles of Mustachianism

Ultimately, the core principles of the FIRE movement, or Mustachianism, remain robust and adaptable even in the face of contemporary economic challenges. The current housing crisis and high-interest rate environment do not render FIRE obsolete but rather necessitate a more strategic and flexible approach. While high incomes can accelerate the journey, the emphasis remains on optimizing spending, eliminating waste, and making conscious choices that align with one’s financial goals.

The most critical takeaway is that housing, like almost every other aspect of one’s financial life, is a choice. It is not an immutable external force but a variable that can be influenced through thoughtful analysis and decisive action. Whether through internal migration to more affordable domestic cities, exploring innovative housing solutions like house hacking (where local regulations permit), or embracing the adventurous path of international relocation, individuals possess agency in shaping their financial destinies.

The challenge presented by the reader serves as a vital reminder for the FIRE community to continuously refine its strategies and share practical, data-driven solutions that resonate with a broader audience facing diverse economic realities. By fostering open dialogue and collaborative exploration of "good living" locations and efficient lifestyle techniques, the collective pursuit of financial independence can continue to thrive, adapting to and overcoming whatever economic shifts the future may hold.