In the rural landscapes of Vermont, where the traditional county fair serves as both a cultural cornerstone and a concentrated marketplace, a growing movement toward early childhood financial literacy is taking shape through experiential learning. While many parents view the fairground as a site of inevitable impulse spending, educational observers and financial practitioners are increasingly utilizing these high-stimulation environments as "living laboratories" for economic instruction. A recent case study involving two children, aged five and seven, illustrates a structured pedagogical approach to money management that bridges the gap between abstract mathematical concepts and the realities of the modern consumer economy. This methodology, often referred to as a "family money philosophy," emphasizes the distinction between essential provisions and discretionary acquisitions, providing a framework for understanding labor, debt, and capital allocation before children reach adolescence.

The Vermont County Fair as a Consumer Microcosm

The annual county fair in Vermont represents a significant seasonal economic event, drawing thousands of visitors to a concentrated area of agricultural displays and commercial vendors. For children, the environment is a dense "panorama of consumerism," where marketing is directed specifically at their demographic through sensory appeals, including livestock interactions, vibrant toys, and specialty foods. From a journalistic perspective, the fair functions as a high-pressure testing ground for financial discipline.

Recent data from the Council for Economic Education suggests that while 25 states currently require high school students to take a personal finance course to graduate, the foundations of financial behavior are often set much earlier. Research indicates that by age seven, many children have already developed the cognitive capacity to understand basic economic concepts such as trade-offs and delayed gratification. The Vermont model leverages this developmental window by allowing children to navigate the fair’s commercial offerings using their own earned capital rather than relying on parental subsidies for non-essential items.

The Structural Framework: The Family Money Philosophy

The core of this educational strategy is a clearly defined "family money philosophy" that delineates the financial responsibilities of the parents versus those of the children. Under this system, the parental unit assumes the costs for all "needs," a category that includes shelter, clothing, healthcare, education, and basic nutrition. Furthermore, the parents cover the "admission capital"—the cost of entry to cultural and educational venues such as museums and the county fair itself.

However, once inside these venues, the financial dynamic shifts to a model of individual responsibility. The children are responsible for funding "discretionary items," categorized into three primary areas:

- Supplemental Nutrition: While parents provide standard meals, children must pay for "specialty" items, such as desserts at a restaurant or fair-specific treats.

- Souvenirs and Trinkets: Non-essential items, such as toys from a museum gift shop or inflatable items from a fair vendor, must be purchased with the child’s personal funds.

- Discretionary Literacy: In environments like the Scholastic Book Fair, where children are surrounded by curated marketing, the household policy dictates that while the home is stocked with library books and used volumes, new "premium" book purchases are the financial responsibility of the child.

This clear demarcation serves to demystify the adult world of finance, transforming money from a mysterious resource provided by parents into a finite tool earned through labor and allocated through choice.

Domestic Labor and the Internal Market Economy

To facilitate this system, the household operates an internal labor market. Children are offered the opportunity to perform specific chores with compensation set at what is described as "fair market value." This system introduces the concept of the "chore bundle" or lump-sum contracts, where children can negotiate higher payments for more complex or time-consuming tasks. For instance, a recent agreement in the study saw the seven-year-old child negotiate a $10 payment for a comprehensive reorganization of kitchen cabinetry—a task requiring significant organizational labor and duration.

The chore list is seasonally adjusted and scaled to the children’s developmental abilities. Current tasks include:

- Organizing domestic storage areas (e.g., shoe racks, kitchen drawers).

- Assisting with laundry for other family members (notably, children are not paid for their own laundry, which is considered a personal responsibility).

- Waste management, including emptying household bins and ensuring no debris is left in transit.

- Outdoor maintenance, such as filling bird feeders or assisting with gardening.

Crucially, the household distinguishes between "unpaid daily work" and "compensated labor." Unpaid tasks are those required for the functioning of the family unit, such as clearing the table, making beds, and collecting eggs from the family’s chickens. This distinction mirrors the real-world difference between personal maintenance and professional employment, teaching children that while some labor is a civic or familial duty, other forms of labor generate capital.

Case Study: The Inflatable Unicorn and the Mechanics of Debt

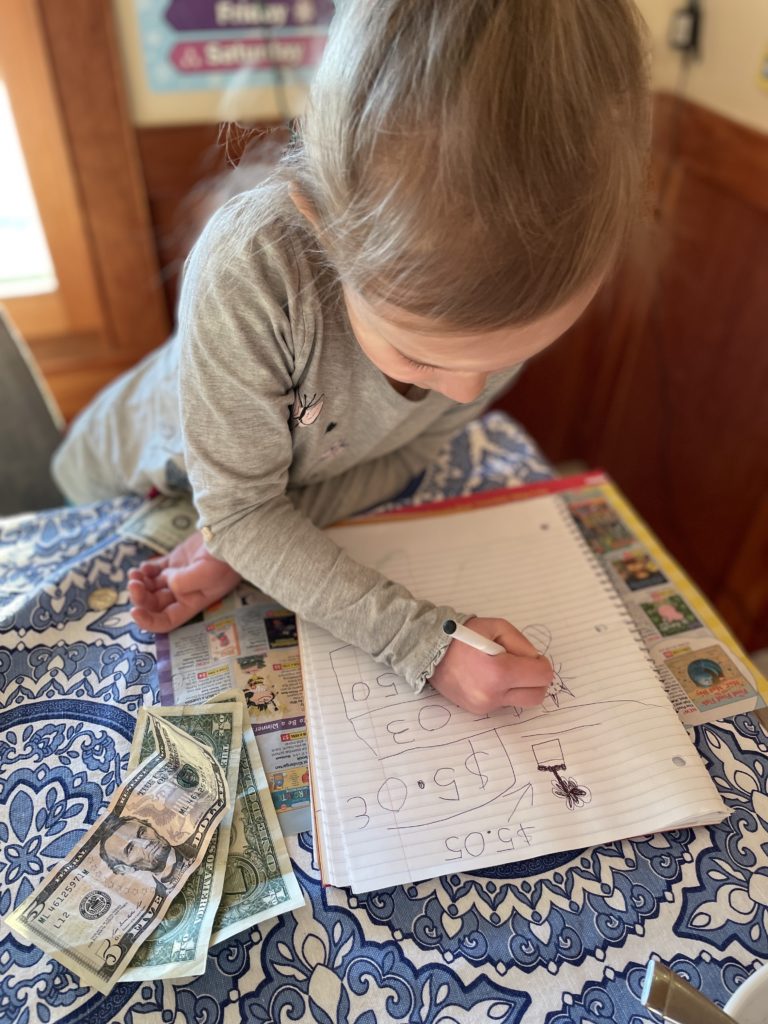

One of the most significant educational outcomes observed in this Vermont-based model occurred during the previous year’s county fair. A child sought to purchase an inflatable unicorn priced at $13, while possessing only $9 in personal capital. The parents opted to act as a lending institution, providing a $4 loan to cover the deficit.

The subsequent "repayment period" served as a visceral lesson in the psychological and economic burden of debt. Upon returning home, the child was required to perform mandatory chores to settle the $4 balance. The child eventually articulated a core economic frustration: "It is not fun to do chores to earn money for something I’ve already bought."

This experience highlights a critical aspect of financial pedagogy: the value of "safe failure." By allowing the child to enter a small, manageable amount of debt, the parents facilitated a first-hand understanding of interest-free but labor-backed credit. The child’s realization that debt effectively "steals" future time and labor is a concept that many adults struggle to internalize. Since this incident, reports indicate that neither child has opted to spend beyond their immediate means, demonstrating a long-term shift in their approach to liquidity and credit.

Collaborative Consumption and Currency Denominations

The educational model also addresses the complexities of collaborative spending. During visits to local farms for "pizza nights," the children were given the autonomy to purchase shared desserts. This led to a secondary lesson in cost-sharing and mathematics. When the elder child noted that she was disproportionately funding a dessert consumed by both, a negotiation ensued, resulting in a 50/50 split of the $7 cost.

This scenario required the children to engage in:

- Cost-Benefit Analysis: Determining if the dessert was worth the personal capital.

- Negotiation: Persuading a sibling to contribute to a shared goal.

- Applied Mathematics: Navigating the challenge of dividing an odd-numbered dollar amount ($7) and handling coin denominations to ensure an equitable split.

By requiring the children to physically approach the counter, place the order, and handle the currency, the parents removed the "frictionless" nature of modern transactions, forcing the children to recognize the tangible departure of their money.

Broader Impact and the "Bank of Parental Units"

The next phase of this financial education involves the introduction of long-term savings and the concept of compound interest. Plans are currently underway to establish a "Bank of Parental Units," an internal savings program that will pay a set interest rate on funds the children choose to save rather than spend.

Financial analysts suggest that this type of early exposure to interest is vital. According to the 2023 T. Rowe Price Parents, Kids & Money Survey, nearly 40% of parents say they are reluctant to discuss financial matters with their children. However, the Vermont case study suggests that transparency—explaining that "Mama is paid for her work and uses that money for our needs"—removes the anxiety and stigma often associated with household finances.

The broader implications of this "scaffolded" approach to financial literacy are significant. By treating money as a neutral tool—comparable to sleep, exercise, or nutrition—parents can equip children with the skills necessary to navigate an increasingly complex global economy. The goal is not merely to teach children how to save, but to help them view money as a means of achieving stability and autonomy, rather than as a measure of self-worth or an emotional surrogate.

As these Vermont children transition from counting coins to understanding interest rates, they represent a growing cohort of "economically literate" youth who are less likely to fall into the traps of predatory lending and impulsive consumerism in adulthood. The "Family Money Philosophy" thus serves as a template for other households seeking to turn everyday activities into lifelong lessons in economic resilience.