Beneath the overt drumbeat of geopolitical conflict and daily headlines of violence, a more insidious economic unraveling is quietly gaining momentum, challenging the very foundations of the global financial order. The unquestioned dominance of the U.S. dollar, a cornerstone of international finance for decades, is facing unprecedented scrutiny and erosion of trust. This shift is not the result of a sudden decision but a gradual, deliberate process, now accelerating to a potentially critical point.

The Foundations of Dollar Hegemony: A Historical Overview

The Bretton Woods system, established in 1944, pegged global currencies to the U.S. dollar, which was, in turn, convertible to gold. While direct gold convertibility ended in 1971, the dollar retained its preeminent status, largely due to the sheer size and stability of the U.S. economy and its commitment to a predictable global financial architecture. This was further solidified by the "petrodollar" system, forged in the 1970s, wherein major oil-producing nations, particularly in the Gulf, agreed to price oil in dollars and recycle their vast surpluses into U.S. Treasury bonds. In exchange, the U.S. provided security guarantees and military protection. This symbiotic relationship granted the U.S. extraordinary economic leverage, enabling it to finance large deficits, export inflation, and borrow at rates unavailable to other sovereign debtors. The stability of this system rested on two critical pillars: the perceived strength of the U.S. economy and, crucially, the reliability and neutrality of the U.S. government as a custodian of global assets. Recent events suggest that the latter pillar is being profoundly shaken.

A Chronology of Eroding Trust: Precedents and Provocations

The decline in confidence in the dollar system has unfolded through a series of distinct, yet interconnected, geopolitical and financial events.

Venezuela’s Gold: A Sovereign Test Case (2019)

The initial crack in the edifice appeared in 2019 when Venezuela, grappling with severe economic and political crises, requested the repatriation of 31 tonnes of its sovereign gold reserves, valued at approximately $2 billion, held at the Bank of England. To Caracas’s dismay, the request was denied. The Bank of England, acting on the U.K. government’s recognition of Juan Guaidó, an opposition figure who had never won a presidential election, as Venezuela’s "legitimate" interim president, refused to release the gold to Nicolás Maduro’s government.

This move, while framed by Western nations as a stand against an authoritarian regime, set a deeply troubling precedent. It demonstrated that sovereign assets, traditionally considered sacrosanct and immune from political interference, could be withheld based on political recognition and foreign policy objectives. For many nations, particularly those with less stable political relationships with Western powers, this was a stark warning: holding reserves in Western financial institutions carried an inherent, unquantifiable risk. While largely dismissed by mainstream commentary as a punitive measure against a "rogue state," the incident resonated deeply within central banking circles globally, sparking quiet discussions about asset diversification and jurisdictional safety.

Russia’s Frozen Billions: The Weaponization of Finance (2022)

The invasion of Ukraine by Russia in February 2022 escalated the weaponization of finance to an unprecedented level. In response to the aggression, Western nations, including the U.S., E.U., and U.K., froze approximately $300 billion of Russia’s foreign exchange reserves held in their jurisdictions. This move, while widely applauded in the West as a robust response to a flagrant violation of international law, sent shockwaves through the global financial community.

Never before had a G20 nation’s sovereign reserves been frozen on such a scale. This action fundamentally altered the perception of sovereign immunity for national assets. It signaled that even major economic powers could have their wealth effectively confiscated if they ran afoul of the prevailing geopolitical consensus. While the legal justifications were debated extensively, the practical implication was undeniable: assets held in Western financial systems were no longer universally safe havens.

Data from the International Monetary Fund (IMF) has since indicated a steady decline in the dollar’s share of global foreign exchange reserves, falling from over 70% in 2000 to around 58% by late 2023. This decline has coincided with a surge in central bank gold purchases, reaching record levels in 2022 and 2023. Nations like China, India, and other emerging economies have been at the forefront of this diversification, accumulating gold and exploring bilateral trade agreements in local currencies, explicitly citing concerns over financial weaponization. This collective, albeit often unspoken, action underscored the new reality: geopolitical risk had become a material factor in reserve management.

The ‘America First’ Doctrine and Alliance Strain (Post-2016 and Anticipated)

The presidency of Donald Trump, beginning in 2017, further contributed to the erosion of trust, not through direct asset seizures, but through a profound shift in U.S. foreign policy rhetoric and action. The "America First" doctrine introduced an era of unpredictable alliances, unilateral trade tariffs even against traditional partners, and public questioning of long-standing security commitments like NATO. Threats to annex Greenland, for instance, exemplified an unconventional approach to international relations.

This transactional view of international engagement implicitly undermined the second pillar of dollar hegemony: the reliability of the U.S. government as a stable, predictable custodian of the global system. Allies and adversaries alike began to perceive U.S. foreign policy as less anchored by multilateral norms and more susceptible to domestic political whims. The prospect of a potential return of such policies has exacerbated these concerns, suggesting that the post-World War II security architecture, once a bedrock for dollar confidence, could be renegotiated or withdrawn, leaving nations to fend for themselves.

The Petrodollar’s Precarious Position: From Shield to Bullseye

The cumulative effect of these events has been particularly pronounced in the Gulf Cooperation Council (GCC) states, which have been central to the petrodollar system for five decades. The original deal was elegantly simple: Gulf nations would price their vast oil exports in U.S. dollars, recycle the resulting surpluses into U.S. Treasuries and other dollar-denominated assets, and in return, receive robust American military protection. This arrangement provided the U.S. with perpetual demand for its currency and debt, while ensuring regional stability and security for the Gulf.

Changing Geopolitical Realities: Security Guarantees Under Fire

However, the security guarantee underpinning the petrodollar is now perceived to be failing. U.S. military bases across the Gulf—in Bahrain, Qatar, Kuwait, and the UAE—were historically presented as an impenetrable shield, a tangible manifestation of American commitment. Today, amidst escalating regional conflicts, particularly those linked to the ongoing conflict in Iran and the Red Sea, these bases have become liabilities. The countries hosting them are increasingly targeted by proxies and adversaries precisely because of the U.S. military presence. For instance, attacks by Iran-backed groups in Iraq and Syria, and Houthi missile and drone strikes targeting shipping in the Red Sea and potentially Gulf states, have demonstrated the vulnerability of the region. What was once a protective umbrella has, in many instances, transformed into a bullseye, drawing nations into conflicts they might otherwise avoid.

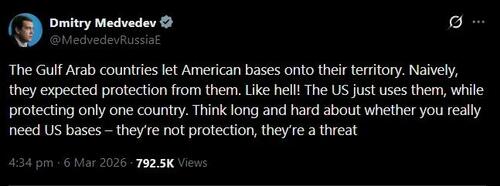

Dmitry Medvedev, former Russian President and current Deputy Chairman of the Security Council, notably articulated this sentiment with a pointed critique: "U.S. protection… is a liability dressed up as an asset." While often dismissed for his provocative rhetoric, Medvedev’s observation on this specific point appears prescient, capturing the growing sentiment among Gulf nations.

Gulf States Reassess: Investment Exodus?

Against this backdrop, reports indicate that GCC states are actively discussing the possibility of withdrawing significant investment commitments from the United States. These are not quiet, private deliberations but increasingly public conversations, signaling a clear shift in market sentiment. While no formal declarations have been made, the very public nature of these discussions suggests that capital markets are already anticipating a redirection of funds. Global capital, ever sensitive to risk and return, tends to move proactively. An actual announcement would merely formalize a trend already underway.

The consequences of such a shift for the U.S. Treasury market are profound. The petrodollar recycling loop has been a critical structural force in absorbing U.S. debt issuance and keeping borrowing costs manageable. Without this reliable source of demand from Gulf sovereigns, the U.S. will face greater challenges in financing its ever-growing national debt.

Strains in the US Treasury Market: A ‘Clusterfuck’ Brewing

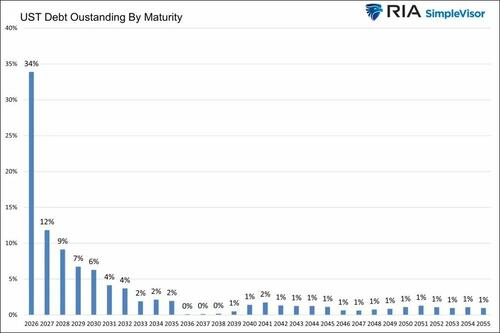

The U.S. Treasury market, the bedrock of global finance, is facing unprecedented strain. The nation’s national debt has surpassed $34 trillion, a figure projected to grow exponentially. In fiscal year 2025 alone, approximately $9.2 trillion in U.S. Treasuries are slated for rollover—representing roughly one-third of all outstanding federal debt. The refinancing wave for 2026 is similarly substantial.

Alarmingly, annual interest payments on the federal debt have now crossed the $1 trillion mark for the first time in history. This staggering figure consumes a growing portion of the federal budget, crowding out other essential spending and contributing to larger deficits. Despite efforts by the Treasury to manage the market through debt buybacks, the 10-year Treasury yield has continued its upward trajectory, reflecting persistent concerns about inflation, fiscal sustainability, and diminishing demand.

The potential withdrawal of Gulf sovereign wealth funds from U.S. Treasuries adds another layer of complexity. When a significant buyer base diminishes or turns into a seller, other market participants must absorb the supply. This inevitably happens at higher interest rates, further exacerbating the interest burden on the federal debt, widening the deficit, and necessitating even more debt issuance—a classic debt spiral.

The Quest for Alternatives: Collateral Over Currency

Underneath these immediate market pressures lies a deeper, more fundamental shift: a migration from a currency-based monetary order to a collateral-based one. For decades, U.S. Treasuries were universally considered the ultimate global safe asset—the default store of value in times of uncertainty. That status is now visibly eroding.

What is emerging as a replacement are commodities and physical assets. Nations and investors are increasingly seeking tangible, real-world assets—things that can be actually used, that are not subject to the political whims of any single government, and whose value is intrinsically tied to utility rather than fiat decree. This trend is no coincidence: the GCC nations, for example, are rich in precisely these types of assets, while the U.S. has inadvertently demonstrated its inability to reliably protect its allies’ financial interests or even its own military installations abroad.

The soaring prices of gold and silver, which hit record highs last year, are not solely attributable to inflation expectations or interest rate policy. They reflect a more profound, primal demand: a desire for a store of value that does not require implicit trust in governments that have proven themselves increasingly unpredictable and willing to weaponize financial systems. Central banks globally have been aggressively accumulating gold, signaling a systemic diversification away from dollar-denominated assets.

Turbulence in Private Credit Markets: A Canary in the Coal Mine

Beyond sovereign debt, cracks are also appearing in the burgeoning private credit market, a sector that has grown exponentially in recent years, offering an alternative to traditional bank lending.

In February, Blue Owl Capital, a prominent private credit firm, gated its retail private credit fund after redemption requests surged, effectively limiting withdrawals for investors. Following this, BlackRock, the world’s largest asset manager, announced similar restrictions on its $26 billion private credit fund. These actions by major players signal potential liquidity challenges within the sector. BlackRock had also recently written a private loan to zero, a loan that was marked at par just three months prior, marking the second such instance for the firm.

Further underscoring these concerns, Rubric Capital, a hedge fund spun out of Point72, issued a scathing letter to its limited partners, lambasting the private credit market as a "fraudulent bubble" and accusing certain players of "Enron-like accounting" to obscure underlying weaknesses and potential defaults.

While direct links to Gulf sovereign wealth funds’ capital flight are speculative, the pattern is clear: capital initially deployed into U.S. private markets under assumptions of political stability and reliable returns is now seeking an exit. The phrase "canary in the coal mine" has been used to describe Blue Owl’s situation; with BlackRock joining the trend, many analysts suggest the canary is not just singing but has indeed "ceased to be." This indicates a broader re-evaluation of risk and liquidity across U.S. capital markets.

The AI Paradox: Innovation vs. Instability

This unfolding financial instability presents a profound paradox for one of the most dynamic sectors of the U.S. economy: artificial intelligence. The "Magnificent Seven" technology giants have committed an astounding $600 billion in AI capital expenditure for 2026 alone. Such colossal investments presuppose a stable, predictable financial universe characterized by cheap dollars, stable long-term interest rates, and a reliable demand base for U.S. Treasuries.

The current AI investment model often relies on a circular system: Big Tech companies borrow cheaply in dollar-denominated markets, invest heavily in GPUs and other AI infrastructure, GPU manufacturers then reinvest their profits into Big Tech, and a virtuous cycle of valuation mark-ups ensues. This entire edifice is predicated on the continued integrity and stability of the dollar system.

However, the accelerating capital flight from U.S. markets, evidenced by the dramatic outperformance of emerging markets relative to the S&P 500 since January 2025, directly contradicts this assumption. The AI capital expenditure cycle and the global capital flight cycle are running in diametrically opposed directions. As the author succinctly puts it, "Something has to give. Burning refineries don’t care about your capex commitments." The stability required for such massive, long-term investments in AI infrastructure is increasingly at odds with the emerging realities of a fracturing financial order.

Broader Geopolitical and Economic Implications

The entire purpose of U.S. power projection in the Middle East—the extensive network of bases, the carrier strike groups, the explicit security guarantees—was never solely altruistic. It was fundamentally designed to protect the dollar system, ensuring the continuous flow of oil priced in dollars and the recycling of petrodollars into U.S. debt. This mechanism allowed the U.S. to sustain vast deficits, export inflationary pressures, and secure borrowing rates that other nations could only dream of.

The current escalation of conflicts in the Middle East, regardless of whether Washington actively chose this path or found itself drawn in, is having profound, unintended consequences for this long-standing arrangement. The Gulf states, once secure under the American umbrella, are now finding their alliance translated into vulnerability. They are reassessing what "ally" truly means in practice, particularly when their security assets become targets, and their financial assets are perceived as susceptible to political manipulation.

This period marks a critical juncture in global finance and geopolitics. The erosion of trust in the dollar as the world’s undisputed reserve currency, coupled with the instability in key financial markets, signals a potential acceleration towards a more multipolar financial future. This future may feature a greater reliance on alternative currencies, commodity-backed assets, and regional financial blocs, fundamentally altering the landscape of international trade, investment, and power dynamics. The "Bretton Whoops" is not merely an economic footnote; it is a seismic shift reverberating across the globe.