As the United States navigates another election year, the national discourse inevitably turns to the economy, a battleground where competing narratives often overshadow empirical data. While advanced financial practitioners and informed citizens understand the limited direct influence of any single administration on the colossal U.S. economic engine, political campaigns frequently leverage economic conditions to sway undecided voters in pivotal swing states. This election cycle, the rhetoric surrounding the economy has become particularly pronounced, with claims and counter-claims often rooted more in emotional appeal than in sound economic principles. This article aims to dissect common political misrepresentations about the economy, providing a fact-based analysis of the nation’s financial health and the real drivers behind its trends.

The Current State of the U.S. Economy: A Data-Driven Overview

Contrary to some prevailing political narratives, the U.S. economy exhibits significant strength across several key indicators. Official statistics paint a picture far removed from the "bad economy" often portrayed by opposition parties.

- Robust Job Market and Low Unemployment: The U.S. labor market has demonstrated remarkable resilience. As of recent reports from the Bureau of Labor Statistics (BLS), unemployment rates have hovered near historic lows, often below 4%. For instance, in September 2024, the unemployment rate stood at 3.8%, a figure that has remained consistently low for an extended period, reflecting a tight labor market where job opportunities are plentiful. This sustained period of low unemployment is indicative of a healthy economy, as widespread employment translates to greater consumer spending and economic activity. Historically, unemployment rates this low have been associated with periods of strong economic expansion.

- Steady Economic Growth (GDP): Gross Domestic Product (GDP), the broadest measure of economic activity, has shown consistent growth following the post-pandemic recovery. While growth rates fluctuate quarter-to-quarter, the overall trajectory has been positive, indicating an expanding economy. This growth is fueled by consumer spending, business investment, government expenditure, and net exports. The U.S. remains the world’s largest economy, contributing approximately 25% of global GDP, a testament to its scale and dynamism.

- Inflation and Wage Dynamics: One of the most contentious economic topics in recent years has been inflation. Following a surge in prices post-COVID-19, driven by a confluence of supply chain disruptions, robust consumer demand (partially fueled by government stimulus), and accommodative monetary policy, inflation has steadily moderated. The Consumer Price Index (CPI) peaked in mid-2022 but has since declined significantly, moving closer to the Federal Reserve’s target of 2%. As of late 2024, annual inflation rates have settled around 2.4%, a substantial improvement from peak levels.

Crucially, during this period, wage growth has largely kept pace with, and in many instances, outpaced inflation. Data from the BLS indicates that since 2019, overall prices have increased by approximately 19%, while average hourly wages have risen by around 21%. This means that, on average, American workers have seen their purchasing power maintained or even slightly improved, challenging the narrative that inflation has universally made life harder for Americans without commensurate wage adjustments. This real wage growth underscores a fundamental strength in the economy often overlooked in political debates.

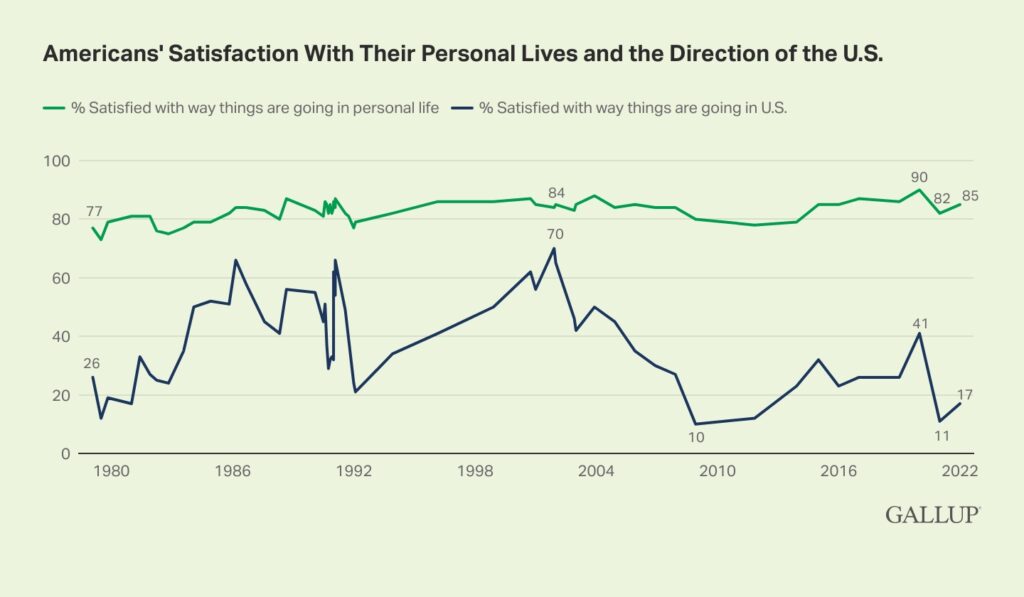

The Disconnect: Public Perception vs. Economic Reality

Despite these strong economic indicators, public sentiment often lags or diverges from objective data. A recent Gallup poll, for example, highlighted this disparity: while a significant majority of Americans (around 85%) reported doing well personally, only a small fraction (approximately 17%) believed the national economy was performing well. This mathematical impossibility—where most individuals thrive but the collective economy is perceived as struggling—points to the powerful influence of media narratives, political rhetoric, and the spread of misinformation, particularly through social media channels. The constant bombardment of negative economic messaging, irrespective of underlying facts, can shape public opinion more effectively than official statistics.

Deconstructing Political Economic Myths

Politicians, often eager to claim credit or assign blame, frequently simplify complex economic mechanisms for electoral advantage. Here, we address several persistent myths:

1. The President Controls the Economy: A Limited Lever

One of the most enduring political myths is the notion that a sitting president holds direct, comprehensive control over the U.S. economy. When the economy booms, incumbents often claim credit; when it falters, the opposition points fingers. However, the reality is far more nuanced. The U.S. economy is a vast, intricate, and largely free-market system, driven by billions of individual decisions made by consumers, businesses, and investors. Its sheer scale—representing a quarter of the global economy—and its deep integration into international markets mean that global events, technological advancements, and natural business cycles exert far greater influence than any single presidential administration.

While a president can influence economic conditions through fiscal policy (taxation, government spending), trade agreements, and regulatory changes, the effects of these policies are often delayed, indirect, and subject to congressional approval. Economic cycles of boom and bust are primarily driven by market forces, investor sentiment (periods of "irrational exuberance" followed by fear and pessimism), and external shocks. For instance, the 2007-2008 housing crisis and subsequent financial meltdown were products of complex market failures and regulatory shortcomings that unfolded over years, not simply the result of one president’s actions. Similarly, the post-pandemic recovery and inflation were influenced by global supply chains, international demand, and the collective responses of central banks worldwide. The president’s role is more akin to a captain steering a massive supertanker through turbulent seas; they can adjust the rudder and throttle, but they cannot control the ocean’s currents or sudden storms.

2. The President Controls Interest Rates: The Federal Reserve’s Mandate

Another common political promise is the pledge to "fight" to bring down interest rates, often framed as an act of sympathy for middle-class Americans struggling with higher borrowing costs for mortgages, car loans, and credit cards. This rhetoric fundamentally misunderstands or intentionally misrepresents the role of the Federal Reserve.

The Federal Reserve (the "Fed") is the independent central bank of the United States. Its primary mandate is to achieve maximum employment and maintain price stability (i.e., control inflation). To fulfill this mandate, the Fed utilizes monetary policy tools, most notably adjusting the federal funds rate, which influences interest rates throughout the economy. This independence from political interference is crucial for the Fed to make sound, long-term economic decisions, free from the short-term pressures of election cycles. Historically, countries where central banks lack independence and are subject to political dictates (e.g., Argentina, Turkey) often suffer from runaway inflation and economic instability.

When the economy "gets too hot" with excessive demand and rising inflation, the Fed raises interest rates to cool it down, making borrowing more expensive and encouraging saving. Conversely, during economic downturns, the Fed lowers rates to stimulate borrowing, investment, and job creation. These are critical "gas and brake pedals" for the economy. A president bullying Fed officials or threatening to "take over" the department, as some candidates have done, undermines this vital independence and could lead to disastrous economic consequences.

3. Inflation Has Made Life Harder for Americans (and the President Can Magically Reverse It)

As discussed, while the post-COVID period saw a significant spike in inflation, it was a complex phenomenon driven by a unique confluence of factors: supply chain disruptions (factory closures, remote work), strong consumer demand (government stimulus), and historically low interest rates. These factors have largely resolved themselves, bringing inflation back to near-target levels.

The most significant counterpoint to the "inflation has made life harder" narrative is the concurrent rise in wages. When wages outpace or keep pace with inflation, the average American’s purchasing power remains stable or improves. The political promise to "bring prices back down" is also problematic. While reducing the rate of inflation (disinflation) is desirable, a broad reduction in absolute prices (deflation) is typically a sign of a severely struggling economy, leading to reduced corporate profits, wage cuts, and increased unemployment. Economic growth inherently involves some level of price and wage increases; the key is balance and sustainable growth.

Furthermore, the notion that "greedy corporations" are solely to blame for price increases, using "greedflation" as a political talking point, often oversimplifies market dynamics. While businesses seek to maximize profits, competitive markets generally prevent widespread, sustained price gouging without underlying cost pressures. Independent analyses, such as one conducted by NPR on grocery prices, often find that profit margins for industries during inflationary periods do not show evidence of unusual "windfall profits" that could be solely attributed to corporate greed, but rather reflect increased input costs, labor expenses, and supply chain challenges.

4. The President Controls Housing Prices: A Multifaceted Challenge

The housing market has been a significant concern, with both house prices and rents rising faster than general inflation and wages over the past decade. This trend has been exacerbated by rising interest rates, making homeownership less affordable due to higher mortgage costs, creating a "double whammy" for prospective buyers.

The political discourse often includes proposals such as subsidies for first-time homebuyers or schemes to artificially reduce interest rates. However, these solutions, while seemingly benevolent, often worsen the problem by artificially inflating demand without addressing the fundamental issue: an insufficient supply of housing. When demand outstrips supply, prices inevitably rise.

The real solutions lie in structural reforms to increase housing supply. This includes:

- Streamlining Permitting and Zoning: Reducing bureaucratic hurdles, accelerating permit approvals, and modernizing outdated building codes can significantly lower construction costs and time.

- Zoning Reform: Eliminating restrictive single-family zoning, minimum lot sizes, setback requirements, and excessive parking mandates allows for denser, more diverse housing types (duplexes, townhouses, small apartment buildings) to be built in desirable areas.

- Limiting NIMBYism: Reforming laws that grant excessive power to "Not In My Backyard" groups, allowing a vocal minority to block essential housing developments, can unlock new construction.

By reducing the cost and complexity of building, the supply of housing can increase, eventually leading to more affordable prices and rents. This is a local and state-level issue as much as a federal one, highlighting the limited direct control a president has.

5. The President Controls Gas Prices, and They Are "High" and We Want Them Lower: An Outdated Metric

Gasoline prices remain a disproportionately significant talking point in U.S. elections, despite their diminishing economic relevance for many households. The political blame game over gas prices is particularly perplexing given several facts:

- Historical Context: On an inflation-adjusted basis, gasoline prices in the U.S. typically fluctuate within the $3-$4 per gallon range, a level consistent with prices seen in the 1950s. While daily fluctuations can feel significant, the long-term trend, when adjusted for inflation, shows remarkable stability.

- Relative Spending: For the average American household, spending on gasoline accounts for a relatively small percentage of disposable income, typically around 2.5%. This is often dwarfed by other vehicle ownership costs like insurance, maintenance, depreciation, and loan payments, which collectively represent a much larger financial burden.

- Technological Obsolescence: Perhaps most critically, gasoline as a primary fuel source is rapidly becoming obsolete. The widespread availability and increasing affordability of electric vehicles (EVs) offer consumers a superior alternative. Used EVs can often be purchased for less than comparable internal combustion engine (ICE) vehicles, and new EVs are increasingly competitive, especially when considering fuel savings (electricity is significantly cheaper per mile than gasoline) and reduced maintenance. EVs offer a faster, quieter, and cleaner driving experience, often with lower total cost of ownership.

Given these realities, continued political focus on gas prices is akin to debating the price of Kodak film or typewriters in the digital age—it’s a distraction from more pressing and modern economic realities and opportunities.

Beyond Economic Metrics: The Pursuit of "Enough"

Perhaps the most profound critique of current economic discourse is its fundamental premise: that the economy should be a constant source of worry, and that more material wealth is always the answer to national happiness. The U.S. has long surpassed the point of having "enough" in terms of basic necessities and widespread material comfort. When segments of the American middle class lament their economic struggles, it often resembles overfed individuals at a lavish buffet wishing for "just one more flavor of donuts."

While acknowledging genuine issues like income and wealth inequality is crucial—and a progressive tax system can help foster a more equitable and peaceful society—it’s also important to recognize that beyond a certain point, increased wealth does not correlate with increased happiness. Research consistently shows that psychological well-being is less about the absolute amount of money one has and more about financial security, personal fulfillment, strong social connections, and a sense of purpose.

If politicians genuinely prioritized the happiness and well-being of their constituents, their platforms might focus less on pandering to specific interest groups or promising endless material growth, and more on principles that foster financial independence, resilience, community engagement, and a sustainable lifestyle. Such principles, often found in movements advocating for mindful consumption and purposeful living, emphasize that "enough" is primarily a mindset and a collection of life skills, not merely a larger paycheck.

The Imperative of Economic Literacy

The current election cycle underscores the critical need for economic literacy among both politicians and the electorate. When public perception is shaped by misinformation rather than factual data, sound policy decisions become challenging, and citizens are less equipped to make informed choices. Resources like "USA Facts," an initiative by former Microsoft CEO Steve Ballmer, aim to provide unbiased, data-driven insights into national trends, offering a valuable counter-narrative to political hype.

Ultimately, citizens are encouraged to conduct their own research, scrutinize political claims, and understand the real mechanisms driving the economy. Casting an informed vote is just one step; maintaining an awareness of economic realities and focusing on elements within one’s "circle of control" are crucial for personal financial well-being and contributing to a more rational public discourse. The goal should be to move beyond partisan bickering and towards a shared understanding of how things really work, for the collective betterment of the nation.