The annual county fair in Vermont, a traditional staple of rural American life, served this year as a primary laboratory for an intensive case study in early childhood financial education. While such events are typically characterized by agricultural displays and communal entertainment, they also represent high-density consumer environments where marketing is frequently directed at minors. In response to these pressures, a pedagogical framework has emerged that utilizes real-world transactions to teach children, specifically in the five-to-seven-year-old demographic, the fundamentals of labor, debt, and discretionary spending. This approach, often referred to as "scaffolding," seeks to demystify the abstract nature of currency by grounding it in tangible effort and consequence.

The Structural Framework of the Family Economic Model

The methodology observed in this Vermont-based model rests on a clear demarcation between essential needs and discretionary wants. Under this system, parents or guardians assume full financial responsibility for "needs," which are defined as clothing, shelter, healthcare, basic nutrition, and educational materials. Furthermore, the cost of admission to cultural and communal events, such as museums or fairs, is covered by the household budget.

However, a strict boundary is drawn regarding "wants." These include souvenirs, specialized snacks, and items from commercial entities such as the Scholastic Book Fair. By shifting the financial burden of these items to the children, the model forces a transition from passive consumption to active economic decision-making.

To facilitate this, children are provided with opportunities to earn "commissions" through a tiered chore system. Unlike traditional allowances, which are often granted regardless of behavior or contribution, this system mirrors a market economy. Compensation is based on the completion of tasks that benefit the family unit as a whole, rather than tasks related to personal hygiene or individual responsibility.

Chronology of Financial Development: From Labor to Debt Management

The implementation of this financial literacy program follows a specific chronological progression, beginning with the concept of labor-for-value and advancing toward complex concepts of credit and partnership.

-

Phase One: The Labor-Value Connection. Children are introduced to the concept that money is a finite resource earned through effort. Chores such as cleaning common areas, organizing kitchen infrastructure, or assisting with seasonal property maintenance (e.g., stacking wood) are compensated at a perceived "fair market value." For instance, a comprehensive reorganization of kitchen cabinets might command a $10 lump sum, provided the work meets quality standards.

-

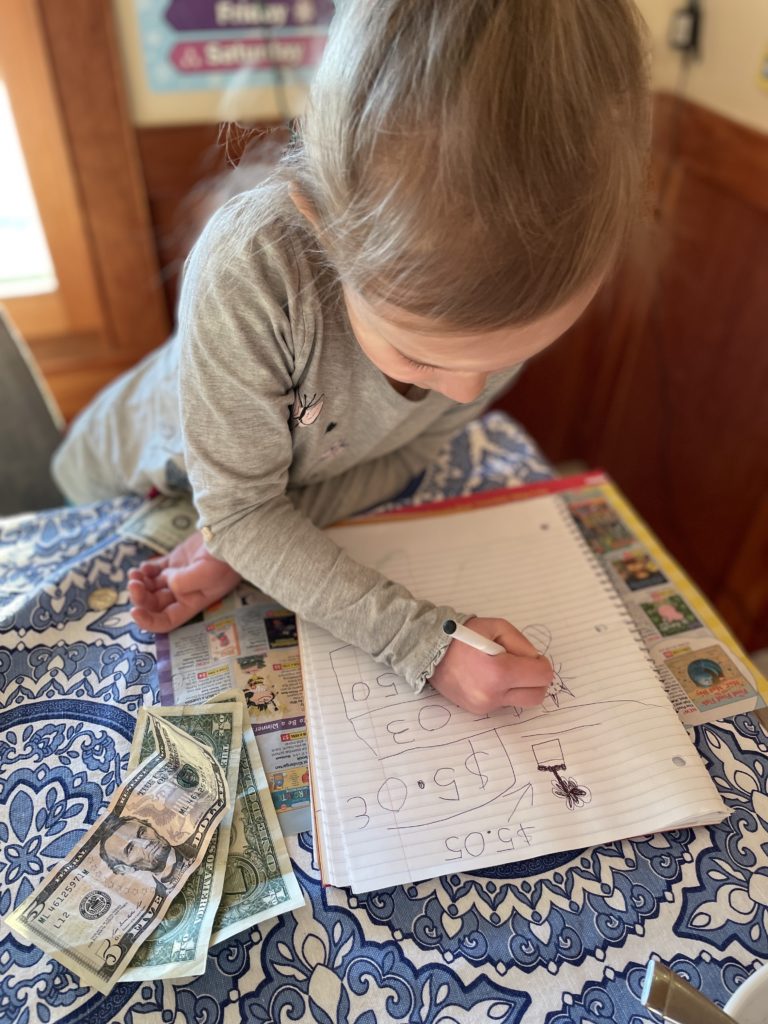

Phase Two: The Experience of Debt. A pivotal moment in the development of financial literacy occurs when a child’s desire for a product exceeds their current liquidity. In a documented instance at a previous Vermont fair, a child sought to purchase a $13 inflatable item with only $9 in cash. The parents facilitated a $4 loan, creating a real-world debt scenario. The subsequent "repayment phase" involved mandatory labor where the child received no immediate reward, as the earnings were diverted to settle the debt. This phase is critical for developing a visceral understanding of the "opportunity cost" of credit.

-

Phase Three: Collaborative Spending and Negotiation. As children gain experience, they often encounter scenarios requiring cost-sharing. Observations show that siblings may choose to pool resources for shared treats, such as desserts at a restaurant. This introduces the complexities of division (e.g., dividing a $7 expense between two parties) and the necessity of negotiation regarding usage and contribution.

-

Phase Four: Independent Transaction Execution. The final stage of the current progression involves the child managing the entire transaction. This includes remembering to bring their own wallet to a venue, selecting the item, interacting with the cashier, and ensuring the correct change is received.

Supporting Data: The State of Youth Financial Literacy

The necessity of such home-based programs is underscored by national statistics regarding financial literacy. According to the 2023 Survey of the States by the Council for Economic Education, only 25 states currently require high school students to take a course in personal finance to graduate. While this is an increase from previous years, it leaves a significant gap in early childhood education.

Furthermore, data from T. Rowe Price’s 15th Annual Parents, Kids & Money Survey indicates that nearly 40% of parents feel "uncomfortable" discussing money with their children. This discomfort often leads to a "money silence" that can result in poor financial habits later in life. In contrast, children who are exposed to financial concepts before age seven are significantly more likely to develop healthy saving habits and understand the basic mechanics of inflation and interest by the time they reach adolescence.

Research from the University of Cambridge suggests that many basic money habits are formed by age seven. This supports the Vermont model’s focus on the five-to-seven-age range as the optimal window for introducing "scaffolding" techniques.

Expert Analysis: The Psychological Impact of Debt Education

Financial analysts and child psychologists note that the "work-off-debt" strategy is particularly effective because it removes the abstraction of credit cards. When a child experiences the "unpleasantness" of working without a resulting payout—because the payout was spent in the past—it creates a lasting psychological deterrent to impulsive borrowing.

"The goal is to move money from the realm of ‘magic’ to the realm of ‘tools,’" says one independent financial consultant familiar with the Vermont case. "When a child sees a parent tap a card at a grocery store, they don’t see the hours of work behind that tap. By requiring the child to physically count coins and work for ‘wants,’ the parents are providing a map of the adult world that is usually hidden."

This methodology also addresses the "status" associated with money. By treating it as a tool—similar to water, sleep, or exercise—the framework attempts to reduce the anxiety and emotional weight often attached to wealth.

Broader Implications and Future Projections

The success of experiential learning in Vermont suggests a potential shift in how modern families approach the "allowance" debate. The transition from a passive allowance to a commission-based system reflects a broader economic trend toward the "gig economy" and self-directed income.

The next planned evolution for this specific case study involves the introduction of the "Bank of Parental Units." This concept involves the parents paying a high internal interest rate on any money the children choose to save rather than spend. This is designed to teach the concept of "compound interest" and the "time value of money."

However, the model is not without its challenges. The primary risk involves the emotional toll of "forgotten wallets" or lost funds. In one instance at a science museum, a child misplaced her wallet, leading to significant emotional distress. While the wallet was eventually recovered, the incident served as a stark lesson in the responsibility of ownership. Experts suggest that these "micro-failures" in a controlled environment are essential, as they prevent "macro-failures" in adulthood when the stakes are significantly higher.

Conclusion: A Scalable Model for Early Education

The Vermont county fair serves as a reminder that every consumer interaction is a potential classroom. By adopting a formal "Family Money Philosophy," parents can transform routine outings into sophisticated lessons in economics. The data suggests that while the lessons may be simple—counting change, comparing prices, and working off debt—the long-term impact on financial stability is profound.

As the children in this case study move toward adolescence, the scaffolding will likely expand to include stock market basics, charitable giving, and household budgeting. For now, the focus remains on the foundational belief that money is a tool to be mastered, not a mystery to be feared. The "boring meetings" and "serious but kind" interactions of the adult professional world are being translated into a language that five- and seven-year-olds can not only understand but also apply to their own lives.