The financial trajectory of Michael and Brian, a 34-year-old couple residing in central Connecticut, serves as a poignant case study for the economic challenges facing many mid-career professionals in the current New England market. Despite a robust household gross income of approximately $167,544, the couple faces a complex intersection of consumer debt, rising housing costs, and the psychological weight of "dreams deferred." Their situation highlights the precarious nature of financial stability when high-earning potential is met with unexpected life events, such as forced relocation and medical emergencies. This report examines their current financial standing, the timeline of events leading to their current debt load, and the strategic recommendations for achieving long-term solvency and home ownership.

Current Financial Status and Household Dynamics

Michael and Brian represent a dual-income household with significant professional contributions to the state of Connecticut. Michael operates as a project coordinator for a state behavioral health agency focusing on youth, supplemented by a secondary role as a disability leadership coordinator. Brian serves as a quality assurance manager for a state-run hospital. Their combined net annual income, after taxes and primary deductions, stands at $109,455.42.

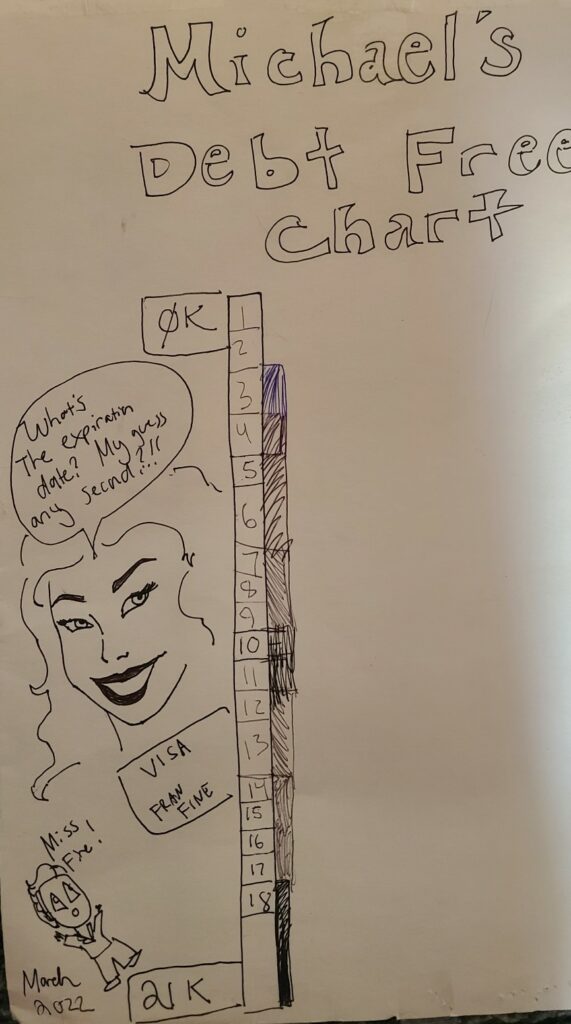

While their income is substantial, the couple is currently burdened by $28,259 in consumer debt, primarily distributed across three credit cards. A significant portion of this debt—approximately $16,057 on a Sharon Credit Union Visa—is currently under a 0% introductory APR that is set to expire in November 2023, at which point the rate will escalate to 17.99%. This "interest cliff" creates a time-sensitive pressure on their capital allocation.

The couple’s asset portfolio is valued at approximately $91,250, though the majority is illiquid, held in various retirement vehicles including 401k, 403b, 457b, and HSA accounts. Their liquid savings are relatively low, with Michael holding $7,000 in an emergency fund and Brian maintaining $1,000 in personal savings. This lack of liquidity, combined with high monthly expenditures, has created a sense of financial stagnation despite their professional success.

Chronology of Financial Disruption (2013–2023)

The couple’s current financial anxiety is rooted in a series of disruptive events over the past decade, culminating in a turbulent 2022–2023 fiscal year.

- 2013–2021: Stability and Debt Reduction: Since entering a relationship in 2013, the couple maintained a modest lifestyle in a 600-square-foot studio apartment with a monthly rent of $945. During this period, Brian successfully eliminated $58,000 in student loan debt, a significant milestone that should have positioned the couple for home ownership.

- August 2022: The Housing Pivot: Based on their low overhead, the couple forecasted a re-entry into the housing market by late 2023. They aimed to transition from renters to owners, leveraging Brian’s career move from the private sector to a more secure state position with a pension and lifelong benefits.

- Late 2022: Forced Relocation and Medical Crisis: The couple’s plans were derailed when they were forced to vacate their long-term residence. Simultaneously, they adopted two kittens that required extensive veterinary care for gastrointestinal issues. These "unplanned expenses" led to the accumulation of the current $28,259 consumer debt load.

- 2023: The New Rental Reality: The couple moved into a two-bedroom, two-bathroom apartment in a refurbished industrial mill. While the space offers 12-foot ceilings and modern amenities, the rent doubled to $2,000 per month. This increase, combined with Connecticut’s high utility rates and Brian’s significant car repair costs (averaging $1,064 monthly over eight months), has compressed their ability to save for a down payment.

Supporting Data: The Connecticut Economic Landscape

The financial pressures felt by Michael and Brian are reflective of broader economic trends in Connecticut. According to data from the U.S. Bureau of Labor Statistics and local housing authorities, Connecticut remains one of the most expensive states for both utilities and housing in the Northeast.

- Utility Costs: The couple reports an average monthly electricity bill of $235. Connecticut consistently ranks among the top five states for the highest residential electricity rates in the country, driven by high delivery charges from major suppliers like Eversource and United Illuminating.

- The Rental-to-Ownership Gap: With a median home price in Connecticut hovering near $380,000 as of mid-2023, a standard 20% down payment would require $76,000. Currently, the couple’s liquid assets ($8,000 combined) represent only 10% of that goal.

- The "Millennial Debt" Phenomenon: Like many in their cohort, Michael and Brian have experienced "lifestyle creep" necessitated by the market. The transition from a $945 studio to a $2,000 apartment was not a choice of luxury but a result of a 2022 rental market characterized by low inventory and surging demand.

Debt Obligations and the November Deadline

The most critical factor in the couple’s immediate financial health is the structure of their debt.

| Creditor | Balance | Interest Rate | Note |

|---|---|---|---|

| Brian’s Visa (SCU) | $16,057 | 0% (17.99% after Nov 2023) | Immediate priority |

| Michael’s Visa Platinum | $9,700 | 10.99% | High priority |

| Brian’s Visa (Navy Fed) | $2,503 | 0.99% (17.74% after Nov 2023) | Smallest balance |

To avoid a massive increase in monthly interest charges, the couple must aggressively pay down the $16,057 balance before the November anniversary. Financial analysts suggest that failure to do so could result in an additional $240 per month in interest alone, further stalling their home ownership goals.

Expert Analysis and Strategic Recommendations

Financial consultant Liz Frugalwoods, who reviewed the case, emphasizes that the couple is in a "stronger position than they realize," provided they shift from a defensive to an offensive financial posture. The primary recommendation is a "spending detox" to reallocate capital toward debt.

Expenditure Realignment

The couple’s current monthly spending is approximately $8,035. Analysis suggests that by eliminating discretionary spending—such as dining out ($200), home goods ($200), and personal care ($180)—the couple could reduce monthly outflows to $6,665. This would free up an additional $1,370 per month. When combined with their existing debt payment allocations, the couple could potentially apply over $4,400 per month toward their balances, achieving total debt freedom in approximately 6.5 months.

Retirement and the "Triple Crown" Advantage

One of the couple’s greatest strengths is Brian’s access to a 403b, a 457b, and a state pension. The 457b is particularly valuable as it allows for penalty-free withdrawals upon separation from service, regardless of age, providing a unique bridge for early retirement. Experts recommend that once the consumer debt is cleared, the couple should maximize these contributions to reduce their taxable income, which is currently a significant burden on their gross earnings.

The Graduate School Dilemma

Brian has expressed interest in pursuing a master’s degree to achieve "academic success." However, from a strictly journalistic and financial analysis perspective, the Return on Investment (ROI) for such a degree must be scrutinized. Unless the degree is tied to a guaranteed salary increase within the state system, the tuition costs and time commitment could act as a further "unhelpful detour" from the primary goal of home ownership.

Broader Implications and Long-term Outlook

The case of Michael and Brian illustrates a common struggle for the "HENRY" (High Earner, Not Rich Yet) demographic. They possess the income to be wealthy but lack the liquid capital to secure traditional markers of adulthood, such as real estate. Their feeling of "shame" is a documented psychological response to the disconnect between professional achievement and financial liquidity.

In the broader context of the U.S. economy, the couple’s reliance on state-sponsored benefits (pensions and HSAs) highlights the growing divide between public-sector stability and private-sector volatility. As they move toward their 10-year anniversary, their ability to pivot from "emergency mode" to "strategic accumulation" will depend entirely on their discipline in the fourth quarter of 2023.

If the couple adheres to the recommended debt-repayment schedule, they could enter 2024 debt-free with a surplus of nearly $4,000 per month to direct toward a down payment. In such a scenario, home ownership in the Connecticut market becomes a viable reality by 2025. Conversely, continued reliance on credit for "expected emergencies" (car repairs and vet bills) without a robust emergency fund will likely keep them in a cycle of high-interest obligations, delaying their goals indefinitely.

The transition from a refurbished mill to a "piece of earth to call their own" is within reach, but it requires a fundamental shift in how they perceive their $167,000 income—not as a lifestyle enabler, but as a tool for wealth construction.