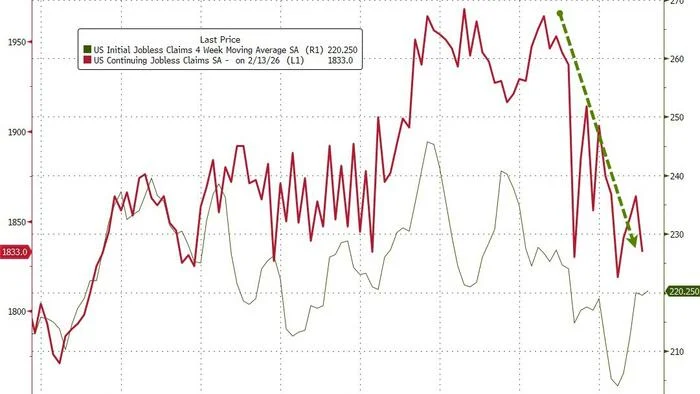

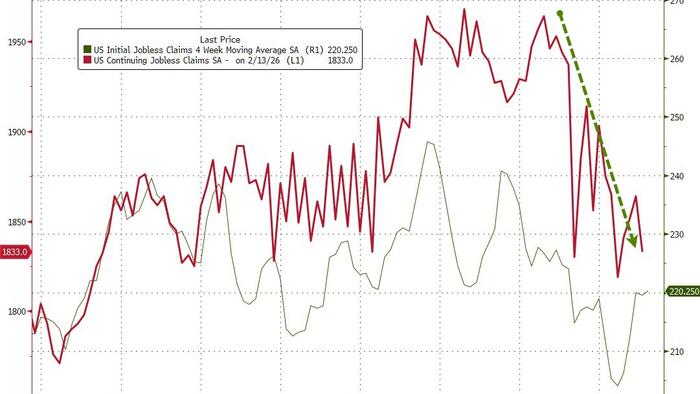

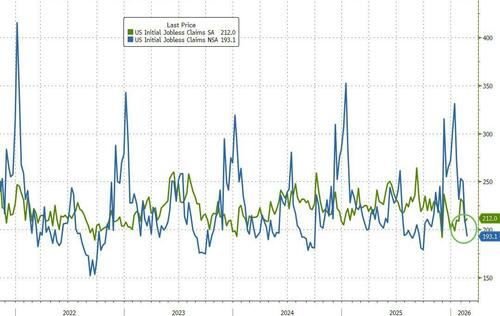

The American labor market continues to exhibit remarkable resilience, with initial jobless claims holding firm near multi-decade lows, confounding expectations for a significant slowdown and signaling an enduring strength within the economy. For the latest reporting week, 212,000 Americans filed for unemployment benefits for the first time, a figure that came in below the consensus estimate of 216,000. This sustained low level of claims, which saw unadjusted figures tumble to their lowest point since September, underscores a labor market that is yet to show any widespread signs of stress, despite persistent inflationary pressures and a prolonged period of elevated interest rates.

Understanding Jobless Claims: A Vital Economic Barometer

Initial jobless claims, reported weekly by the U.S. Department of Labor, serve as a crucial, timely indicator of the health of the labor market. These figures represent the number of individuals who filed for unemployment insurance benefits for the first time during a given week. A low number of initial claims typically suggests that employers are retaining their staff, and that widespread layoffs are not occurring. Conversely, a rising trend in initial claims can foreshadow an economic downturn or a weakening job market.

Continuing jobless claims, also reported weekly, track the number of individuals who are receiving unemployment benefits after their initial claim. This metric provides insight into the duration of unemployment and the ability of laid-off workers to find new employment. A decline in continuing claims suggests that more people are exiting the unemployment rolls, either because they have found new jobs or their benefits have expired, further reinforcing a positive outlook for labor market dynamics. Both indicators are closely watched by economists, policymakers, and investors alike for their real-time insights into economic momentum.

Detailed Analysis of the Latest Figures

The report highlighted that the 212,000 initial claims represented a slight decrease from the previous week’s revised total, reaffirming a trend of stability. This figure consistently hovers well below the historical average seen in robust economic periods, often considered to be in the 250,000-300,000 range before the pandemic. The unadjusted claims data, which can sometimes provide a clearer picture of underlying trends by removing seasonal adjustments, further bolstered the narrative of strength, registering its lowest level since September of the previous year. This suggests that the decline is not merely a statistical artifact of seasonal adjustments but reflects genuine underlying conditions in the employment landscape.

Beyond initial filings, the number of Americans receiving ongoing unemployment benefits also registered a notable decline. Continuing jobless claims dropped to 1.833 million, comfortably below the 1.9 million threshold that some analysts had termed the "Maginot Line" – a symbolic resistance level beyond which concerns about labor market weakening might escalate. This reduction in continuing claims suggests that those who do lose their jobs are either finding new employment relatively quickly or are exhausting their benefits, with the former being the more economically favorable interpretation. The consistent downward pressure on both initial and continuing claims paints a picture of a job market where job security remains high and unemployment spells are relatively short for many.

Regional Labor Market Dynamics

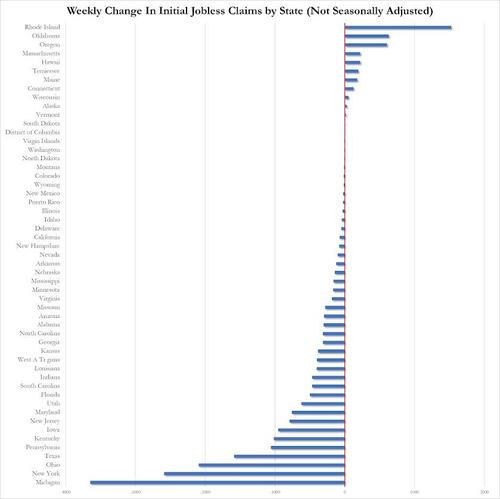

While the national picture remains robust, the report also provided granular insights into state-level variations in jobless claims, highlighting the heterogeneous nature of the U.S. labor market. Michigan and New York experienced the most significant drops in initial jobless claims last week. This could be attributed to a variety of factors, including seasonal hiring patterns, a rebound in specific industries prevalent in these states (e.g., manufacturing in Michigan, finance and tourism in New York), or localized economic stimulus. For instance, strong automotive sales could bolster employment in Michigan’s manufacturing sector, while a surge in travel and entertainment could positively impact New York’s service industries.

Conversely, Rhode Island and Oklahoma recorded the largest increases in claims. These localized upticks warrant closer examination to determine if they signal nascent weaknesses in particular sectors or if they are merely temporary fluctuations. In Rhode Island, a smaller state economy, even minor adjustments in specific industries like tourism or fishing could lead to noticeable shifts in unemployment figures. Similarly, Oklahoma’s economy, heavily influenced by energy and agriculture, could see claims rise due to volatility in commodity prices or seasonal agricultural cycles. These state-level divergences underscore the importance of looking beyond national aggregates to understand the full scope of labor market activity.

Historical Context and Recent Trends

The current state of jobless claims stands in stark contrast to the unprecedented surge experienced during the initial phase of the COVID-19 pandemic. In March and April 2020, initial jobless claims skyrocketed into the millions weekly, reaching an all-time peak of 6.8 million in a single week, as businesses across the nation shuttered and widespread layoffs ensued. This period marked the most severe and rapid deterioration of the U.S. labor market in modern history.

Following the initial shock, government stimulus, rapid vaccine development, and a gradual reopening of the economy led to a remarkable recovery. Jobless claims began a steady descent, albeit with intermittent fluctuations, returning to pre-pandemic levels much faster than many economists had predicted. Prior to the pandemic, typical initial claims hovered in the 200,000-250,000 range. The fact that current figures consistently remain within or even below this pre-pandemic benchmark, despite a significantly different economic environment characterized by high inflation and aggressive monetary tightening by the Federal Reserve, speaks volumes about the underlying strength and adaptability of the American workforce and employer base. This prolonged period of low claims, stretching over the past year, has been a key factor in defying recession predictions and sustaining economic growth.

Broader Economic Landscape: Interconnected Indicators

The robust performance of jobless claims does not occur in isolation but is deeply intertwined with other critical economic indicators, collectively painting a comprehensive picture of the U.S. economy.

-

Unemployment Rate: The U.S. unemployment rate has remained remarkably low, generally hovering between 3.7% and 3.9% for an extended period, close to a 50-year low. This figure, derived from the monthly jobs report, complements the jobless claims data by providing a broader measure of labor force utilization. Low claims reinforce the idea that few people are entering unemployment, while a low unemployment rate indicates that a high proportion of the labor force is actively employed.

-

Job Openings and Labor Turnover Survey (JOLTS): Data from the JOLTS report, while showing some moderation from its peak, continues to indicate a significant number of job openings across various sectors. When job openings remain high and jobless claims are low, it suggests a persistent demand for labor, even if the pace of hiring has slowed. The quits rate, another component of JOLTS, also remains elevated, signaling that workers are confident enough in their job prospects to voluntarily leave their positions, often for better opportunities. This dynamic contributes to wage growth and worker mobility.

-

Wage Growth: A tight labor market, characterized by low unemployment and strong demand for workers, typically leads to upward pressure on wages. While wage growth has moderated somewhat from its post-pandemic highs, it remains elevated compared to historical averages, contributing to consumer purchasing power but also posing a challenge to the Federal Reserve’s efforts to curb inflation. Sustained wage growth without a corresponding increase in productivity can fuel inflationary pressures.

-

Labor Force Participation Rate: The labor force participation rate, which measures the proportion of the working-age population that is either employed or actively seeking employment, has shown some gradual improvement but remains slightly below its pre-pandemic levels. While the low unemployment rate suggests tightness, a higher participation rate could alleviate some of the labor supply constraints and potentially temper wage pressures without necessarily increasing unemployment.

-

GDP Growth and Consumer Spending: A strong and stable labor market is a fundamental pillar of economic growth. High employment levels and steady incomes typically translate into robust consumer confidence and spending, which account for a significant portion of U.s. gross domestic product (GDP). The continued strength in jobless claims suggests that this vital engine of the economy remains well-lubricated, contributing to the economy’s ability to absorb shocks and sustain growth.

The "No Fire, No Hire" Phenomenon

The report’s conclusion referencing the "no fire-no hire" economy aptly describes a nuanced trend observed in the current labor market. This phenomenon suggests that employers, having faced significant challenges in recruiting and retaining talent in recent years, are now highly reluctant to lay off existing staff, even amidst economic uncertainties or a slowdown in demand. The memory of labor shortages and the high costs associated with recruitment, training, and onboarding new employees make companies prioritize retaining their current workforce.

Simultaneously, however, many businesses are adopting a more cautious approach to new hiring. High interest rates, elevated input costs, and a general sense of economic uncertainty are prompting companies to optimize their existing workforce rather than rapidly expand headcount. This dynamic results in a stable labor market where job losses are minimal ("no fire"), but the pace of new job creation might be slower than in previous boom cycles ("no hire"). The "no fire-no hire" economy therefore contributes to lower jobless claims and a stable unemployment rate, supporting trend growth, but it might also signify a more conservative business environment where aggressive expansion is less common.

Expert Analysis and Federal Reserve Implications

Economists largely interpret the consistently low jobless claims as a testament to the labor market’s enduring strength, a key factor that has allowed the U.S. economy to navigate inflationary pressures and higher interest rates without succumbing to a recession. Many analysts point to this resilience as evidence supporting the possibility of a "soft landing," where inflation is brought under control without triggering a significant increase in unemployment.

The Federal Reserve, which operates under a dual mandate of achieving maximum employment and price stability, closely scrutinizes these labor market indicators. Persistent strength in employment, as evidenced by low jobless claims and a low unemployment rate, provides the Fed with less immediate pressure to cut interest rates. While a cooling labor market would typically signal a need for monetary easing, the current data suggests that the labor component of the economy is still running hot. This could reinforce the Fed’s cautious stance, implying that interest rates might remain elevated for longer than some market participants anticipate, as policymakers continue to prioritize bringing inflation back down to their 2% target. Federal Reserve Chair Jerome Powell and other officials have repeatedly emphasized that their policy decisions are data-dependent, and the latest jobless claims figures will undoubtedly be a significant input into their ongoing assessment of economic conditions.

Outlook and Potential Challenges

While the current labor market data presents an optimistic picture, the economic landscape remains dynamic, and potential challenges persist. Geopolitical tensions, volatile energy prices, and the ongoing battle against inflation could still introduce unforeseen headwinds. The debate continues among economists regarding how long the labor market can maintain its current strength in the face of restrictive monetary policy. Some argue that a lagged effect of interest rate hikes could eventually lead to a more significant cooling, while others believe that structural shifts, such as demographics and ongoing labor shortages in certain sectors, will keep the labor market tight for the foreseeable future.

Looking ahead, market participants will continue to monitor weekly jobless claims, alongside other crucial economic releases such as the Consumer Price Index (CPI), Producer Price Index (PPI), and the monthly Nonfarm Payrolls report, for further indications of economic direction. The ability of the U.S. labor market to sustain its current vigor will be paramount in determining the trajectory of monetary policy and the overall health of the economy in the coming months.

In conclusion, the latest jobless claims report serves as a powerful reminder of the U.S. labor market’s surprising durability. With initial filings near multi-decade lows and continuing claims declining, the employment sector remains a steadfast pillar of economic stability, defying predictions of a sharper downturn and providing a crucial buffer against broader economic uncertainties. This resilience, while positive for workers and overall growth, will continue to shape the Federal Reserve’s policy considerations as it navigates the delicate balance between price stability and maximum employment.